One of the cybercrime underground’s more active sellers of Social Security numbers, background and credit reports has been pulling data from hacked accounts at the U.S. consumer data broker USinfoSearch, KrebsOnSecurity has learned.

![]() Since at least February 2023, a service advertised on Telegram called USiSLookups has operated an automated bot that allows anyone to look up the SSN or background report on virtually any American. For prices ranging from $8 to $40 and payable via virtual currency, the bot will return detailed consumer background reports automatically in just a few moments.

Since at least February 2023, a service advertised on Telegram called USiSLookups has operated an automated bot that allows anyone to look up the SSN or background report on virtually any American. For prices ranging from $8 to $40 and payable via virtual currency, the bot will return detailed consumer background reports automatically in just a few moments.

USiSLookups is the project of a cybercriminal who uses the nicknames JackieChan/USInfoSearch, and the Telegram channel for this service features a small number of sample background reports, including that of President Joe Biden, and podcaster Joe Rogan. The data in those reports includes the subject’s date of birth, address, previous addresses, previous phone numbers and employers, known relatives and associates, and driver’s license information.

JackieChan’s service abuses the name and trademarks of Columbus, OH based data broker USinfoSearch, whose website says it provides “identity and background information to assist with risk management, fraud prevention, identity and age verification, skip tracing, and more.”

“We specialize in non-FCRA data from numerous proprietary sources to deliver the information you need, when you need it,” the company’s website explains. “Our services include API-based access for those integrating data into their product or application, as well as bulk and batch processing of records to suit every client.”

As luck would have it, my report was also listed in the Telegram channel for this identity fraud service, presumably as a teaser for would-be customers. On October 19, 2023, KrebsOnSecurity shared a copy of this file with the real USinfoSearch, along with a request for information about the provenance of the data.

USinfoSearch said it would investigate the report, which appears to have been obtained on or before June 30, 2023. On Nov. 9, 2023, Scott Hostettler, general manager of USinfoSearch parent Martin Data LLC shared a written statement about their investigation that suggested the ID theft service was trying to pass off someone else’s consumer data as coming from USinfoSearch:

Regarding the Telegram incident, we understand the importance of protecting sensitive information and upholding the trust of our users is our top priority. Any allegation that we have provided data to criminals is in direct opposition to our fundamental principles and the protective measures we have established and continually monitor to prevent any unauthorized disclosure. Because Martin Data has a reputation for high-quality data, thieves may steal data from other sources and then disguise it as ours. While we implement appropriate safeguards to guarantee that our data is only accessible by those who are legally permitted, unauthorized parties will continue to try to access our data. Thankfully, the requirements needed to pass our credentialing process is tough even for established honest companies.

USinfoSearch’s statement did not address any questions put to the company, such as whether it requires multi-factor authentication for customer accounts, or whether my report had actually come from USinfoSearch’s systems.

After much badgering, on Nov. 21 Hostettler acknowledged that the USinfoSearch identity fraud service on Telegram was in fact pulling data from an account belonging to a vetted USinfoSearch client.

“I do know 100% that my company did not give access to the group who created the bots, but they did gain access to a client,” Hostettler said of the Telegram-based identity fraud service. “I apologize for any inconvenience this has caused.”

Hostettler said USinfoSearch heavily vets any new potential clients, and that all users are required to undergo a background check and provide certain documents. Even so, he said, several fraudsters each month present themselves as credible business owners or C-level executives during the credentialing process, completing the application and providing the necessary documentation to open a new account.

“The level of skill and craftsmanship demonstrated in the creation of these supporting documents is incredible,” Hostettler said. “The numerous licenses provided appear to be exact replicas of the original document. Fortunately, I’ve discovered several methods of verification that do not rely solely on those documents to catch the fraudsters.”

“These people are unrelenting, and they act without regard for the consequences,” Hostettler continued. “After I deny their access, they will contact us again within the week using the same credentials. In the past, I’ve notified both the individual whose identity is being used fraudulently and the local police. Both are hesitant to act because nothing can be done to the offender if they are not apprehended. That is where most attention is needed.”

JackieChan is most active on Telegram channels focused on “SIM swapping,” which involves bribing or tricking mobile phone company employees into redirecting a target’s phone number to a device the attackers control. SIM swapping allows crooks to temporarily intercept the target’s text messages and phone calls, including any links or one-time codes for authentication that are delivered via SMS.

Reached on Telegram, JackieChan said most of his clients hail from the criminal SIM swapping world, and that the bulk of his customers use his service via an application programming interface (API) that allows customers to integrate the lookup service with other web-based services, databases, or applications.

“Sim channels is where I get most of my customers,” JackieChan told KrebsOnSecurity. “I’m averaging around 100 lookups per day on the [Telegram] bot, and around 400 per day on the API.”

JackieChan claims his USinfoSearch bot on Telegram abuses stolen credentials needed to access an API used by the real USinfoSearch, and that his service was powered by USinfoSearch account credentials that were stolen by malicious software tied to a botnet that he claims to have operated for some time.

This is not the first time USinfoSearch has had trouble with identity thieves masquerading as legitimate customers. In 2013, KrebsOnSecurity broke the news that an identity fraud service in the underground called “SuperGet[.]info” was reselling access to personal and financial data on more than 200 million Americans that was obtained via the big-three credit bureau Experian.

The consumer data resold by Superget was not obtained directly from Experian, but rather via USinfoSearch. At the time, USinfoSearch had a contractual agreement with a California company named Court Ventures, whereby customers of Court Ventures had access to the USinfoSearch data, and vice versa.

When Court Ventures was purchased by Experian in 2012, the proprietor of SuperGet — a Vietnamese hacker named Hieu Minh Ngo who had impersonated an American private investigator — was grandfathered in as a client. The U.S. Secret Service agent who oversaw Ngo’s capture, extradition, prosecution and rehabilitation told KrebsOnSecurity he’s unaware of any other cybercriminal who has caused more material financial harm to more Americans than Ngo.

JackieChan also sells access to hacked email accounts belonging to law enforcement personnel in the United States and abroad. Hacked police department emails can come in handy for ID thieves trying to pose as law enforcement officials who wish to purchase consumer data from platforms like USinfoSearch. Hence, Mr. Hostettler’s ongoing battle with fraudsters seeking access to his company’s service.

These police credentials are mainly marketed to criminals seeking fraudulent “Emergency Data Requests,” wherein crooks use compromised government and police department email accounts to rapidly obtain customer account data from mobile providers, ISPs and social media companies.

Normally, these companies will require law enforcement officials to supply a subpoena before turning over customer or user records. But EDRs allow police to bypass that process by attesting that the information sought is related to an urgent matter of life and death, such as an impending suicide or terrorist attack.

![]()

In response to an alarming increase in the volume of fraudulent EDRs, many service providers have chosen to require all EDRs be processed through a service called Kodex, which seeks to filter EDRs based on the reputation of the law enforcement entity requesting the information, and other attributes of the requestor.

For example, if you want to send an EDR to Coinbase or Twilio, you’ll first need to have valid law enforcement credentials and create an account at the Kodex online portal at these companies. However, Kodex may still throttle or block any requests from any accounts if they set off certain red flags.

Within their own separate Kodex portals, Twilio can’t see requests submitted to Coinbase, or vice versa. But each can see if a law enforcement entity or individual tied to one of their own requests has ever submitted a request to a different Kodex client, and then drill down further into other data about the submitter, such as Internet address(es) used, and the age of the requestor’s email address.

In August, JackieChan was advertising a working Kodex account for sale on the cybercrime channels, including redacted screenshots of the Kodex account dashboard as proof of access.

Kodex co-founder Matt Donahue told KrebsOnSecurity his company immediately detected that the law enforcement email address used to create the Kodex account pictured in JackieChan’s ad was likely stolen from a police officer in India. One big tipoff, Donahue said, was that the person creating the account did so using an Internet address in Brazil.

“There’s a lot of friction we can put in the way for illegitimate actors,” Donahue said. “We don’t let people use VPNs. In this case we let them in to honeypot them, and that’s how they got that screenshot. But nothing was allowed to be transmitted out from that account.”

Massive amounts of data about you and your personal history are available from USinfoSearch and dozens of other data brokers that acquire and sell “non-FCRA” data — i.e., consumer data that cannot be used for the purposes of determining one’s eligibility for credit, insurance, or employment.

Anyone who works in or adjacent to law enforcement is eligible to apply for access to these data brokers, which often market themselves to police departments and to “skip tracers,” essentially bounty hunters hired to locate others in real life — often on behalf of debt collectors, process servers or a bail bondsman.

There are tens of thousands of police jurisdictions around the world — including roughly 18,000 in the United States alone. And the harsh reality is that all it takes for hackers to apply for access to data brokers (and abuse the EDR process) is illicit access to a single police email account.

The trouble is, compromised credentials to law enforcement email accounts show up for sale with alarming frequency on the Telegram channels where JackieChan and their many clients reside. Indeed, Donahue said Kodex so far this year has identified attempted fake EDRs coming from compromised email accounts for police departments in India, Italy, Thailand and Turkey.

In the summer of 2022, KrebsOnSecurity documented the plight of several readers who had their accounts at big-three consumer credit reporting bureau Experian hijacked after identity thieves simply re-registered the accounts using a different email address. Sixteen months later, Experian clearly has not addressed this gaping lack of security. I know that because my account at Experian was recently hacked, and the only way I could recover access was by recreating the account.

Entering my SSN and birthday at Experian showed my identity was tied to an email address I did not authorize.

I recently ordered a copy of my credit file from Experian via annualcreditreport.com, but as usual Experian declined to provide it, saying they couldn’t verify my identity. Attempts to log in to my account directly at Experian.com also failed; the site said it didn’t recognize my username and/or password.

A request for my Experian account username required my full Social Security number and date of birth, after which the website displayed portions of an email address I never authorized and did not recognize (the full address was redacted by Experian).

I immediately suspected that Experian was still allowing anyone to recreate their credit file account using the same personal information but a different email address, a major authentication failure that was explored in last year’s story, Experian, You Have Some Explaining to Do. So once again I sought to re-register as myself at Experian.

The homepage said I needed to provide a Social Security number and mobile phone number, and that I’d soon receive a link that I should click to verify myself. The site claims that the phone number you provide will be used to help validate your identity. But it appears you could supply any phone number in the United States at this stage in the process, and Experian’s website would not balk. Regardless, users can simply skip this step by selecting the option to “Continue another way.”

Experian then asks for your full name, address, date of birth, Social Security number, email address and chosen password. After that, they require you to successfully answer between three to five multiple-choice security questions whose answers are very often based on public records. When I recreated my account this week, only two of the five questions pertained to my real information, and both of those questions concerned street addresses we’ve previously lived at — information that is just a Google search away.

Assuming you sail through the multiple-choice questions, you’re prompted to create a 4-digit PIN and provide an answer to one of several pre-selected challenge questions. After that, your new account is created and you’re directed to the Experian dashboard, which allows you to view your full credit file, and freeze or unfreeze it.

At this point, Experian will send a message to the old email address tied to the account, saying certain aspects of the user profile have changed. But this message isn’t a request seeking verification: It’s just a notification from Experian that the account’s user data has changed, and the original user is offered zero recourse here other than to a click a link to log in at Experian.com.

If you don’t have an Experian account, it’s a good idea to create one. Because at least then you will receive one of these emails when someone hijacks your credit file at Experian.

And of course, a user who receives one of these notices will find that the credentials to their Experian account no longer work. Nor do their PIN or account recovery question, because those have been changed also. Your only option at this point is recreate your account at Experian and steal it back from the ID thieves!

In contrast, if you try to modify an existing account at either of the other two major consumer credit reporting bureaus — Equifax or TransUnion — they will ask you to enter a code sent to the email address or phone number on file before any changes can be made.

Reached for comment, Experian declined to share the full email address that was added without authorization to my credit file.

“To ensure the protection of consumers’ identities and information, we have implemented a multi-layered security approach, which includes passive and active measures, and are constantly evolving,” Experian spokesperson Scott Anderson said in an emailed statement. “This includes knowledge-based questions and answers, and device possession and ownership verification processes.”

Anderson said all consumers have the option to activate a multi-factor authentication method that’s requested each time they log in to their account. But what good is multi-factor authentication if someone can simply recreate your account with a new phone number and email address?

Several readers who spotted my rant about Experian on Mastodon earlier this week responded to a request to validate my findings. The Mastodon user @Jackerbee is a reader from Michican who works in the biotechnology industry. @Jackerbee said when prompted by Experian to provide his phone number and the last four digits of his SSN, he chose the option to “manually enter my information.”

“I put my second phone number and the new email address,” he explained. “I received a single email in my original account inbox that said they’ve updated my information after I ‘signed up.’ No verification required from the original email address at any point. I also did not receive any text alerts at the original phone number. The especially interesting and egregious part is that when I sign in, it does 2FA with the new phone number.”

The Mastodon user PeteMayo said they recreated their Experian account twice this week, the second time by supplying a random landline number.

“The only difference: it asked me FIVE questions about my personal history (last time it only asked three) before proclaiming, ‘Welcome back, Pete!,’ and granting full access,” @PeteMayo wrote. “I feel silly saving my password for Experian; may as well just make a new account every time.”

![]()

I was fortunate in that whoever hijacked my account did not also thaw my credit freeze. Or if they did, they politely froze it again when they were done. But I fully expect my Experian account will be hijacked yet again unless Experian makes some important changes to its authentication process.

It boggles the mind that these fundamental authentication weaknesses have been allowed to persist for so long at Experian, which already has a horrible track record in this regard.

In December 2022, KrebsOnSecurity alerted Experian that identity thieves had worked out a remarkably simple way to bypass its security and access any consumer’s full credit report — armed with nothing more than a person’s name, address, date of birth, and Social Security number. Experian fixed the glitch, and acknowledged that it persisted for nearly seven weeks, between Nov. 9, 2022 and Dec. 26, 2022.

In April 2021, KrebsOnSecurity revealed how identity thieves were exploiting lax authentication on Experian’s PIN retrieval page to unfreeze consumer credit files. In those cases, Experian failed to send any notice via email when a freeze PIN was retrieved, nor did it require the PIN to be sent to an email address already associated with the consumer’s account.

A few days after that April 2021 story, KrebsOnSecurity broke the news that an Experian API was exposing the credit scores of most Americans.

More greatest hits from Experian:

2022: Class Action Targets Experian Over Account Security

2017: Experian Site Can Give Anyone Your Credit Freeze PIN

2015: Experian Breach Affects 15 Million Customers

2015: Experian Breach Tied to NY-NJ ID Theft Ring

2015: At Experian, Security Attrition Amid Acquisitions

2015: Experian Hit With Class Action Over ID Theft Service

2014: Experian Lapse Allowed ID Theft Service Access to 200 Million Consumer Records

2013: Experian Sold Consumer Data to ID Theft Service

On Dec. 23, 2022, KrebsOnSecurity alerted big-three consumer credit reporting bureau Experian that identity thieves had worked out how to bypass its security and access any consumer’s full credit report — armed with nothing more than a person’s name, address, date of birth, and Social Security number. Experian fixed the glitch, but remained silent about the incident for a month. This week, however, Experian acknowledged that the security failure persisted for nearly seven weeks, between Nov. 9, 2022 and Dec. 26, 2022.

![]()

The tip about the Experian weakness came from Jenya Kushnir, a security researcher living in Ukraine who said he discovered the method being used by identity thieves after spending time on Telegram chat channels dedicated to cybercrime.

Normally, Experian’s website will ask a series of multiple-choice questions about one’s financial history, as a way of validating the identity of the person requesting the credit report. But Kushnir said the crooks learned they could bypass those questions and trick Experian into giving them access to anyone’s credit report, just by editing the address displayed in the browser URL bar at a specific point in Experian’s identity verification process.

When I tested Kushnir’s instructions on my own identity at Experian, I found I was able to see my report even though Experian’s website told me it didn’t have enough information to validate my identity. A security researcher friend who tested it at Experian found she also could bypass Experian’s four or five multiple-choice security questions and go straight to her full credit report at Experian.

Experian acknowledged receipt of my Dec. 23 report four days later on Dec. 27, a day after Kushnir’s method stopped working on Experian’s website (the exploit worked as long as you came to Experian’s website via annualcreditreport.com — the site mandated to provide a free copy of your credit report from each of the major bureaus once a year).

Experian never did respond to official requests for comment on that story. But earlier this week, I received an otherwise unhelpful letter via snail mail from Experian (see image above), which stated that the weakness we reported persisted between Nov. 9, 2022 and Dec. 26, 2022.

“During this time period, we experienced an isolated technical issue where a security feature may not have functioned,” Experian explained.

It’s not entirely clear whether Experian sent me this paper notice because they legally had to, or if they felt I deserved a response in writing and thought maybe they’d kill two birds with one stone. But it’s pretty crazy that it took them a full month to notify me about the potential impact of a security failure that I notified them about.

It’s also a little nuts that Experian didn’t simply include a copy of my current credit report along with this letter, which is confusingly worded and reads like they suspect someone other than me may have been granted access to my credit report without any kind of screening or authorization.

After all, if I hadn’t authorized the request for my credit file that apparently prompted this letter (I had), that would mean the thieves already had my report. Shouldn’t I be granted the same visibility into my own credit file as them?

Instead, their woefully inadequate letter once again puts the onus on me to wait endlessly on hold for an Experian representative over the phone, or sign up for a free year’s worth of Experian monitoring my credit report.

As it stands, using Kushnir’s exploit was the only time I’ve ever been able to get Experian’s website to cough up a copy of my credit report. To make matters worse, a majority of the information in that credit report is not mine. So I’ve got that to look forward to.

If there is a silver lining here, I suppose that if I were Experian, I probably wouldn’t want to show Brian Krebs his credit file either. Because it’s clear this company has no idea who I really am. And in a weird, kind of sad way I guess, that makes me happy.

For thoughts on what you can do to minimize your victimization by and overall worth to the credit bureaus, see this section of the most recent Experian story.

Identity thieves have been exploiting a glaring security weakness in the website of Experian, one of the big three consumer credit reporting bureaus. Normally, Experian requires that those seeking a copy of their credit report successfully answer several multiple choice questions about their financial history. But until the end of 2022, Experian’s website allowed anyone to bypass these questions and go straight to the consumer’s report. All that was needed was the person’s name, address, birthday and Social Security number.

The vulnerability in Experian’s website was exploitable after one applied to see their credit file via annualcreditreport.com.

In December, KrebsOnSecurity heard from Jenya Kushnir, a security researcher living in Ukraine who said he discovered the method being used by identity thieves after spending time on Telegram chat channels dedicated to the cashing out of compromised identities.

“I want to try and help to put a stop to it and make it more difficult for [ID thieves] to access, since [Experian is] not doing shit and regular people struggle,” Kushnir wrote in an email to KrebsOnSecurity explaining his motivations for reaching out. “If somehow I can make small change and help to improve this, inside myself I can feel that I did something that actually matters and helped others.”

Kushnir said the crooks learned they could trick Experian into giving them access to anyone’s credit report, just by editing the address displayed in the browser URL bar at a specific point in Experian’s identity verification process.

Following Kushnir’s instructions, I sought a copy of my credit report from Experian via annualcreditreport.com — a website that is required to provide all Americans with a free copy of their credit report from each of the three major reporting bureaus, once per year.

Annualcreditreport.com begins by asking for your name, address, SSN and birthday. After I supplied that and told Annualcreditreport.com I wanted my report from Experian, I was taken to Experian.com to complete the identity verification process.

![]()

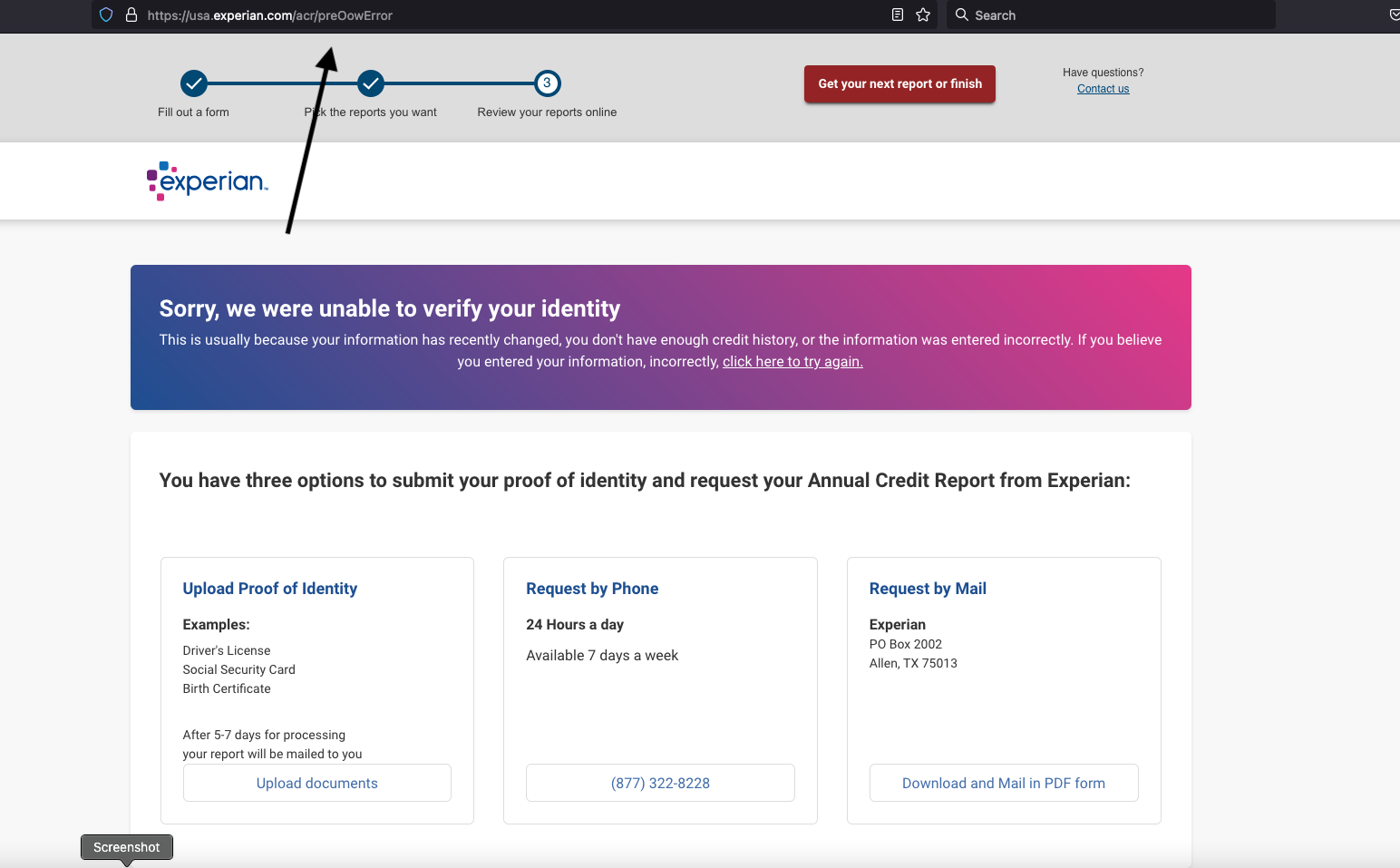

Normally at this point, Experian’s website would present four or five multiple-guess questions, such as “Which of the following addresses have you lived at?”

Kushnir told me that when the questions page loads, you simply change the last part of the URL from “/acr/oow/” to “/acr/report,” and the site would display the consumer’s full credit report.

But when I tried to get my report from Experian via annualcreditreport.com, Experian’s website said it didn’t have enough information to validate my identity. It wouldn’t even show me the four multiple-guess questions. Experian said I had three options for a free credit report at this point: Mail a request along with identity documents, call a phone number for Experian, or upload proof of identity via the website.

But that didn’t stop Experian from showing me my full credit report after I changed the Experian URL as Kushnir had instructed — modifying the error page’s trailing URL from “/acr/OcwError” to simply “/acr/report”.

Experian’s website then immediately displayed my entire credit file.

Even though Experian said it couldn’t tell that I was actually me, it still coughed up my report. And thank goodness it did. The report contains so many errors that it’s probably going to take a good deal of effort on my part to straighten out.

Now I know why Experian has NEVER let me view my own file via their website. For example, there were four phone numbers on my Experian credit file: Only one of them was mine, and that one hasn’t been mine for ages.

I was so dumbfounded by Experian’s incompetence that I asked a close friend and trusted security source to try the method on her identity file at Experian. Sure enough, when she got to the part where Experian asked questions, changing the last part of the URL in her address bar to “/report” bypassed the questions and immediately displayed her full credit report. Her report also was replete with errors.

KrebsOnSecurity shared Kushnir’s findings with Experian on Dec. 23, 2022. On Dec. 27, 2022, Experian’s PR team acknowledged receipt of my Dec. 23 notification, but the company has so far ignored multiple requests for comment or clarification.

By the time Experian confirmed receipt of my report, the “exploit” Kushnir said he learned from the identity thieves on Telegram had been patched and no longer worked. But it remains unclear how long Experian’s website was making it so easy to access anyone’s credit report.

In response to information shared by KrebsOnSecurity, Senator Ron Wyden (D-Ore.) said he was disappointed — but not at all surprised — to hear about yet another cybersecurity lapse at Experian.

“The credit bureaus are poorly regulated, act as if they are above the law and have thumbed their noses at Congressional oversight,” Wyden said in a written statement. “Just last year, Experian ignored repeated briefing requests from my office after you revealed another cybersecurity lapse the company.”

Sen. Wyden’s quote above references a story published here in July 2022, which broke the news that identity thieves were hijacking consumer accounts at Experian.com just by signing up as them at Experian once more, supplying the target’s static, personal information (name, DoB/SSN, address) but a different email address.

From interviews with multiple victims who contacted KrebsOnSecurity after that story, it emerged that Experian’s own customer support representatives were actually telling consumers who got locked out of their Experian accounts to recreate their accounts using their personal information and a new email address. This was Experian’s advice even for people who’d just explained that this method was what identity thieves had used to lock them in out in the first place.

Clearly, Experian found it simpler to respond this way, rather than acknowledging the problem and addressing the root causes (lazy authentication and abhorrent account recovery practices). It’s also worth mentioning that reports of hijacked Experian.com accounts persisted into late 2022. That screw-up has since prompted a class action lawsuit against Experian.

Sen. Wyden said the Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB) need to do much more to protect Americans from screw-ups by the credit bureaus.

“If they don’t believe they have the authority to do so, they should endorse legislation like my Mind Your Own Business Act, which gives the FTC power to set tough mandatory cybersecurity standards for companies like Experian,” Wyden said.

Sadly, none of this is terribly shocking behavior for Experian, which has shown itself a completely negligent custodian of obscene amounts of highly sensitive consumer information.

In April 2021, KrebsOnSecurity revealed how identity thieves were exploiting lax authentication on Experian’s PIN retrieval page to unfreeze consumer credit files. In those cases, Experian failed to send any notice via email when a freeze PIN was retrieved, nor did it require the PIN to be sent to an email address already associated with the consumer’s account.

A few days after that April 2021 story, KrebsOnSecurity broke the news that an Experian API was exposing the credit scores of most Americans.

It’s bad enough that we can’t really opt out of companies like Experian making $2.6 billion each quarter collecting and selling gobs of our personal and financial information. But there has to be some meaningful accountability when these monopolistic companies engage in negligent and reckless behavior with the very same consumer data that feeds their quarterly profits. Or when security and privacy shortcuts are found to be intentional, like for cost-saving reasons.

And as we saw with Equifax’s consolidated class-action settlement in response to letting state-sponsored hackers from China steal data on nearly 150 million Americans back in 2017, class-actions and more laughable “free credit monitoring” services from the very same companies that created the problem aren’t going to cut it.

It is easy to adopt a defeatist attitude with the credit bureaus, who often foul things up royally even for consumers who are quite diligent about watching their consumer credit files and disputing any inaccuracies.

But there are some concrete steps that everyone can take which will dramatically lower the risk that identity thieves will ruin your financial future. And happily, most of these steps have the side benefit of costing the credit bureaus money, or at least causing the data they collect about you to become less valuable over time.

The first step is awareness. Find out what these companies are saying about you behind your back. Keep in mind that — fair or not — your credit score as collectively determined by these bureaus can affect whether you get that loan, apartment, or job. In that context, even small, unintentional errors that are unrelated to identity theft can have outsized consequences for consumers down the road.

Each bureau is required to provide a free copy of your credit report every year. The easiest way to get yours is through annualcreditreport.com.

Some consumers report that this site never works for them, and that each bureau will insist they don’t have enough information to provide a report. I am definitely in this camp. Thankfully, a financial institution that I already have a relationship with offers the ability to view your credit file through them. Your mileage on this front may vary, and you may end up having to send copies of your identity documents through the mail or website.

When you get your report, look for anything that isn’t yours, and then document and file a dispute with the corresponding credit bureau. And after you’ve reviewed your report, set a calendar reminder to recur every four months, reminding you it’s time to get another free copy of your credit file.

If you haven’t already done so, consider making 2023 the year that you freeze your credit files at the three major reporting bureaus, including Experian, Equifax and TransUnion. It is now free to people in all 50 U.S. states to place a security freeze on their credit files. It is also free to do this for your partner and/or your dependents.

Freezing your credit means no one who doesn’t already have a financial relationship with you can view your credit file, making it unlikely that potential creditors will grant new lines of credit in your name to identity thieves. Freezing your credit file also means Experian and its brethren can no longer sell peeks at your credit history to others.

Anytime you wish to apply for new credit or a new job, or open an account at a utility or communications provider, you can quickly thaw a freeze on your credit file, and set it to freeze automatically again after a specified length of time.

Please don’t confuse a credit freeze (a.k.a. “security freeze”) with the alternative that the bureaus will likely steer you towards when you ask for a freeze: “Credit lock” services.

The bureaus pitch these credit lock services as a way for consumers to easily toggle their credit file availability with push of a button on a mobile app, but they do little to prevent the bureaus from continuing to sell your information to others.

My advice: Ignore the lock services, and just freeze your credit files already.

One final note. Frequent readers here will have noticed that I’ve criticized these so-called “knowledge-based authentication” or KBA questions that Experian’s website failed to ask as part of its consumer verification process.

KrebsOnSecurity has long assailed KBA as weak authentication because the questions and answers are drawn largely from consumer records that are public and easily accessible to organized identity theft groups.

That said, given that these KBA questions appear to be the ONLY thing standing between me and my Experian credit report, it seems like maybe they should at least take care to ensure that those questions actually get asked.

Our personal and professional lives are becoming increasingly intertwined with the online world. Regular internet usage has made us all prone to cyber-security risks. You leave a digital footprint every time you use the internet, which is a trace of all your online activities.

When you create new accounts or subscribe to different websites, you give them explicit (or implicit, through their family of apps or subsidiary websites) access to your personal and credit card information. In other cases, websites might track basic information without your knowledge, such as your location and search history.

There is an industry of data brokers specifically dedicated to keeping track of user data, packaging it, and supplying it to tech companies who use it to run targeted ads and enhance on-platform user experience. Given the widespread use of the internet and exponential improvements in technology, data has become a valuable commodity — creating a need for the sale and purchase of user data.

This article discusses how data brokers sell your personal information and how you can minimize risk.

Data brokers are companies that aggregate user information from various sources on the internet. They collect, collate, package, and sometimes even analyze this data to create a holistic and coherent version of you online. This data is then supplied to tech companies to fuel their third-party advertising-centered business models.

Companies interested in buying data include but are not limited to:

These companies and social media platforms use your data to better understand target demographics and the content with which they interact. While the practice isn’t unethical in and of itself (personalizing user experiences and creating more convenient UIs are usually cited as the primary reasons for it), it does make your data vulnerable to malicious attacks targeted toward big-tech servers.

Most of your online activities are related. Devices like your phone, laptop, tablets, and even fitness watches are linked to each other. Moreover, you might use one email ID for various accounts and subscriptions. This online interconnectedness makes it easier for data brokers to create a cohesive user profile.

Mobile phone apps are the most common way for data brokerage firms to collect your data. You might have countless apps for various purposes, such as financial transactions, health and fitness, or social media.

A number of these apps usually fall under the umbrella of the same or subsidiary family of apps, all of which work toward collecting and supplying data to big tech platforms. Programs like Google’s AdSense make it easier for developers to monetize their apps in exchange for the user information they collect.

Data brokers also collect data points like your home address, full name, Social Security number, phone number, and date of birth. They have automated scraping tools to quickly collect relevant information from public profiles.[Text Wrapping Break]

Lastly, data brokers can gather data from other third parties that track your cookies or even place trackers or cookies on your browsers. Cookies are small data files that track your online activities when visiting different websites. They track your IP address and browsing history, which third parties can exploit. Cookies are also the reason you see personalized ads and products.

Data brokers collate your private information into one package and sell it to “people search” websites like Spokeo or TruePeopleSearch. You or a tech business can use these websites to search for people and get extensive consumer data. People search sites also contain public records like voter registration information, marriage records, and birth certificates. This data is used for consumer research and large-scale data analysis.

Next, marketing and sales firms are some of data brokers’ biggest clients. These companies purchase massive data sets from data brokers to research your data profile. They have advanced algorithms to segregate users into various consumer groups and target you specifically. Their predictive algorithms can suggest personalized ads and products to generate higher lead generation and conversation percentages for their clients.

We tend to accept the terms and conditions that various apps ask us to accept without thinking twice or reading the fine print. You probably cannot proceed without letting the app track certain data or giving your personal information. To a certain extent, we trade some of our privacy for convenience. This becomes public information, and apps and data brokers collect, track, and use our data however they please while still complying with the law.

There is no comprehensive privacy law in the U.S. on a federal level. This allows data brokers to collect personal information and condense it into marketing insights. While not all methods of gathering private data are legal, it is difficult to track the activities of data brokers online (especially on the dark web). As technology advances, there are also easier ways to harvest and exploit data.

Vermont and California have already enacted laws to regulate the data brokerage industry. In 2018, Vermont passed the country’s first data broker legislation. This requires data brokers to register annually with the Secretary of State and provide information about their data collection activities, opt-out policies, purchaser credentialing practices, and data breaches.

California has passed similar laws to make data brokering a more transparent industry. For risk mitigation of data brokerage, the Federal Trade Commission (FTC) has published reports and provided recommendations to Congress to reduce the engagement of data broker firms. Giving individuals the right to opt-out of the sale of their personal data is a step toward a more rigorous law regarding data privacy.

Some data brokers let you remove your information from their websites. There are also extensive guides available online that list the method by which you can opt-out of some of the biggest data brokering firms. For example, a guide by Griffin Boyce, the systems administrator at Harvard University’s Berkman Klein Center for Internet and Society, provides detailed information on how to opt-out of a long list of data broker companies.

Acxiom, LLC is one of the largest data brokering firms and has collected data for approximately 68% of people who have an online presence. You can opt-out of their data collection either through their website or by calling them directly.

Epsilon Data Management is another big player in the data broker industry that operates as a marketing service and marketing analytics company. You can opt-out of their website through various methods such as by email, phone, and mail. Credit rating agencies like Experian and Equifax are also notorious for collecting your data. Similarly, you can opt-out through their websites or by calling them.

McAfee is a pioneer in providing online and offline data protection to its customers. We offer numerous cybersecurity services for keeping your information private and secure.

With regard to data brokers, we enable users to do a personal data clean-up. Cleaning up your personal data online may be a difficult task, as it requires you to reach out to multiple data brokers and opt out. Instead, sign up for McAfee’s Personal Data Cleanup feature to do a convenient and thorough personal data clean-up. We will search for traces of your personal data and assist in getting it removed.

The post How Data Brokers Sell Your Identity appeared first on McAfee Blog.

Twice in the past month KrebsOnSecurity has heard from readers who had their accounts at big-three credit bureau Experian hacked and updated with a new email address that wasn’t theirs. In both cases the readers used password managers to select strong, unique passwords for their Experian accounts. Research suggests identity thieves were able to hijack the accounts simply by signing up for new accounts at Experian using the victim’s personal information and a different email address.

![]()

John Turner is a software engineer based in Salt Lake City. Turner said he created the account at Experian in 2020 to place a security freeze on his credit file, and that he used a password manager to select and store a strong, unique password for his Experian account.

Turner said that in early June 2022 he received an email from Experian saying the email address on his account had been changed. Experian’s password reset process was useless at that point because any password reset links would be sent to the new (impostor’s) email address.

An Experian support person Turner reached via phone after a lengthy hold time asked for his Social Security Number (SSN) and date of birth, as well as his account PIN and answers to his secret questions. But the PIN and secret questions had already been changed by whoever re-signed up as him at Experian.

“I was able to answer the credit report questions successfully, which authenticated me to their system,” Turner said. “At that point, the representative read me the current stored security questions and PIN, and they were definitely not things I would have used.”

Turner said he was able to regain control over his Experian account by creating a new account. But now he’s wondering what else he could do to prevent another account compromise.

“The most frustrating part of this whole thing is that I received multiple ‘here’s your login information’ emails later that I attributed to the original attackers coming back and attempting to use the ‘forgot email/username’ flow, likely using my SSN and DOB, but it didn’t go to their email that they were expecting,” Turner said. “Given that Experian doesn’t support two-factor authentication of any kind — and that I don’t know how they were able to get access to my account in the first place — I’ve felt very helpless ever since.”

Arthur Rishi is a musician and co-executive director of the Boston Landmarks Orchestra. Rishi said he recently discovered his Experian account had been hijacked after receiving an alert from his credit monitoring service (not Experian’s) that someone had tried to open an account in his name at JPMorgan Chase.

Rishi said the alert surprised him because his credit file at Experian was frozen at the time, and Experian did not notify him about any activity on his account. Rishi said Chase agreed to cancel the unauthorized account application, and even rescinded its credit inquiry (each credit pull can ding your credit score slightly).

But he never could get anyone from Experian’s support to answer the phone, despite spending what seemed like eternity trying to progress through the company’s phone-based system. That’s when Rishi decided to see if he could create a new account for himself at Experian.

“I was able to open a new account at Experian starting from scratch, using my SSN, date of birth and answering some really basic questions, like what kind of car did you take out a loan for, or what city did you used to live in,’ Rishi said.

Upon completing the sign-up, Rishi noticed that his credit was unfrozen.

Like Turner, Rishi is now worried that identity thieves will just hijack his Experian account once more, and that there is nothing he can do to prevent such a scenario. For now, Rishi has decided to pay Experian $25.99 a month to more closely monitor his account for suspicious activity. Even using the paid Experian service, there were no additional multi-factor authentication options available, although he said Experian did send a one-time code to his phone via SMS recently when he logged on.

“Experian now sometimes does require MFA for me if I use a new browser or have my VPN on,” Rishi said, but he’s not sure if Experian’s free service would have operated differently.

“I get so angry when I think about all this,” he said. “I have no confidence this won’t happen again.”

In a written statement, Experian suggested that what happened to Rishi and Turner was not a normal occurrence, and that its security and identity verification practices extend beyond what is visible to the user.

“We believe these are isolated incidents of fraud using stolen consumer information,” Experian’s statement reads. “Specific to your question, once an Experian account is created, if someone attempts to create a second Experian account, our systems will notify the original email on file.”

“We go beyond reliance on personally identifiable information (PII) or a consumer’s ability to answer knowledge-based authentication questions to access our systems,” the statement continues. “We do not disclose additional processes for obvious security reasons; however, our data and analytical capabilities verify identity elements across multiple data sources and are not visible to the consumer. This is designed to create a more positive experience for our consumers and to provide additional layers of protection. We take consumer privacy and security seriously, and we continually review our security processes to guard against constant and evolving threats posed by fraudsters.”

KrebsOnSecurity sought to replicate Turner and Rishi’s experience — to see if Experian would allow me to re-create my account using my personal information but a different email address. The experiment was done from a different computer and Internet address than the one that created the original account years ago.

After providing my Social Security Number (SSN), date of birth, and answering several multiple choice questions whose answers are derived almost entirely from public records, Experian promptly changed the email address associated with my credit file. It did so without first confirming that new email address could respond to messages, or that the previous email address approved the change.

Experian’s system then sent an automated message to the original email address on file, saying the account’s email address had been changed. The only recourse Experian offered in the alert was to sign in, or send an email to an Experian inbox that replies with the message, “this email address is no longer monitored.”

![]()

After that, Experian prompted me to select new secret questions and answers, as well as a new account PIN — effectively erasing the account’s previously chosen PIN and recovery questions. Once I’d changed the PIN and security questions, Experian’s site helpfully reminded me that I have a security freeze on file, and would I like to remove or temporarily lift the security freeze?

To be clear, Experian does have a business unit that sells one-time password services to businesses. While Experian’s system did ask for a mobile number when I signed up a second time, at no time did that number receive a notification from Experian. Also, I could see no option in my account to enable multi-factor authentication for all logins.

How does Experian differ from the practices of Equifax and TransUnion, the other two big consumer credit reporting bureaus? When KrebsOnSecurity tried to re-create an existing account at TransUnion using my Social Security number, TransUnion rejected the application, noting that I already had an account and prompting me to proceed through its lost password flow. The company also appears to send an email to the address on file asking to validate account changes.

Likewise, trying to recreate an existing account at Equifax using personal information tied to my existing account prompts Equifax’s systems to report that I already have an account, and to use their password reset process (which involves sending a verification email to the address on file).

KrebsOnSecurity has long urged readers in the United States to place a security freeze on their files with the three major credit bureaus. With a freeze in place, potential creditors can’t pull your credit file, which makes it very unlikely anyone will be granted new lines of credit in your name. I’ve also advised readers to plant their flag at the three major bureaus, to prevent identity thieves from creating an account for you and assuming control over your identity.

The experiences of Rishi, Turner and this author suggest Experian’s practices currently undermine both of those proactive security measures. Even so, having an active account at Experian may be the only way you find out when crooks have assumed your identity. Because at least then you should receive an email from Experian saying they gave your identity to someone else.

In April 2021, KrebsOnSecurity revealed how identity thieves were exploiting lax authentication on Experian’s PIN retrieval page to unfreeze consumer credit files. In those cases, Experian failed to send any notice via email when a freeze PIN was retrieved, nor did it require the PIN to be sent to an email address already associated with the consumer’s account.

A few days after that April 2021 story, KrebsOnSecurity broke the news that an Experian API was exposing the credit scores of most Americans.

Emory Roan, policy counsel for the Privacy Rights Clearinghouse, said Experian not offering multi-factor authentication for consumer accounts is inexcusable in 2022.

“They compound the problem by gating the recovery process with information that’s likely available or inferable from third party data brokers, or that could have been exposed in previous data breaches,” Roan said. “Experian is one of the largest Consumer Reporting Agencies in the country, trusted as one of the few essential players in a credit system Americans are forced to be part of. For them to not offer consumers some form of (free) MFA is baffling and reflects extremely poorly on Experian.”

Nicholas Weaver, a researcher for the International Computer Science Institute at University of California, Berkeley, said Experian has no real incentive to do things right on the consumer side of its business. That is, he said, unless Experian’s customers — banks and other lenders — choose to vote with their feet because too many people with frozen credit files are having to deal with unauthorized applications for new credit.

“The actual customers of the credit service don’t realize how much worse Experian is, and this isn’t the first time Experian has screwed up horribly,” Weaver said. “Experian is part of a triopoly, and I’m sure this is costing their actual customers money, because if you have a credit freeze that gets lifted and somebody loans against it, it’s the lender who eats that fraud cost.”

And unlike consumers, he said, lenders do have a choice in which of the triopoly handles their credit checks.

“I do think it’s important to point out that their real customers do have a choice, and they should switch to TransUnion and Equifax,” he added.

More greatest hits from Experian:

2017: Experian Site Can Give Anyone Your Credit Freeze PIN

2015: Experian Breach Affects 15 Million Customers

2015: Experian Breach Tied to NY-NJ ID Theft Ring

2015: At Experian, Security Attrition Amid Acquisitions

2015: Experian Hit With Class Action Over ID Theft Service

2014: Experian Lapse Allowed ID Theft Service Access to 200 Million Consumer Records

2013: Experian Sold Consumer Data to ID Theft Service

Update, 10:32 a.m.: Updated the story to clarify that while Experian does sometimes ask users to enter a one-time code sent via SMS to the number on file, there does not appear to be any option to enable this on all logins.