Identity thieves have been exploiting a glaring security weakness in the website of Experian, one of the big three consumer credit reporting bureaus. Normally, Experian requires that those seeking a copy of their credit report successfully answer several multiple choice questions about their financial history. But until the end of 2022, Experian’s website allowed anyone to bypass these questions and go straight to the consumer’s report. All that was needed was the person’s name, address, birthday and Social Security number.

The vulnerability in Experian’s website was exploitable after one applied to see their credit file via annualcreditreport.com.

In December, KrebsOnSecurity heard from Jenya Kushnir, a security researcher living in Ukraine who said he discovered the method being used by identity thieves after spending time on Telegram chat channels dedicated to the cashing out of compromised identities.

“I want to try and help to put a stop to it and make it more difficult for [ID thieves] to access, since [Experian is] not doing shit and regular people struggle,” Kushnir wrote in an email to KrebsOnSecurity explaining his motivations for reaching out. “If somehow I can make small change and help to improve this, inside myself I can feel that I did something that actually matters and helped others.”

Kushnir said the crooks learned they could trick Experian into giving them access to anyone’s credit report, just by editing the address displayed in the browser URL bar at a specific point in Experian’s identity verification process.

Following Kushnir’s instructions, I sought a copy of my credit report from Experian via annualcreditreport.com — a website that is required to provide all Americans with a free copy of their credit report from each of the three major reporting bureaus, once per year.

Annualcreditreport.com begins by asking for your name, address, SSN and birthday. After I supplied that and told Annualcreditreport.com I wanted my report from Experian, I was taken to Experian.com to complete the identity verification process.

![]()

Normally at this point, Experian’s website would present four or five multiple-guess questions, such as “Which of the following addresses have you lived at?”

Kushnir told me that when the questions page loads, you simply change the last part of the URL from “/acr/oow/” to “/acr/report,” and the site would display the consumer’s full credit report.

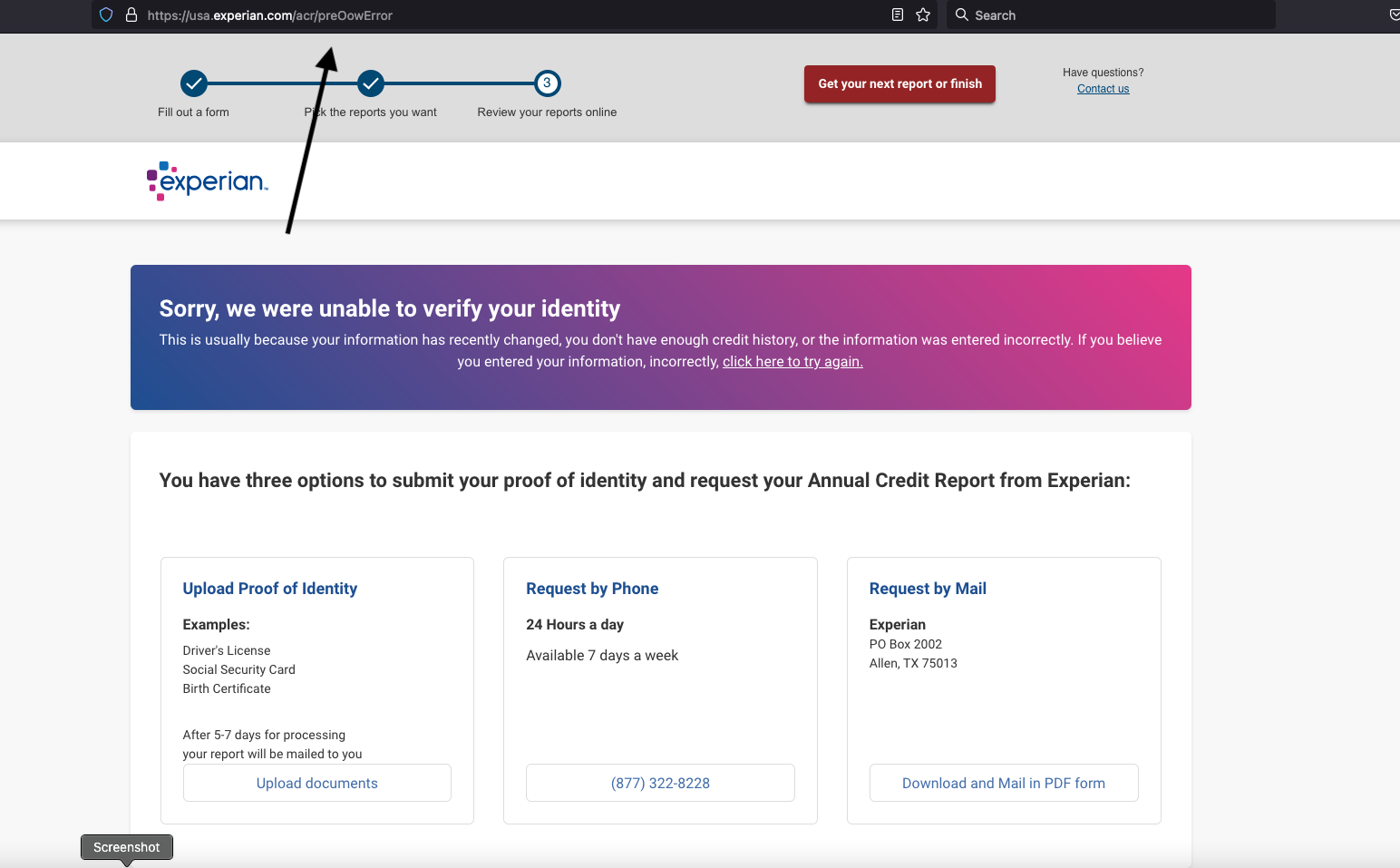

But when I tried to get my report from Experian via annualcreditreport.com, Experian’s website said it didn’t have enough information to validate my identity. It wouldn’t even show me the four multiple-guess questions. Experian said I had three options for a free credit report at this point: Mail a request along with identity documents, call a phone number for Experian, or upload proof of identity via the website.

But that didn’t stop Experian from showing me my full credit report after I changed the Experian URL as Kushnir had instructed — modifying the error page’s trailing URL from “/acr/OcwError” to simply “/acr/report”.

Experian’s website then immediately displayed my entire credit file.

Even though Experian said it couldn’t tell that I was actually me, it still coughed up my report. And thank goodness it did. The report contains so many errors that it’s probably going to take a good deal of effort on my part to straighten out.

Now I know why Experian has NEVER let me view my own file via their website. For example, there were four phone numbers on my Experian credit file: Only one of them was mine, and that one hasn’t been mine for ages.

I was so dumbfounded by Experian’s incompetence that I asked a close friend and trusted security source to try the method on her identity file at Experian. Sure enough, when she got to the part where Experian asked questions, changing the last part of the URL in her address bar to “/report” bypassed the questions and immediately displayed her full credit report. Her report also was replete with errors.

KrebsOnSecurity shared Kushnir’s findings with Experian on Dec. 23, 2022. On Dec. 27, 2022, Experian’s PR team acknowledged receipt of my Dec. 23 notification, but the company has so far ignored multiple requests for comment or clarification.

By the time Experian confirmed receipt of my report, the “exploit” Kushnir said he learned from the identity thieves on Telegram had been patched and no longer worked. But it remains unclear how long Experian’s website was making it so easy to access anyone’s credit report.

In response to information shared by KrebsOnSecurity, Senator Ron Wyden (D-Ore.) said he was disappointed — but not at all surprised — to hear about yet another cybersecurity lapse at Experian.

“The credit bureaus are poorly regulated, act as if they are above the law and have thumbed their noses at Congressional oversight,” Wyden said in a written statement. “Just last year, Experian ignored repeated briefing requests from my office after you revealed another cybersecurity lapse the company.”

Sen. Wyden’s quote above references a story published here in July 2022, which broke the news that identity thieves were hijacking consumer accounts at Experian.com just by signing up as them at Experian once more, supplying the target’s static, personal information (name, DoB/SSN, address) but a different email address.

From interviews with multiple victims who contacted KrebsOnSecurity after that story, it emerged that Experian’s own customer support representatives were actually telling consumers who got locked out of their Experian accounts to recreate their accounts using their personal information and a new email address. This was Experian’s advice even for people who’d just explained that this method was what identity thieves had used to lock them in out in the first place.

Clearly, Experian found it simpler to respond this way, rather than acknowledging the problem and addressing the root causes (lazy authentication and abhorrent account recovery practices). It’s also worth mentioning that reports of hijacked Experian.com accounts persisted into late 2022. That screw-up has since prompted a class action lawsuit against Experian.

Sen. Wyden said the Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB) need to do much more to protect Americans from screw-ups by the credit bureaus.

“If they don’t believe they have the authority to do so, they should endorse legislation like my Mind Your Own Business Act, which gives the FTC power to set tough mandatory cybersecurity standards for companies like Experian,” Wyden said.

Sadly, none of this is terribly shocking behavior for Experian, which has shown itself a completely negligent custodian of obscene amounts of highly sensitive consumer information.

In April 2021, KrebsOnSecurity revealed how identity thieves were exploiting lax authentication on Experian’s PIN retrieval page to unfreeze consumer credit files. In those cases, Experian failed to send any notice via email when a freeze PIN was retrieved, nor did it require the PIN to be sent to an email address already associated with the consumer’s account.

A few days after that April 2021 story, KrebsOnSecurity broke the news that an Experian API was exposing the credit scores of most Americans.

It’s bad enough that we can’t really opt out of companies like Experian making $2.6 billion each quarter collecting and selling gobs of our personal and financial information. But there has to be some meaningful accountability when these monopolistic companies engage in negligent and reckless behavior with the very same consumer data that feeds their quarterly profits. Or when security and privacy shortcuts are found to be intentional, like for cost-saving reasons.

And as we saw with Equifax’s consolidated class-action settlement in response to letting state-sponsored hackers from China steal data on nearly 150 million Americans back in 2017, class-actions and more laughable “free credit monitoring” services from the very same companies that created the problem aren’t going to cut it.

It is easy to adopt a defeatist attitude with the credit bureaus, who often foul things up royally even for consumers who are quite diligent about watching their consumer credit files and disputing any inaccuracies.

But there are some concrete steps that everyone can take which will dramatically lower the risk that identity thieves will ruin your financial future. And happily, most of these steps have the side benefit of costing the credit bureaus money, or at least causing the data they collect about you to become less valuable over time.

The first step is awareness. Find out what these companies are saying about you behind your back. Keep in mind that — fair or not — your credit score as collectively determined by these bureaus can affect whether you get that loan, apartment, or job. In that context, even small, unintentional errors that are unrelated to identity theft can have outsized consequences for consumers down the road.

Each bureau is required to provide a free copy of your credit report every year. The easiest way to get yours is through annualcreditreport.com.

Some consumers report that this site never works for them, and that each bureau will insist they don’t have enough information to provide a report. I am definitely in this camp. Thankfully, a financial institution that I already have a relationship with offers the ability to view your credit file through them. Your mileage on this front may vary, and you may end up having to send copies of your identity documents through the mail or website.

When you get your report, look for anything that isn’t yours, and then document and file a dispute with the corresponding credit bureau. And after you’ve reviewed your report, set a calendar reminder to recur every four months, reminding you it’s time to get another free copy of your credit file.

If you haven’t already done so, consider making 2023 the year that you freeze your credit files at the three major reporting bureaus, including Experian, Equifax and TransUnion. It is now free to people in all 50 U.S. states to place a security freeze on their credit files. It is also free to do this for your partner and/or your dependents.

Freezing your credit means no one who doesn’t already have a financial relationship with you can view your credit file, making it unlikely that potential creditors will grant new lines of credit in your name to identity thieves. Freezing your credit file also means Experian and its brethren can no longer sell peeks at your credit history to others.

Anytime you wish to apply for new credit or a new job, or open an account at a utility or communications provider, you can quickly thaw a freeze on your credit file, and set it to freeze automatically again after a specified length of time.

Please don’t confuse a credit freeze (a.k.a. “security freeze”) with the alternative that the bureaus will likely steer you towards when you ask for a freeze: “Credit lock” services.

The bureaus pitch these credit lock services as a way for consumers to easily toggle their credit file availability with push of a button on a mobile app, but they do little to prevent the bureaus from continuing to sell your information to others.

My advice: Ignore the lock services, and just freeze your credit files already.

One final note. Frequent readers here will have noticed that I’ve criticized these so-called “knowledge-based authentication” or KBA questions that Experian’s website failed to ask as part of its consumer verification process.

KrebsOnSecurity has long assailed KBA as weak authentication because the questions and answers are drawn largely from consumer records that are public and easily accessible to organized identity theft groups.

That said, given that these KBA questions appear to be the ONLY thing standing between me and my Experian credit report, it seems like maybe they should at least take care to ensure that those questions actually get asked.

Learning meets fun at the 2022 SANS Holiday Hack Challenge – strap yourself in for a crackerjack ride at the North Pole as I foil Grinchum's foul plan and recover the five golden rings

The post Cracked it! Highlights from KringleCon 5: Golden Rings appeared first on WeLiveSecurity

Ransomware. Even the name sounds scary.

When you get down to it, ransomware is one of the nastiest attacks a hacker can wage. They target some of our most important and precious things—our files, our photos, and the information stored on our devices. Think about suddenly losing access to all of them and being forced to pay a ransom to get access back. Worse yet, paying the ransom is no guarantee the hacker will return them.

That’s what a ransomware attack does. Broadly speaking, it’s a type of malware that infects a network or a device and then typically encrypts the files, data, and apps stored on it, digitally scrambling them so the proper owners can’t access them. Only a digital key can unlock them—one that the hacker holds.

Nasty for sure, yet you can take several steps that can greatly reduce the risk of it happening to you. Our recently published Ransomware Security Guide breaks them down for you, and in this blog we’ll look at a few reasons why ransomware protection is so vital.

The short answer is pretty bad—to the tune of billions of dollars stolen from victims each year. Ransomware targets people and their families just as explained above. Yet it also targets large organizations, governments, and even companies that run critical stretches of energy infrastructure and the food supply chain. Accordingly, the ransom amounts for these victims climb into millions of dollars.

A few recent cases of large-scale ransomware attacks include:

Who’s behind such attacks? Given the scope and scale of them, it’s often organized hacking groups. Put simply, these are big heists. It demands expertise to pull them off, not to mention further expertise to transfer large sums of cryptocurrency in ways that cover the hackers’ tracks.

As for ransomware attacks on people and their families, the individual dollar amounts of an attack are far lower, typically in the hundreds of dollars. Again, the culprits behind them may be large hacking groups that cast a wider net for individual victims, where hundreds of successful attacks at hundreds of dollars each quickly add up. One example: a hacker group that posed as a government agency and as a major retailer, which mailed out thousands of USB drives infected with malware.

Other ransomware hackers who target people and families are far less sophisticated. Small-time hackers and hacking groups can find the tools they need to conduct such attacks by shopping on the dark web, where ransomware is available for sale or for lease as a service (Ransomware as a Service, or RaaS). In effect, near-amateur hackers can grab a ready-to-deploy attack right off the shelf.

Taken together, hackers will level a ransomware attack at practically anyone or any organization—making it everyone’s concern.

Hackers have several ways of getting ransomware onto one of your devices. Like any other type of malware, it can infect your device via a phishing link or a bogus attachment. It can also end up there by downloading apps from questionable app stores, with a stolen or hacked password, or through an outdated device or network router with poor security measures in place. And as mentioned above, infected storage devices provide another avenue.

Social engineering attacks enter the mix as well, where the hacker poses as someone the victim knows and gets the victim to either download malware or provide the hacker access to an otherwise password-protected device, app, or network.

And yes, ransomware can end up on smartphones as well.

While not a prevalent as other types of malware attacks, smartphone ransomware can encrypt files, photos, and the like on a smartphone, just as it can on computers and networks. Yet other forms of mobile ransomware don’t have to encrypt data to make the phone unusable. The “Lockerpin” ransomware that has struck some Android devices in the past would change the PIN number that locked the phone. Other forms of mobile ransomware paste a window over the phone’s apps, making them unusable without decrypting the ransomware.

Part of avoiding ransomware involves reducing human error—keeping a watchful eye open for those spammy links, malicious downloads, bogus emails, and basically keeping your apps and devices up to date so that they have the latest security measures in place. The remainder relies on a good dose of prevention.

Our Ransomware Security Guide provides a checklist for both.

It gets into the details of what ransomware looks like and how it works, followed by the straightforward things you can do to prevent it, along with the steps to take if the unfortunate ends up happening to you or someone you know.

Ransomware is one of the nastiest attacks going because it targets our files, photos, and information, things we don’t know where we’d be without. Yet it’s good to know you can indeed lower your risk with a few relatively simple steps. Once you have them in place, chances are a good feeling will come over you, the one that comes with knowing you’ve protected what’s precious and important to you.

The post Your Guide to Ransomware—and Preventing It Too appeared first on McAfee Blog.

Hybrid work and hybrid play now merge into hybrid living, but where is the line between the two? Is there one?

The post Hybrid work: Turning business platforms into preferred social spaces appeared first on WeLiveSecurity

In Brief The Federal Communications Commission plans to overhaul its security reporting rules for the telecom industry to, among other things, eliminate a mandatory seven-day wait for informing customers of stolen data and expand the definition of what constitutes an incident.…

Briefly this week, it appeared that quantum computers might finally be ready to break 2048-bit RSA encryption, but that moment has passed.…

Multiple bugs affecting millions of vehicles from almost all major car brands could allow miscreants to perform any manner of mischief — in some cases including full takeovers — by exploiting vulnerabilities in the vehicles' telematic systems, automotive APIs and supporting infrastructure, according to security researchers.…

An international law enforcement effort has released a decryptor for victims of MegaCortex ransomware, widely used by cybercriminals to infect large corporations across 71 countries to the tune of more than $100 million in damages.…

![]()

![]()

![]()

Authored by Vonny Gamot

The official 40th birthday of the internet serves as a timely reminder that while it is a fantastic place, we must practice good digital hygiene to safeguard our privacy and identity so we can protect ourselves from the latest threats.

Since its widely recognized creation on January 1st 1983, the internet has since transformed economies and the everyday lives of people. From social media, memes, and viral videos to smart homes, online shopping and even cloud computing, the internet entertains, educates, and connects us. Above all, it will continue to play a crucial role in human civilization for many generations to come.

Yet with the good comes the not-so-good. Wherever people gather, cyberthieves gather too. The internet is no exception. As the evolution of the internet continues, cybercriminals are evolving in tandem, looking for new and inventive ways, such as using Artificial Intelligence to exploit its features. With over five billion people accessing and using the Internet in 2022, that’s over 60% of the world’s population potentially at risk.

So, while we celebrate the internet’s 40th birthday, it’s also a good reminder to take stock of the latest online threats and ensure our digital hygiene is up to scratch for the year ahead. When we do this, we can take full advantage of the incredible opportunities the internet affords us.

The new year is a great moment to reflect, reset, and consider your personal online safety and protection. Stay vigilant against the latest threats and scams and use dedicated and robust online protection software such as our newly released McAfee+ plans—which comes with important features like identity monitoring that can spot your personal info on the dark web and personal data cleanup that can help remove your personal info from data broker sites that will sell it to companies and crooks alike.

It’s also a time to keep a fresh eye out for scams and phishing attacks. If that email, text, or message you received looks too good to be true, or you feel that the sender is trying to pressure you into doing sharing info or sending money, it’s always best to double check that the source is legitimate. These are often indicators that a scam is afoot.

Beyond using online protection software and keeping your guard up, you can take several other steps that can make you immediately safer than you were before. Here are four strong suggestions that will get you started:

MFA is an excellent way to frustrate cybercriminals attempting to break into online accounts. MFA means that users need more than a username and password to log in, for example, a one-time code sent to private email, text, or through an authentication app utilizing face or fingerprint scans. This adds an extra layer of security as the cybercriminal has to access the device, email, or biometric reader to get into someone’s online account.

Strong, unique passwords for each of your online accounts are a must. It’s always important for people to understand that reusing passwords is just as risky as using “password123” and puts online accounts at risk. A tactic known as “credential stuffing” is where a cybercriminal attempts to input stolen usernames and password combinations in dozens of random websites to see which door it opens. It is also important to consider using password managers which can create and safeguard all passwords in one secure desktop extension or mobile phone app.

Updating software is vital to the security of a device. These updates include security patches that cyber experts have created to foil cybercriminals. The more outdated the software is, the more time criminals have had to work out ways to infiltrate and steal information within them. Moreover, updates often include new and improved features, which makes a strong case for keeping things current.

Phishing is when a scammer sends texts or emails that appear to be from trusted sources like your favourite online clothing store, employer or, as we’re seeing during the cost-of-living crisis, energy firms, or banks. They do this to encourage people to share personal information.

Once a phishing attempt has been recognised it is vital that they are not engaged with, links are left unopened, and the potential scam email is not forwarded along to another person. Before the message is deleted, it is vital that the sender is blocked and that the message is marked as junk and reported.

If you think that you have entered your credit card details onto a phishing website, contact your bank or credit card issuing company immediately. Report your personal information as stolen, and you may want to request that your existing card be canceled depending on the circumstances.

Online protection is part mindset, part prevention, and part action. While the steps above mark a start, they’re just that. There’s plenty more you can do, and when taken in batches, the steps you take can really add up to an exceptional level of protection. The question is, where to start?

Our McAfee Safety Series can get you moving in the right direction. It’s a set of guides that cover a range of important security topics and that show you several straightforward things you can do that will make you safer. They range from phishing and privacy to online shopping and safer online media. In all, they can help you spot scams, hacks, and attacks—and potentially prevent them in the first place.

I encourage you to grab the first one that looks interesting to you. What you learn can put you several steps ahead of the hackers, scammers, and thieves out there.

The post 40 Years of the Internet – Tips for Staying Safe Online in 2023 appeared first on McAfee Blog.

Webinar How does your security team prioritize work? When a new attack from a state actor hits the news, do you know if your team should drop everything to hunt for IOCs? Do you understand your security control coverage for the threat actors that might target your organization? Recently, the Red Canary corporate security team asked itself these questions when it was creating its own threat model.…

A variant of the bad penny that is Dridex, the general-purpose malware that has been around for years, now has macOS platforms in its sights and a new way of delivering malicious macros via documents.…

Speaking to many CISOs, it’s clear that many security executives view zero trust as a journey that can be difficult to start, and one that even makes identifying successful outcomes a challenge. Simultaneously, the topic of security resilience has risen up the C-level agenda and is now another focus for security teams. So, are these complementary? Or will they present conflicting demands that will disrupt rather than assist the CISO in their role?

One of the most striking results coming from Cisco’s latest Security Outcomes Report is that organizations with a mature zero trust implementation – those with basic controls, constant validation and automated workflows – experience a 30% improvement in security resilience compared to those who have not started their zero trust journey. So, these two initiatives – implementing zero trust and working to achieve security resilience – appear to complement each other while supporting the CISO when a cyber black swan swims in.

Security resilience is the ability to withstand an incident and recover more strongly. In other words, ride out the storm and come back better. Meanwhile, zero trust is best known as a “never trust, always verify” principle. The idea is to check before you provide access, and authenticate identity based on a risk profile of assets and users. This starts to explain why the two are complementary.

The Security Outcomes Report summarizes the results of a survey of more than 4,700 security professionals. Among the insights that emerge are nine security resilience outcomes they consider most important. The top three outcomes for resilience are prevention, mitigation and adaptation. In other words, they prioritize first the ability to avoid an incident by having the right controls in place, then the ability to reduce and reverse the overall impact when an incident occurs, and then the ability to pivot rapidly without being bound by too rigid a set of systems. Zero trust will support these outcomes.

Preventing, or reducing the likelihood of a cybersecurity incident, is an obvious first step and no surprise as the most important outcome. Pursuing programs that identify users and monitor the health of devices is a crucial a preventative step. In fact, simply ensuring that multifactor authentication (MFA) is ubiquitous across the organization can bring an 11% improvement in security resilience.

When incidents occur, security teams will need a clear picture of the incident they are having to manage. This will help in them respond quickly, with a proactive determination of recovery requirements. Previous studies show that once a team achieves 80% coverage of critical systems, the ability to maintain continuity increases measurably. This knowledge will also help teams develop more focused incident response processes. A mature zero trust environment has also been found to almost double a team’s ability to streamline these processes when compared to a limited zero trust implementation.

When talking to CISOs about successful implementation programs, communication within the business emerges as a recurring theme. Security teams must inform and guide users through the phases of zero trust implementation, while emphasizing the benefits to them. When users are aware of their responsibility to keep the organization secure, they take a participatory role in an important aspect of the business. So, when an incident occurs, they can support the company’s response. This increases resilience. Research has shown that a mature program will more than double the effect of efforts to improve the security culture. Additionally, the same communication channels established to spread the word of zero trust now can be called upon when an incident requires immediate action.

Mature implementations have also been seen to help increase cost effectiveness and reduce unplanned work. This releases more resource to cope with the unexpected – another important driver of resilience surfaced in Volume 3 of the Security Outcomes Report. Having more efficient resources enables the security function to reallocate teams when needed. Reviewing and updating resource processes and procedures, along with all other important processes, is a vital part of any of any change initiative. Mature zero trust environments reflect this commitment continuous assessment and improvement.

Inherent in organizational resilience is the ability to adapt and innovate. The corporate landscape is littered with examples of those who failed to do those two things. A zero trust environment enables organizations to lower their risk of incidents while adapting their security posture to fit the ongoing changes of the business. Think of developing new partners, supporting new products remotely, securing a changing supply chain. The basic tenets of MFA – including continuous validation, segmentation and automation – sets a foundation that accommodates those changes without compromising security. The view that security makes change difficult is becoming obsolete. With zero trust and other keys to achieving security resilience, security now is a partner in business change. And for those CISOs who fear even starting this journey, understanding the benefits should help them take that first step.

Download the Security Outcomes Report, Vol. 3: Achieving Security Resilience today.

Learn more about cybersecurity research and security resilience:

We’d love to hear what you think. Ask a Question, Comment Below, and Stay Connected with Cisco Secure on social!

Cisco Secure Social Channels

A New York federal judge told JP Morgan Chase Bank this week that he would not toss a lawsuit accusing the bank of ignoring red flags when cybercrooks stole $272 million from the New York account of the company that makes Ray-Bans in 2019.…