Microsoft on Tuesday released updates to quash at least 74 security bugs in its Windows operating systems and software. Two of those flaws are already being actively attacked, including an especially severe weakness in Microsoft Outlook that can be exploited without any user interaction.

![]()

The Outlook vulnerability (CVE-2023-23397) affects all versions of Microsoft Outlook from 2013 to the newest. Microsoft said it has seen evidence that attackers are exploiting this flaw, which can be done without any user interaction by sending a booby-trapped email that triggers automatically when retrieved by the email server — before the email is even viewed in the Preview Pane.

While CVE-2023-23397 is labeled as an “Elevation of Privilege” vulnerability, that label doesn’t accurately reflect its severity, said Kevin Breen, director of cyber threat research at Immersive Labs.

Known as an NTLM relay attack, it allows an attacker to get someone’s NTLM hash [Windows account password] and use it in an attack commonly referred to as “Pass The Hash.”

“The vulnerability effectively lets the attacker authenticate as a trusted individual without having to know the person’s password,” Breen said. “This is on par with an attacker having a valid password with access to an organization’s systems.”

Security firm Rapid7 points out that this bug affects self-hosted versions of Outlook like Microsoft 365 Apps for Enterprise, but Microsoft-hosted online services like Microsoft 365 are not vulnerable.

The other zero-day flaw being actively exploited in the wild — CVE-2023-24880 — is a “Security Feature Bypass” in Windows SmartScreen, part of Microsoft’s slate of endpoint protection tools.

Patch management vendor Action1 notes that the exploit for this bug is low in complexity and requires no special privileges. But it does require some user interaction, and can’t be used to gain access to private information or privileges. However, the flaw can allow other malicious code to run without being detected by SmartScreen reputation checks.

Dustin Childs, head of threat awareness at Trend Micro’s Zero Day Initiative, said CVE-2023-24880 allows attackers to create files that would bypass Mark of the Web (MOTW) defenses.

“Protective measures like SmartScreen and Protected View in Microsoft Office rely on MOTW, so bypassing these makes it easier for threat actors to spread malware via crafted documents and other infected files that would otherwise be stopped by SmartScreen,” Childs said.

Seven other vulnerabilities Microsoft patched this week earned its most-dire “critical” severity label, meaning the updates address security holes that could be exploited to give the attacker full, remote control over a Windows host with little or no interaction from the user.

Also this week, Adobe released eight patches addressing a whopping 105 security holes across a variety of products, including Adobe Photoshop, Cold Fusion, Experience Manager, Dimension, Commerce, Magento, Substance 3D Stager, Cloud Desktop Application, and Illustrator.

For a more granular rundown on the updates released today, see the SANS Internet Storm Center roundup. If today’s updates cause any stability or usability issues in Windows, AskWoody.com will likely have the lowdown on that.

Please consider backing up your data and/or imaging your system before applying any updates. And feel free to sound off in the comments if you experience any problems as a result of these patches.

The Biden administration today issued its vision for beefing up the nation’s collective cybersecurity posture, including calls for legislation establishing liability for software products and services that are sold with little regard for security. The White House’s new national cybersecurity strategy also envisions a more active role by cloud providers and the U.S. military in disrupting cybercriminal infrastructure, and it names China as the single biggest cyber threat to U.S. interests.

![]()

The strategy says the White House will work with Congress and the private sector to develop legislation that would prevent companies from disavowing responsibility for the security of their software products or services.

Coupled with this stick would be a carrot: An as-yet-undefined “safe harbor framework” that would lay out what these companies could do to demonstrate that they are making cybersecurity a central concern of their design and operations.

“Any such legislation should prevent manufacturers and software publishers with market power from fully disclaiming liability by contract, and establish higher standards of care for software in specific high-risk scenarios,” the strategy explains. “To begin to shape standards of care for secure software development, the Administration will drive the development of an adaptable safe harbor framework to shield from liability companies that securely develop and maintain their software products and services.”

Brian Fox, chief technology officer and founder of the software supply chain security firm Sonatype, called the software liability push a landmark moment for the industry.

“Market forces are leading to a race to the bottom in certain industries, while contract law allows software vendors of all kinds to shield themselves from liability,” Fox said. “Regulations for other industries went through a similar transformation, and we saw a positive result — there’s now an expectation of appropriate due care, and accountability for those who fail to comply. Establishing the concept of safe harbors allows the industry to mature incrementally, leveling up security best practices in order to retain a liability shield, versus calling for sweeping reform and unrealistic outcomes as previous regulatory attempts have.”

In 2012 (approximately three national cyber strategies ago), then director of the U.S. National Security Agency (NSA) Keith Alexander made headlines when he remarked that years of successful cyber espionage campaigns from Chinese state-sponsored hackers represented “the greatest transfer of wealth in history.”

The document released today says the People’s Republic of China (PRC) “now presents the broadest, most active, and most persistent threat to both government and private sector networks,” and says China is “the only country with both the intent to reshape the international order and, increasingly, the economic, diplomatic, military, and technological power to do so.”

Many of the U.S. government’s efforts to restrain China’s technology prowess involve ongoing initiatives like the CHIPS Act, a new law signed by President Biden last year that sets aside more than $50 billion to expand U.S.-based semiconductor manufacturing and research and to make the U.S. less dependent on foreign suppliers; the National Artificial Intelligence Initiative; and the National Strategy to Secure 5G.

As the maker of most consumer gizmos with a computer chip inside, China is also the source of an incredible number of low-cost Internet of Things (IoT) devices that are not only poorly secured, but are probably more accurately described as insecure by design.

The Biden administration said it would continue its previously announced plans to develop a system of labeling that could be applied to various IoT products and give consumers some idea of how secure the products may be. But it remains unclear how those labels might apply to products made by companies outside of the United States.

One could convincingly make the case that the world has witnessed yet another historic transfer of wealth and trade secrets over the past decade — in the form of ransomware and data ransom attacks by Russia-based cybercriminal syndicates, as well as Russian intelligence agency operations like the U.S. government-wide Solar Winds compromise.

![]()

On the ransomware front, the White House strategy seems to focus heavily on building the capability to disrupt the digital infrastructure used by adversaries that are threatening vital U.S. cyber interests. The document points to the 2021 takedown of the Emotet botnet — a cybercrime machine that was heavily used by multiple Russian ransomware groups — as a model for this activity, but says those disruptive operations need to happen faster and more often.

To that end, the Biden administration says it will expand the capacity of the National Cyber Investigative Joint Task Force (NCIJTF), the primary federal agency for coordinating cyber threat investigations across law enforcement agencies, the intelligence community, and the Department of Defense.

“To increase the volume and speed of these integrated disruption campaigns, the Federal Government must further develop technological and organizational platforms that enable continuous, coordinated operations,” the strategy observes. “The NCIJTF will expand its capacity to coordinate takedown and disruption campaigns with greater speed, scale, and frequency. Similarly, DoD and the Intelligence Community are committed to bringing to bear their full range of complementary authorities to disruption campaigns.”

The strategy anticipates the U.S. government working more closely with cloud and other Internet infrastructure providers to quickly identify malicious use of U.S.-based infrastructure, share reports of malicious use with the government, and make it easier for victims to report abuse of these systems.

“Given the interest of the cybersecurity community and digital infrastructure owners and operators in continuing this approach, we must sustain and expand upon this model so that collaborative disruption operations can be carried out on a continuous basis,” the strategy argues. “Threat specific collaboration should take the form of nimble, temporary cells, comprised of a small number of trusted operators, hosted and supported by a relevant hub. Using virtual collaboration platforms, members of the cell would share information bidirectionally and work rapidly to disrupt adversaries.”

But here, again, there is a carrot-and-stick approach: The administration said it is taking steps to implement Executive Order (EO) 13984 –issued by the Trump administration in January 2021 — which requires cloud providers to verify the identity of foreign persons using their services.

“All service providers must make reasonable attempts to secure the use of their infrastructure against abuse or other criminal behavior,” the strategy states. “The Administration will prioritize adoption and enforcement of a risk-based approach to cybersecurity across Infrastructure-as-a-Service providers that addresses known methods and indicators of malicious activity including through implementation of EO 13984.”

Ted Schlein, founding partner of the cybersecurity venture capital firm Ballistic Ventures, said how this gets implemented will determine whether it can be effective.

“Adversaries know the NSA, which is the elite portion of the nation’s cyber defense, cannot monitor U.S.-based infrastructure, so they just use U.S.-based cloud infrastructure to perpetrate their attacks,” Schlein said. “We have to fix this. I believe some of this section is a bit pollyannaish, as it assumes a bad actor with a desire to do a bad thing will self-identify themselves, as the major recommendation here is around KYC (‘know your customer’).”

One brief but interesting section of the strategy titled “Explore a Federal Cyber Insurance Backdrop” contemplates the government’s liability and response to a too-big-to-fail scenario or “catastrophic cyber incident.”

“We will explore how the government can stabilize insurance markets against catastrophic risk to drive better cybersecurity practices and to provide market certainty when catastrophic events do occur,” the strategy reads.

When the Bush administration released the first U.S. national cybersecurity strategy 20 years ago after the 9/11 attacks, the popular term for that same scenario was a “digital Pearl Harbor,” and there was a great deal of talk then about how the cyber insurance market would soon help companies shore up their cybersecurity practices.

In the wake of countless ransomware intrusions, many companies now hold cybersecurity insurance to help cover the considerable costs of responding to such intrusions. Leaving aside the question of whether insurance coverage has helped companies improve security, what happens if every one of these companies has to make a claim at the same time?

The notion of a Digital Pearl Harbor incident struck many experts at the time as a hyperbolic justification for expanding the government’s digital surveillance capabilities, and an overstatement of the capabilities of our adversaries. But back in 2003, most of the world’s companies didn’t host their entire business in the cloud.

Today, nobody questions the capabilities, goals and outcomes of dozens of nation-state level cyber adversaries. And these days, a catastrophic cyber incident could be little more than an extended, simultaneous outage at multiple cloud providers.

The full national cybersecurity strategy is available from the White House website (PDF).

Image: Shutterstock.com

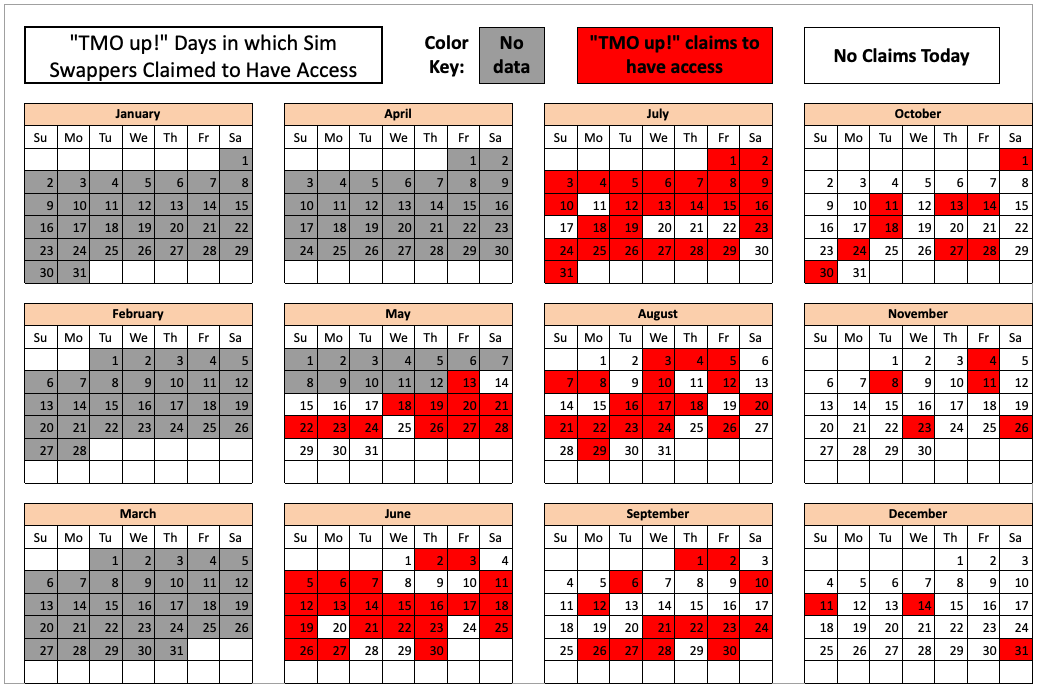

Three different cybercriminal groups claimed access to internal networks at communications giant T-Mobile in more than 100 separate incidents throughout 2022, new data suggests. In each case, the goal of the attackers was the same: Phish T-Mobile employees for access to internal company tools, and then convert that access into a cybercrime service that could be hired to divert any T-Mobile user’s text messages and phone calls to another device.

The conclusions above are based on an extensive analysis of Telegram chat logs from three distinct cybercrime groups or actors that have been identified by security researchers as particularly active in and effective at “SIM-swapping,” which involves temporarily seizing control over a target’s mobile phone number.

Countless websites and online services use SMS text messages for both password resets and multi-factor authentication. This means that stealing someone’s phone number often can let cybercriminals hijack the target’s entire digital life in short order — including access to any financial, email and social media accounts tied to that phone number.

All three SIM-swapping entities that were tracked for this story remain active in 2023, and they all conduct business in open channels on the instant messaging platform Telegram. KrebsOnSecurity is not naming those channels or groups here because they will simply migrate to more private servers if exposed publicly, and for now those servers remain a useful source of intelligence about their activities.

Each advertises their claimed access to T-Mobile systems in a similar way. At a minimum, every SIM-swapping opportunity is announced with a brief “Tmobile up!” or “Tmo up!” message to channel participants. Other information in the announcements includes the price for a single SIM-swap request, and the handle of the person who takes the payment and information about the targeted subscriber.

The information required from the customer of the SIM-swapping service includes the target’s phone number, and the serial number tied to the new SIM card that will be used to receive text messages and phone calls from the hijacked phone number.

Initially, the goal of this project was to count how many times each entity claimed access to T-Mobile throughout 2022, by cataloging the various “Tmo up!” posts from each day and working backwards from Dec. 31, 2022.

But by the time we got to claims made in the middle of May 2022, completing the rest of the year’s timeline seemed unnecessary. The tally shows that in the last seven-and-a-half months of 2022, these groups collectively made SIM-swapping claims against T-Mobile on 104 separate days — often with multiple groups claiming access on the same days.

The 104 days in the latter half of 2022 in which different known SIM-swapping groups claimed access to T-Mobile employee tools.

KrebsOnSecurity shared a large amount of data gathered for this story with T-Mobile. The company declined to confirm or deny any of these claimed intrusions. But in a written statement, T-Mobile said this type of activity affects the entire wireless industry.

“And we are constantly working to fight against it,” the statement reads. “We have continued to drive enhancements that further protect against unauthorized access, including enhancing multi-factor authentication controls, hardening environments, limiting access to data, apps or services, and more. We are also focused on gathering threat intelligence data, like what you have shared, to help further strengthen these ongoing efforts.”

While it is true that each of these cybercriminal actors periodically offer SIM-swapping services for other mobile phone providers — including AT&T, Verizon and smaller carriers — those solicitations appear far less frequently in these group chats than T-Mobile swap offers. And when those offers do materialize, they are considerably more expensive.

The prices advertised for a SIM-swap against T-Mobile customers in the latter half of 2022 ranged between USD $1,000 and $1,500, while SIM-swaps offered against AT&T and Verizon customers often cost well more than twice that amount.

![]()

To be clear, KrebsOnSecurity is not aware of specific SIM-swapping incidents tied to any of these breach claims. However, the vast majority of advertisements for SIM-swapping claims against T-Mobile tracked in this story had two things in common that set them apart from random SIM-swapping ads on Telegram.

First, they included an offer to use a mutually trusted “middleman” or escrow provider for the transaction (to protect either party from getting scammed). More importantly, the cybercriminal handles that were posting ads for SIM-swapping opportunities from these groups generally did so on a daily or near-daily basis — often teasing their upcoming swap events in the hours before posting a “Tmo up!” message announcement.

In other words, if the crooks offering these SIM-swapping services were ripping off their customers or claiming to have access that they didn’t, this would be almost immediately obvious from the responses of the more seasoned and serious cybercriminals in the same chat channel.

There are plenty of people on Telegram claiming to have SIM-swap access at major telecommunications firms, but a great many such offers are simply four-figure scams, and any pretenders on this front are soon identified and banned (if not worse).

One of the groups that reliably posted “Tmo up!” messages to announce SIM-swap availability against T-Mobile customers also reliably posted “Tmo down!” follow-up messages announcing exactly when their claimed access to T-Mobile employee tools was discovered and revoked by the mobile giant.

A review of the timestamps associated with this group’s incessant “Tmo up” and “Tmo down” posts indicates that while their claimed access to employee tools usually lasted less than an hour, in some cases that access apparently went undiscovered for several hours or even days.

How could these SIM-swapping groups be gaining access to T-Mobile’s network as frequently as they claim? Peppered throughout the daily chit-chat on their Telegram channels are solicitations for people urgently needed to serve as “callers,” or those who can be hired to social engineer employees over the phone into navigating to a phishing website and entering their employee credentials.

Allison Nixon is chief research officer for the New York City-based cybersecurity firm Unit 221B. Nixon said these SIM-swapping groups will typically call employees on their mobile devices, pretend to be someone from the company’s IT department, and then try to get the person on the other end of the line to visit a phishing website that mimics the company’s employee login page.

Nixon argues that many people in the security community tend to discount the threat from voice phishing attacks as somehow “low tech” and “low probability” threats.

“I see it as not low-tech at all, because there are a lot of moving parts to phishing these days,” Nixon said. “You have the caller who has the employee on the line, and the person operating the phish kit who needs to spin it up and down fast enough so that it doesn’t get flagged by security companies. Then they have to get the employee on that phishing site and steal their credentials.”

In addition, she said, often there will be yet another co-conspirator whose job it is to use the stolen credentials and log into employee tools. That person may also need to figure out how to make their device pass “posture checks,” a form of device authentication that some companies use to verify that each login is coming only from employer-issued phones or laptops.

For aspiring criminals with little experience in scam calling, there are plenty of sample call transcripts available on these Telegram chat channels that walk one through how to impersonate an IT technician at the targeted company — and how to respond to pushback or skepticism from the employee. Here’s a snippet from one such tutorial that appeared recently in one of the SIM-swapping channels:

“Hello this is James calling from Metro IT department, how’s your day today?”

(yea im doing good, how r u)

i’m doing great, thank you for asking

i’m calling in regards to a ticket we got last week from you guys, saying you guys were having issues with the network connectivity which also interfered with [Microsoft] Edge, not letting you sign in or disconnecting you randomly. We haven’t received any updates to this ticket ever since it was created so that’s why I’m calling in just to see if there’s still an issue or not….”

The TMO UP data referenced above, combined with comments from the SIM-swappers themselves, indicate that while many of their claimed accesses to T-Mobile tools in the middle of 2022 lasted hours on end, both the frequency and duration of these events began to steadily decrease as the year wore on.

![]()

T-Mobile declined to discuss what it may have done to combat these apparent intrusions last year. However, one of the groups began to complain loudly in late October 2022 that T-Mobile must have been doing something that was causing their phished access to employee tools to die very soon after they obtained it.

One group even remarked that they suspected T-Mobile’s security team had begun monitoring their chats.

Indeed, the timestamps associated with one group’s TMO UP/TMO DOWN notices show that their claimed access was often limited to less than 15 minutes throughout November and December of 2022.

Whatever the reason, the calendar graphic above clearly shows that the frequency of claimed access to T-Mobile decreased significantly across all three SIM-swapping groups in the waning weeks of 2022.

T-Mobile US reported revenues of nearly $80 billion last year. It currently employs more than 71,000 people in the United States, any one of whom can be a target for these phishers.

T-Mobile declined to answer questions about what it may be doing to beef up employee authentication. But Nicholas Weaver, a researcher and lecturer at University of California, Berkeley’s International Computer Science Institute, said T-Mobile and all the major wireless providers should be requiring employees to use physical security keys for that second factor when logging into company resources.

A U2F device made by Yubikey.

“These breaches should not happen,” Weaver said. “Because T-Mobile should have long ago issued all employees security keys and switched to security keys for the second factor. And because security keys provably block this style of attack.”

The most commonly used security keys are inexpensive USB-based devices. A security key implements a form of multi-factor authentication known as Universal 2nd Factor (U2F), which allows the user to complete the login process simply by inserting the USB key and pressing a button on the device. The key works without the need for any special software drivers.

The allure of U2F devices for multi-factor authentication is that even if an employee who has enrolled a security key for authentication tries to log in at an impostor site, the company’s systems simply refuse to request the security key if the user isn’t on their employer’s legitimate website, and the login attempt fails. Thus, the second factor cannot be phished, either over the phone or Internet.

Nixon said one confounding aspect of SIM-swapping is that these criminal groups tend to recruit teenagers to do their dirty work.

“A huge reason this problem has been allowed to spiral out of control is because children play such a prominent role in this form of breach,” Nixon said.

Nixon said SIM-swapping groups often advertise low-level jobs on places like Roblox and Minecraft, online games that are extremely popular with young adolescent males.

“Statistically speaking, that kind of recruiting is going to produce a lot of people who are underage,” she said. “They recruit children because they’re naive, you can get more out of them, and they have legal protections that other people over 18 don’t have.”

For example, she said, even when underage SIM-swappers are arrested, the offenders tend to go right back to committing the same crimes as soon as they’re released.

In January 2023, T-Mobile disclosed that a “bad actor” stole records on roughly 37 million current customers, including their name, billing address, email, phone number, date of birth, and T-Mobile account number.

In August 2021, T-Mobile acknowledged that hackers made off with the names, dates of birth, Social Security numbers and driver’s license/ID information on more than 40 million current, former or prospective customers who applied for credit with the company. That breach came to light after a hacker began selling the records on a cybercrime forum.

In the shadow of such mega-breaches, any damage from the continuous attacks by these SIM-swapping groups can seem insignificant by comparison. But Nixon says it’s a mistake to dismiss SIM-swapping as a low volume problem.

“Logistically, you may only be able to get a few dozen or a hundred SIM-swaps in a day, but you can pick any customer you want across their entire customer base,” she said. “Just because a targeted account takeover is low volume doesn’t mean it’s low risk. These guys have crews that go and identify people who are high net worth individuals and who have a lot to lose.”

Nixon said another aspect of SIM-swapping that causes cybersecurity defenders to dismiss the threat from these groups is the perception that they are full of low-skilled “script kiddies,” a derisive term used to describe novice hackers who rely mainly on point-and-click hacking tools.

“They underestimate these actors and say this person isn’t technically sophisticated,” she said. “But if you’re rolling around in millions worth of stolen crypto currency, you can buy that sophistication. I know for a fact some of these compromises were at the hands of these ‘script kiddies,’ but they’re not ripping off other people’s scripts so much as hiring people to make scripts for them. And they don’t care what gets the job done, as long as they get to steal the money.”

Web hosting giant GoDaddy made headlines this month when it disclosed that a multi-year breach allowed intruders to steal company source code, siphon customer and employee login credentials, and foist malware on customer websites. Media coverage understandably focused on GoDaddy’s admission that it suffered three different cyberattacks over as many years at the hands of the same hacking group. But it’s worth revisiting how this group typically got in to targeted companies: By calling employees and tricking them into navigating to a phishing website.

![]()

In a filing with the U.S. Securities and Exchange Commission (SEC), GoDaddy said it determined that the same “sophisticated threat actor group” was responsible for three separate intrusions, including:

-March 2020: A spear-phishing attack on a GoDaddy employee compromised the hosting login credentials of approximately 28,000 GoDaddy customers, as well as login credentials for a small number employees;

-November 2021: A compromised GoDaddy password let attackers steal source code and information tied to 1.2 million customers, including website administrator passwords, sFTP credentials, and private SSL keys;

-December 2022: Hackers gained access to and installed malware on GoDaddy’s cPanel hosting servers that “intermittently redirected random customer websites to malicious sites.”

“Based on our investigation, we believe these incidents are part of a multi-year campaign by a sophisticated threat actor group that, among other things, installed malware on our systems and obtained pieces of code related to some services within GoDaddy,” the company stated in its SEC filing.

What else do we know about the cause of these incidents? We don’t know much about the source of the November 2021 incident, other than GoDaddy’s statement that it involved a compromised password, and that it took about two months for the company to detect the intrusion. GoDaddy has not disclosed the source of the breach in December 2022 that led to malware on some customer websites.

But we do know the March 2020 attack was precipitated by a spear-phishing attack against a GoDaddy employee. GoDaddy described the incident at the time in general terms as a social engineering attack, but one of its customers affected by that March 2020 breach actually spoke to one of the hackers involved.

The hackers were able to change the Domain Name System (DNS) records for the transaction brokering site escrow.com so that it pointed to an address in Malaysia that was host to just a few other domains, including the then brand-new phishing domain servicenow-godaddy[.]com.

The general manager of Escrow.com found himself on the phone with one of the GoDaddy hackers, after someone who claimed they worked at GoDaddy called and said they needed him to authorize some changes to the account.

In reality, the caller had just tricked a GoDaddy employee into giving away their credentials, and he could see from the employee’s account that Escrow.com required a specific security procedure to complete a domain transfer.

The general manager of Escrow.com said he suspected the call was a scam, but decided to play along for about an hour — all the while recording the call and coaxing information out of the scammer.

“This guy had access to the notes, and knew the number to call,” to make changes to the account, the CEO of Escrow.com told KrebsOnSecurity. “He was literally reading off the tickets to the notes of the admin panel inside GoDaddy.”

About halfway through this conversation — after being called out by the general manager as an imposter — the hacker admitted that he was not a GoDaddy employee, and that he was in fact part of a group that enjoyed repeated success with social engineering employees at targeted companies over the phone.

Absent from GoDaddy’s SEC statement is another spate of attacks in November 2020, in which unknown intruders redirected email and web traffic for multiple cryptocurrency services that used GoDaddy in some capacity.

It is possible this incident was not mentioned because it was the work of yet another group of intruders. But in response to questions from KrebsOnSecurity at the time, GoDaddy said that incident also stemmed from a “limited” number of GoDaddy employees falling for a sophisticated social engineering scam.

“As threat actors become increasingly sophisticated and aggressive in their attacks, we are constantly educating employees about new tactics that might be used against them and adopting new security measures to prevent future attacks,” GoDaddy said in a written statement back in 2020.

Voice phishing or “vishing” attacks typically target employees who work remotely. The phishers will usually claim that they’re calling from the employer’s IT department, supposedly to help troubleshoot some issue. The goal is to convince the target to enter their credentials at a website set up by the attackers that mimics the organization’s corporate email or VPN portal.

Experts interviewed for an August 2020 story on a steep rise in successful voice phishing attacks said there are generally at least two people involved in each vishing scam: One who is social engineering the target over the phone, and another co-conspirator who takes any credentials entered at the phishing page — including multi-factor authentication codes shared by the victim — and quickly uses them to log in to the company’s website.

The attackers are usually careful to do nothing with the phishing domain until they are ready to initiate a vishing call to a potential victim. And when the attack or call is complete, they disable the website tied to the domain.

This is key because many domain registrars will only respond to external requests to take down a phishing website if the site is live at the time of the abuse complaint. This tactic also can stymie efforts by companies that focus on identifying newly-registered phishing domains before they can be used for fraud.

A U2F device made by Yubikey.

GoDaddy’s latest SEC filing indicates the company had nearly 7,000 employees as of December 2022. In addition, GoDaddy contracts with another 3,000 people who work full-time for the company via business process outsourcing companies based primarily in India, the Philippines and Colombia.

Many companies now require employees to supply a one-time password — such as one sent via SMS or produced by a mobile authenticator app — in addition to their username and password when logging in to company assets online. But both SMS and app-based codes can be undermined by phishing attacks that simply request this information in addition to the user’s password.

One multifactor option — physical security keys — appears to be immune to these advanced scams. The most commonly used security keys are inexpensive USB-based devices. A security key implements a form of multi-factor authentication known as Universal 2nd Factor (U2F), which allows the user to complete the login process simply by inserting the USB device and pressing a button on the device. The key works without the need for any special software drivers.

The allure of U2F devices for multi-factor authentication is that even if an employee who has enrolled a security key for authentication tries to log in at an impostor site, the company’s systems simply refuse to request the security key if the user isn’t on their employer’s legitimate website, and the login attempt fails. Thus, the second factor cannot be phished, either over the phone or Internet.

In July 2018, Google disclosed that it had not had any of its 85,000+ employees successfully phished on their work-related accounts since early 2017, when it began requiring all employees to use physical security keys in place of one-time codes.

Millions of Americans receiving food assistance benefits just earned a new right that they can’t yet enforce: The right to be reimbursed if funds on their Electronic Benefit Transfer (EBT) cards are stolen by card skimming devices secretly installed at cash machines and grocery store checkout lanes.

![]()

On December 29, 2022, President Biden signed into law the Consolidated Appropriations Act of 2023, which — for the first time ever — includes provisions for the replacement of stolen EBT benefits. This is a big deal because in 2022, organized crime groups began massively targeting EBT accounts — often emptying affected accounts at ATMs immediately after the states disperse funds each month.

EBT cards can be used along with a personal identification number (PIN) to pay for goods at participating stores, and to withdraw cash from an ATM. However, EBT cards differ from debit cards issued to most Americans in two important ways. First, most states do not equip EBT cards with smart chip technology, which can make the cards more difficult and expensive for skimming thieves to clone.

More critically, EBT participants traditionally have had little hope of recovering food assistance funds when their cards were copied by card-skimming devices and used for fraud. That’s because while the EBT programs are operated by individually by the states, those programs are funded by the U.S. Department of Agriculture (USDA), which until late last year was barred from reimbursing states for stolen EBT funds.

The protections passed in the 2023 Appropriations Act allow states to use federal funds to replace stolen EBT benefits, and they permit states to seek reimbursement for any skimmed EBT funds they may have replaced from their own coffers (dating back to Oct. 1, 2022).

But first, all 50 states must each submit a plan for how they are going to protect and replace food benefits stolen via card skimming. Guidance for the states in drafting those plans was issued by the USDA on Jan. 31 (PDF), and states that don’t get them done before Feb. 27, 2023 risk losing the ability to be reimbursed for EBT fraud losses.

Deborah Harris is a staff attorney at The Massachusetts Law Reform Institute (MLRI), a nonprofit legal assistance organization that has closely tracked the EBT skimming epidemic. In November 2022, the MLRI filed a class-action lawsuit against Massachusetts on behalf of thousands of low-income families who were collectively robbed of more than $1 million in food assistance benefits by card skimming devices secretly installed at cash machines and grocery store checkout lanes across the state.

Harris said she’s pleased that the USDA guidelines were issued so promptly, and that the guidance for states was not overly prescriptive. For example, some security experts have suggested that adding contactless capability to EBT cards could help participants avoid skimming devices altogether. But Harris said contactless cards do not require a PIN, which is the only thing that stops EBT cards from being drained at the ATM when a participant’s card is lost or stolen.

Then again, nothing in the guidance even mentions chip-based cards, or any other advice for improving the physical security of EBT cards. Rather, it suggests states should seek to develop the capability to perform basic fraud detection and alerting on suspicious transactions, such as when an EBT card that is normally used only in one geographic area suddenly is used to withdraw cash at an ATM halfway across the country.

“Besides having the states move fast to approve their plans, we’d also like to see a focused effort to move states from magstripe-only cards to chip, and also assisting states to develop the algorithms that will enable them to identify likely incidents of stolen benefits,” Harris said.

Harris said Massachusetts has begun using algorithms to look for these suspicious transaction patterns throughout its EBT network, and now has the ability to alert households and verify transactions. But she said most states do not have this capability.

“We have heard that other states aren’t currently able to do that,” Harris said. “But encouraging states to more affirmatively identify instances of likely theft and assisting with the claims and verification process is critical. Most households can’t do that on their own, and in Massachusetts it’s very hard for a person to get a copy of their transaction history. Some states can do that through third-party apps, but something so basic should not be on the burden of EBT households.”

Some states aren’t waiting for direction from the federal government to beef up EBT card security. Like Maryland, which identified more than 1,400 households hit by EBT skimming attacks last year — a tenfold increase over 2021.

Advocates for EBT beneficiaries in Maryland are backing Senate Bill 401 (PDF), which would require the use of chip technology and ongoing monitoring for suspicious activity (a hearing on SB401 is scheduled in the Maryland Senate Finance Commission for Thursday, Feb. 23, at 1 p.m.).

Michelle Salomon Madaio is a director at the Homeless Persons Representation Project, a legal assistance organization based in Silver Spring, Md. Madaio said the bill would require the state Department of Human Services to replace skimmed benefits, not only after the bill goes into effect but also retroactively from January 2020 to the present.

Madaio said the bill also would require the state to monitor for patterns of suspicious activity on EBT cards, and to develop a mechanism to contact potentially affected households.

“For most of the skimming victims we’ve worked with, the fraudulent transactions would be pretty easy to spot because they mostly happened in the middle of the night or out of state, or both,” Madaio said. “To make matters worse, a lot of families whose benefits were scammed then incurred late fees on many other things as a result.”

It is not difficult to see why organized crime groups have pounced on EBT cards as easy money. In most traditional payment card transactions, there are usually several parties that have a financial interest in minimizing fraud and fraud losses, including the bank that issued the card, the card network (Visa, MasterCard, Discover, etc.), and the merchant.

But that infrastructure simply does not exist within state EBT programs, and it certainly isn’t a thing at the inter-state level. What that means is that the vast majority of EBT cards have zero fraud controls, which is exactly what continues to make them so appealing to thieves.

For now, the only fraud controls available to most EBT cardholders include being especially paranoid about where they use their cards, and frequently changing their PINs.

According to USDA guidance issued prior to the passage of the appropriations act, EBT cardholders should consider changing their card PIN at least once a month.

“By changing PINs frequently, at least monthly, and doing so before benefit issuance dates, households can minimize their risk of stolen benefits from a previously skimmed EBT card,” the USDA advised.

T-Mobile today disclosed a data breach affecting tens of millions of customer accounts, its second major data exposure in as many years. In a filing with federal regulators, T-Mobile said an investigation determined that someone abused its systems to harvest subscriber data tied to approximately 37 million current customer accounts.

Image: customink.com

In a filing today with the U.S. Securities and Exchange Commission, T-Mobile said a “bad actor” abused an application programming interface (API) to hoover up data on roughly 37 million current postpaid and prepaid customer accounts. The data stolen included customer name, billing address, email, phone number, date of birth, T-Mobile account number, as well as information on the number of customer lines and plan features.

APIs are essentially instructions that allow applications to access data and interact with web databases. But left improperly secured, these APIs can be leveraged by malicious actors to mass-harvest information stored in those databases. In October, mobile provider Optus disclosed that hackers abused a poorly secured API to steal data on 10 million customers in Australia.

T-Mobile said it first learned of the incident on Jan. 5, 2023, and that an investigation determined the bad actor started abusing the API beginning around Nov. 25, 2022. The company says it is in the process of notifying affected customers, and that no customer payment card data, passwords, Social Security numbers, driver’s license or other government ID numbers were exposed.

In August 2021, T-Mobile acknowledged that hackers made off with the names, dates of birth, Social Security numbers and driver’s license/ID information on more than 40 million current, former or prospective customers who applied for credit with the company. That breach came to light after a hacker began selling the records on a cybercrime forum.

Last year, T-Mobile agreed to pay $500 million to settle all class action lawsuits stemming from the 2021 breach. The company pledged to spend $150 million of that money toward beefing up its own cybersecurity.

In its filing with the SEC, T-Mobile suggested it was going to take years to fully realize the benefits of those cybersecurity improvements, even as it claimed that protecting customer data remains a top priority.

“As we have previously disclosed, in 2021, we commenced a substantial multi-year investment working with leading external cybersecurity experts to enhance our cybersecurity capabilities and transform our approach to cybersecurity,” the filing reads. “We have made substantial progress to date, and protecting our customers’ data remains a top priority.”

Despite this being the second major customer data spill in as many years, T-Mobile told the SEC the company does not expect this latest breach to have a material impact on its operations.

While that may seem like a daring thing to say in a data breach disclosure affecting a significant portion of your active customer base, consider that T-Mobile reported revenues of nearly $20 billion in the third quarter of 2022 alone. In that context, a few hundred million dollars every couple of years to make the class action lawyers go away is a drop in the bucket.

The settlement related to the 2021 breach says T-Mobile will make $350 million available to customers who file a claim. But here’s the catch: If you were affected by that 2021 breach and you haven’t filed a claim yet, please know that you have only three more days to do that.

If you were a T-Mobile customer affected by the 2021 incident, it is likely that T-Mobile has already made several efforts to notify you of your eligibility to file a claim, which includes a payout of at least $25, with the possibility of more for those who can document direct costs associated with the breach. OpenClassActions.com says the filing deadline is Jan. 23, 2023.

“If you opt for a cash payment you will receive an estimated $25.00,” the site explains. “If you reside in California, you will receive an estimated $100.00. Out of pocket losses can be reimbursed for up to $25,000.00. The amount that you claim from T-Mobile will be determined by the class action administrator based on how many people file a legitimate and timely claim form.”

There are currently no signs that hackers are selling this latest data haul from T-Mobile, but if the past is any teacher much of it will wind up posted online soon. It is a safe bet that scammers will use some of this information to target T-Mobile users with phishing messages, account takeovers and harassment.

T-Mobile customers should fully expect to see phishers taking advantage of public concern over the breach to impersonate the company — and possibly even send messages that include the recipient’s compromised account details to make the communications look more legitimate.

Data stolen and exposed in this breach may also be used for identity theft. Credit monitoring and ID theft protection services can help you recover from having your identity stolen, but most will do nothing to stop the ID theft from happening. If you want the maximum control over who should be able to view your credit or grant new lines of credit in your name, then a security freeze is your best option.

Regardless of which mobile provider you patronize, please consider removing your phone number from as many online accounts as you can. Many online services require you to provide a phone number upon registering an account, but in many cases that number can be removed from your profile afterwards.

Why do I suggest this? Many online services allow users to reset their passwords just by clicking a link sent via SMS, and this unfortunately widespread practice has turned mobile phone numbers into de facto identity documents. Which means losing control over your phone number thanks to an unauthorized SIM swap or mobile number port-out, divorce, job termination or financial crisis can be devastating.

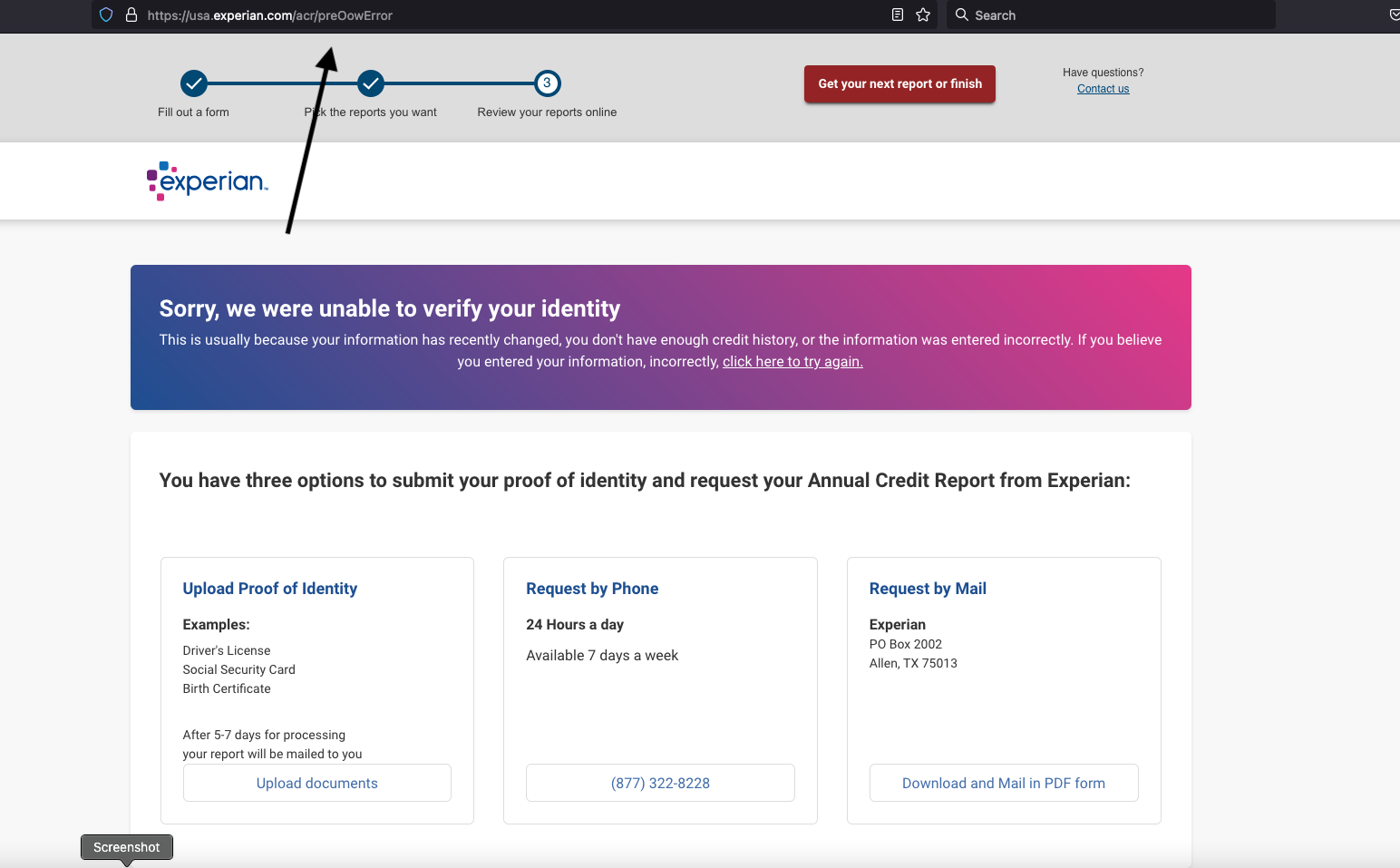

Identity thieves have been exploiting a glaring security weakness in the website of Experian, one of the big three consumer credit reporting bureaus. Normally, Experian requires that those seeking a copy of their credit report successfully answer several multiple choice questions about their financial history. But until the end of 2022, Experian’s website allowed anyone to bypass these questions and go straight to the consumer’s report. All that was needed was the person’s name, address, birthday and Social Security number.

The vulnerability in Experian’s website was exploitable after one applied to see their credit file via annualcreditreport.com.

In December, KrebsOnSecurity heard from Jenya Kushnir, a security researcher living in Ukraine who said he discovered the method being used by identity thieves after spending time on Telegram chat channels dedicated to the cashing out of compromised identities.

“I want to try and help to put a stop to it and make it more difficult for [ID thieves] to access, since [Experian is] not doing shit and regular people struggle,” Kushnir wrote in an email to KrebsOnSecurity explaining his motivations for reaching out. “If somehow I can make small change and help to improve this, inside myself I can feel that I did something that actually matters and helped others.”

Kushnir said the crooks learned they could trick Experian into giving them access to anyone’s credit report, just by editing the address displayed in the browser URL bar at a specific point in Experian’s identity verification process.

Following Kushnir’s instructions, I sought a copy of my credit report from Experian via annualcreditreport.com — a website that is required to provide all Americans with a free copy of their credit report from each of the three major reporting bureaus, once per year.

Annualcreditreport.com begins by asking for your name, address, SSN and birthday. After I supplied that and told Annualcreditreport.com I wanted my report from Experian, I was taken to Experian.com to complete the identity verification process.

![]()

Normally at this point, Experian’s website would present four or five multiple-guess questions, such as “Which of the following addresses have you lived at?”

Kushnir told me that when the questions page loads, you simply change the last part of the URL from “/acr/oow/” to “/acr/report,” and the site would display the consumer’s full credit report.

But when I tried to get my report from Experian via annualcreditreport.com, Experian’s website said it didn’t have enough information to validate my identity. It wouldn’t even show me the four multiple-guess questions. Experian said I had three options for a free credit report at this point: Mail a request along with identity documents, call a phone number for Experian, or upload proof of identity via the website.

But that didn’t stop Experian from showing me my full credit report after I changed the Experian URL as Kushnir had instructed — modifying the error page’s trailing URL from “/acr/OcwError” to simply “/acr/report”.

Experian’s website then immediately displayed my entire credit file.

Even though Experian said it couldn’t tell that I was actually me, it still coughed up my report. And thank goodness it did. The report contains so many errors that it’s probably going to take a good deal of effort on my part to straighten out.

Now I know why Experian has NEVER let me view my own file via their website. For example, there were four phone numbers on my Experian credit file: Only one of them was mine, and that one hasn’t been mine for ages.

I was so dumbfounded by Experian’s incompetence that I asked a close friend and trusted security source to try the method on her identity file at Experian. Sure enough, when she got to the part where Experian asked questions, changing the last part of the URL in her address bar to “/report” bypassed the questions and immediately displayed her full credit report. Her report also was replete with errors.

KrebsOnSecurity shared Kushnir’s findings with Experian on Dec. 23, 2022. On Dec. 27, 2022, Experian’s PR team acknowledged receipt of my Dec. 23 notification, but the company has so far ignored multiple requests for comment or clarification.

By the time Experian confirmed receipt of my report, the “exploit” Kushnir said he learned from the identity thieves on Telegram had been patched and no longer worked. But it remains unclear how long Experian’s website was making it so easy to access anyone’s credit report.

In response to information shared by KrebsOnSecurity, Senator Ron Wyden (D-Ore.) said he was disappointed — but not at all surprised — to hear about yet another cybersecurity lapse at Experian.

“The credit bureaus are poorly regulated, act as if they are above the law and have thumbed their noses at Congressional oversight,” Wyden said in a written statement. “Just last year, Experian ignored repeated briefing requests from my office after you revealed another cybersecurity lapse the company.”

Sen. Wyden’s quote above references a story published here in July 2022, which broke the news that identity thieves were hijacking consumer accounts at Experian.com just by signing up as them at Experian once more, supplying the target’s static, personal information (name, DoB/SSN, address) but a different email address.

From interviews with multiple victims who contacted KrebsOnSecurity after that story, it emerged that Experian’s own customer support representatives were actually telling consumers who got locked out of their Experian accounts to recreate their accounts using their personal information and a new email address. This was Experian’s advice even for people who’d just explained that this method was what identity thieves had used to lock them in out in the first place.

Clearly, Experian found it simpler to respond this way, rather than acknowledging the problem and addressing the root causes (lazy authentication and abhorrent account recovery practices). It’s also worth mentioning that reports of hijacked Experian.com accounts persisted into late 2022. That screw-up has since prompted a class action lawsuit against Experian.

Sen. Wyden said the Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB) need to do much more to protect Americans from screw-ups by the credit bureaus.

“If they don’t believe they have the authority to do so, they should endorse legislation like my Mind Your Own Business Act, which gives the FTC power to set tough mandatory cybersecurity standards for companies like Experian,” Wyden said.

Sadly, none of this is terribly shocking behavior for Experian, which has shown itself a completely negligent custodian of obscene amounts of highly sensitive consumer information.

In April 2021, KrebsOnSecurity revealed how identity thieves were exploiting lax authentication on Experian’s PIN retrieval page to unfreeze consumer credit files. In those cases, Experian failed to send any notice via email when a freeze PIN was retrieved, nor did it require the PIN to be sent to an email address already associated with the consumer’s account.

A few days after that April 2021 story, KrebsOnSecurity broke the news that an Experian API was exposing the credit scores of most Americans.

It’s bad enough that we can’t really opt out of companies like Experian making $2.6 billion each quarter collecting and selling gobs of our personal and financial information. But there has to be some meaningful accountability when these monopolistic companies engage in negligent and reckless behavior with the very same consumer data that feeds their quarterly profits. Or when security and privacy shortcuts are found to be intentional, like for cost-saving reasons.

And as we saw with Equifax’s consolidated class-action settlement in response to letting state-sponsored hackers from China steal data on nearly 150 million Americans back in 2017, class-actions and more laughable “free credit monitoring” services from the very same companies that created the problem aren’t going to cut it.

It is easy to adopt a defeatist attitude with the credit bureaus, who often foul things up royally even for consumers who are quite diligent about watching their consumer credit files and disputing any inaccuracies.

But there are some concrete steps that everyone can take which will dramatically lower the risk that identity thieves will ruin your financial future. And happily, most of these steps have the side benefit of costing the credit bureaus money, or at least causing the data they collect about you to become less valuable over time.

The first step is awareness. Find out what these companies are saying about you behind your back. Keep in mind that — fair or not — your credit score as collectively determined by these bureaus can affect whether you get that loan, apartment, or job. In that context, even small, unintentional errors that are unrelated to identity theft can have outsized consequences for consumers down the road.

Each bureau is required to provide a free copy of your credit report every year. The easiest way to get yours is through annualcreditreport.com.

Some consumers report that this site never works for them, and that each bureau will insist they don’t have enough information to provide a report. I am definitely in this camp. Thankfully, a financial institution that I already have a relationship with offers the ability to view your credit file through them. Your mileage on this front may vary, and you may end up having to send copies of your identity documents through the mail or website.

When you get your report, look for anything that isn’t yours, and then document and file a dispute with the corresponding credit bureau. And after you’ve reviewed your report, set a calendar reminder to recur every four months, reminding you it’s time to get another free copy of your credit file.

If you haven’t already done so, consider making 2023 the year that you freeze your credit files at the three major reporting bureaus, including Experian, Equifax and TransUnion. It is now free to people in all 50 U.S. states to place a security freeze on their credit files. It is also free to do this for your partner and/or your dependents.

Freezing your credit means no one who doesn’t already have a financial relationship with you can view your credit file, making it unlikely that potential creditors will grant new lines of credit in your name to identity thieves. Freezing your credit file also means Experian and its brethren can no longer sell peeks at your credit history to others.

Anytime you wish to apply for new credit or a new job, or open an account at a utility or communications provider, you can quickly thaw a freeze on your credit file, and set it to freeze automatically again after a specified length of time.

Please don’t confuse a credit freeze (a.k.a. “security freeze”) with the alternative that the bureaus will likely steer you towards when you ask for a freeze: “Credit lock” services.

The bureaus pitch these credit lock services as a way for consumers to easily toggle their credit file availability with push of a button on a mobile app, but they do little to prevent the bureaus from continuing to sell your information to others.

My advice: Ignore the lock services, and just freeze your credit files already.

One final note. Frequent readers here will have noticed that I’ve criticized these so-called “knowledge-based authentication” or KBA questions that Experian’s website failed to ask as part of its consumer verification process.

KrebsOnSecurity has long assailed KBA as weak authentication because the questions and answers are drawn largely from consumer records that are public and easily accessible to organized identity theft groups.

That said, given that these KBA questions appear to be the ONLY thing standing between me and my Experian credit report, it seems like maybe they should at least take care to ensure that those questions actually get asked.

Millions of people likely just received an email or snail mail notice saying they’re eligible to claim a class action payment in connection with the 2017 megabreach at consumer credit bureau Equifax. Given the high volume of reader inquiries about this, it seemed worth pointing out that while this particular offer is legit (if paltry), scammers are likely to soon capitalize on public attention to the settlement money.

One reader’s copy of their Equifax Breach Settlement letter. They received a check for $6.97.

In 2017, Equifax disclosed a massive, extended data breach that led to the theft of Social Security Numbers, dates of birth, addresses and other personal information on nearly 150 million people. Following a public breach response perhaps best described as a giant dumpster fire, the big-three consumer credit reporting bureau was quickly hit with nearly two dozen class-action lawsuits.

In exchange for resolving all outstanding class action claims against it, Equifax in 2019 agreed to a settlement that includes up to $425 million to help people affected by the breach.

Affected consumers were eligible to apply for at least three years of credit monitoring via all three major bureaus simultaneously, including Equifax, Experian and TransUnion. Or, if you didn’t want to take advantage of the credit monitoring offers, you could opt for a cash payment of up to $125.

The settlement also offered reimbursement for the time you may have spent remedying identity theft or misuse of your personal information caused by the breach, or purchasing credit monitoring or credit reports. This was capped at 20 total hours at $25 per hour ($500), with total cash reimbursement payments not to exceed $20,000 per consumer.

Those who did file a claim probably started receiving emails or other communications earlier this year from the Equifax Breach Settlement Fund, which has been messaging class participants about methods of collecting their payments.

How much each recipient receives appears to vary quite a bit, but probably most people will have earned a payment on the smaller end of that $125 scale — like less than $10. Those who received higher amounts likely spent more time documenting actual losses and/or explaining how the breach affected them personally.

So far this week, KrebsOnSecurity has received at least 20 messages from readers seeking more information about these notices. Some readers shared copies of letters they got in the mail along with a paper check from the Equifax Breach Settlement Fund (see screenshot above).

Others said they got emails from the Equifax Breach Settlement domain that looked like an animated greeting card offering instructions on how to redeem a virtual prepaid card.

![]()

If you received one of these settlement emails and are wary about clicking the included links (good for you, by the way), copy the redemption code and paste it into the search box at myprepaidcenter.com/redeem. Successfully completing the card application requires accepting a prepaid MasterCard agreement (PDF).

The website for the settlement — equifaxbreachsettlement.com — also includes a lookup tool that lets visitors check whether they were affected by the breach; it requires your last name and the last six digits of your Social Security Number.

But be aware that phishers and other scammers are likely to take advantage of increased public awareness of the payouts to snooker people. Tim Helming, security evangelist at DomainTools.com, today flagged several new domains that mimic the name of the real Equifax Breach Settlement website and do not appear to be defensively registered by Equifax, including equifaxbreechsettlement[.]com, equifaxbreachsettlementbreach[.]com, and equifaxsettlements[.]co.

In February 2020, the U.S. Justice Department indicted four Chinese officers of the People’s Liberation Army (PLA) for perpetrating the 2017 Equifax hack. DOJ officials said the four men were responsible for carrying out the largest theft of sensitive personal information by state-sponsored hackers ever recorded.

Equifax surpassed Wall Street’s expectations in its most recent quarterly earnings: The company reported revenues of $1.24 billion for the quarter ending September 2022.

Of course, most of those earnings come from Equifax’s continued legal ability to buy and sell eye-popping amounts of financial and personal data on U.S. consumers. As one of the three major credit bureaus, Equifax collects and packages information about your credit, salary, and employment history. It tracks how many credit cards you have, how much money you owe, and how you pay your bills. Each company creates a credit report about you, and then sells this report to businesses who are deciding whether to give you credit.

Americans currently have no legal right to opt out of this data collection and trade. But you can and also should freeze your credit, which by the way can make your credit profile less profitable for companies like Equifax — because they make money every time some potential creditor wants a peek inside your financial life. Also, it’s probably a good idea to freeze the credit of your children and/or dependents as well. It’s free on both counts.

Ransomware groups are constantly devising new methods for infecting victims and convincing them to pay up, but a couple of strategies tested recently seem especially devious. The first centers on targeting healthcare organizations that offer consultations over the Internet and sending them booby-trapped medical records for the “patient.” The other involves carefully editing email inboxes of public company executives to make it appear that some were involved in insider trading.

![]()

Alex Holden is founder of Hold Security, a Milwaukee-based cybersecurity firm. Holden’s team gained visibility into discussions among members of two different ransom groups: CLOP (a.k.a. “Cl0p” a.k.a. “TA505“), and a newer ransom group known as Venus.

Last month, the U.S. Department of Health and Human Services (HHS) warned that Venus ransomware attacks were targeting a number of U.S. healthcare organizations. First spotted in mid-August 2022, Venus is known for hacking into victims’ publicly-exposed Remote Desktop services to encrypt Windows devices.

Holden said the internal discussions among the Venus group members indicate this gang has no problem gaining access to victim organizations.

“The Venus group has problems getting paid,” Holden said. “They are targeting a lot of U.S. companies, but nobody wants to pay them.”

Which might explain why their latest scheme centers on trying to frame executives at public companies for insider trading charges. Venus indicated it recently had success with a method that involves carefully editing one or more email inbox files at a victim firm — to insert messages discussing plans to trade large volumes of the company’s stock based on non-public information.

“We imitate correspondence of the [CEO] with a certain insider who shares financial reports of his companies through which your victim allegedly trades in the stock market, which naturally is a criminal offense and — according to US federal laws [includes the possibility of up to] 20 years in prison,” one Venus member wrote to an underling.

“You need to create this file and inject into the machine(s) like this so that metadata would say that they were created on his computer,” they continued. “One of my clients did it, I don’t know how. In addition to pst, you need to decompose several files into different places, so that metadata says the files are native from a certain date and time rather than created yesterday on an unknown machine.”

Holden said it’s not easy to plant emails into an inbox, but it can be done with Microsoft Outlook .pst files, which the attackers may also have access to if they’d already compromised a victim network.

“It’s not going to be forensically solid, but that’s not what they care about,” he said. “It still has the potential to be a huge scandal — at least for a while — when a victim is being threatened with the publication or release of these records.”

The Venus ransom group’s extortion note. Image: Tripwire.com

Holden said the CLOP ransomware gang has a different problem of late: Not enough victims. The intercepted CLOP communication seen by KrebsOnSecurity shows the group bragged about twice having success infiltrating new victims in the healthcare industry by sending them infected files disguised as ultrasound images or other medical documents for a patient seeking a remote consultation.

The CLOP members said one tried-and-true method of infecting healthcare providers involved gathering healthcare insurance and payment data to use in submitting requests for a remote consultation on a patient who has cirrhosis of the liver.

“Basically, they’re counting on doctors or nurses reviewing the patient’s chart and scans just before the appointment,” Holden said. “They initially discussed going in with cardiovascular issues, but decided cirrhosis or fibrosis of the liver would be more likely to be diagnosable remotely from existing test results and scans.”

While CLOP as a money making collective is a fairly young organization, security experts say CLOP members hail from a group of Threat Actors (TA) known as “TA505,” which MITRE’s ATT&CK database says is a financially motivated cybercrime group that has been active since at least 2014. “This group is known for frequently changing malware and driving global trends in criminal malware distribution,” MITRE assessed.

In April, 2021, KrebsOnSecurity detailed how CLOP helped pioneer another innovation aimed at pushing more victims into paying an extortion demand: Emailing the ransomware victim’s customers and partners directly and warning that their data would be leaked to the dark web unless they can convince the victim firm to pay up.

Security firm Tripwire points out that the HHS advisory on Venus says multiple threat actor groups are likely distributing the Venus ransomware. Tripwire’s tips for all organizations on avoiding ransomware attacks include:

While the above tips are important and useful, one critical area of ransomware preparedness overlooked by too many organizations is the need to develop — and then periodically rehearse — a plan for how everyone in the organization should respond in the event of a ransomware or data ransom incident. Drilling this breach response plan is key because it helps expose weaknesses in those plans that could be exploited by the intruders.

As noted in last year’s story Don’t Wanna Pay Ransom Gangs? Test Your Backups, experts say the biggest reason ransomware targets and/or their insurance providers still pay when they already have reliable backups of their systems and data is that nobody at the victim organization bothered to test in advance how long this data restoration process might take.

“Suddenly the victim notices they have a couple of petabytes of data to restore over the Internet, and they realize that even with their fast connections it’s going to take three months to download all these backup files,” said Fabian Wosar, chief technology officer at Emsisoft. “A lot of IT teams never actually make even a back-of-the-napkin calculation of how long it would take them to restore from a data rate perspective.”

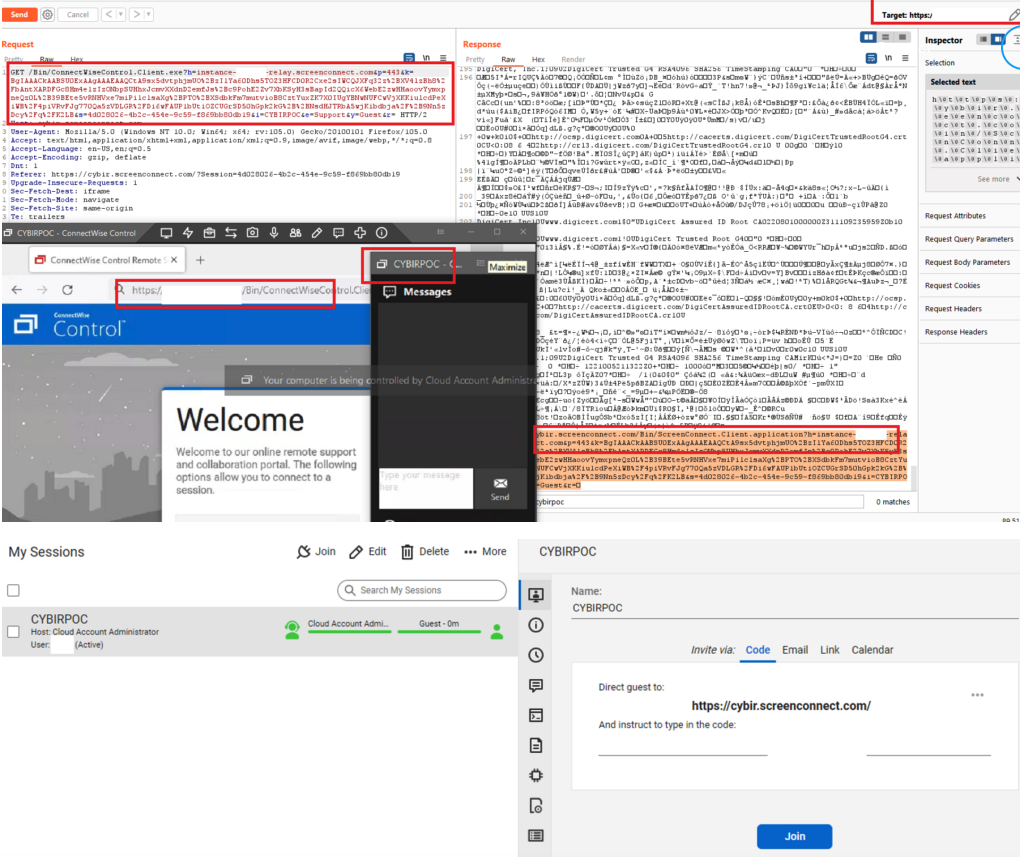

ConnectWise, which offers a self-hosted, remote desktop software application that is widely used by Managed Service Providers (MSPs), is warning about an unusually sophisticated phishing attack that can let attackers take remote control over user systems when recipients click the included link. The warning comes just weeks after the company quietly patched a vulnerability that makes it easier for phishers to launch these attacks.

A phishing attack targeting MSP customers using ConnectWise.

ConnectWise Control is extremely popular among MSPs that manage, protect and service large numbers of computers remotely for client organizations. Their product provides a dynamic software client and hosted server that connects two or more computers together, and provides temporary or persistent remote access to those client systems.

When a support technician wants to use it to remotely administer a computer, the ConnectWise website generates an executable file that is digitally signed by ConnectWise and downloadable by the client via a hyperlink.

When the remote user in need of assistance clicks the link, their computer is then directly connected to the computer of the remote administrator, who can then control the client’s computer as if they were seated in front of it.

While modern Microsoft Windows operating systems by default will ask users whether they want to run a downloaded executable file, many systems set up for remote administration by MSPs disable that user account control feature for this particular application.

In October, security researcher Ken Pyle alerted ConnectWise that their client executable file gets generated based on client-controlled parameters. Meaning, an attacker could craft a ConnectWise Control client download link that would bounce or proxy the remote connection from the MSP’s servers to a server that the attacker controls.

This is dangerous because many organizations that rely on MSPs to manage their computers often set up their networks so that only remote assistance connections coming from their MSP’s networks are allowed.

Using a free ConnectWise trial account, Pyle showed the company how easy it was to create a client executable that is cryptographically signed by ConnectWise and can bypass those network restrictions by bouncing the connection through an attacker’s ConnectWise Control server.

“You as the attacker have full control over the link’s parameters, and that link gets injected into an executable file that is downloaded by the client through an unauthenticated Web interface,” said Pyle, a partner and exploit developer at the security firm Cybir. “I can send this link to a victim, they will click this link, and their workstation will connect back to my instance via a link on your site.”

A composite of screenshots researcher Ken Pyle put together to illustrate the ScreenConnect vulnerability.

On Nov. 29, roughly the same time Pyle published a blog post about his findings, ConnectWise issued an advisory warning users to be on guard against a new round email phishing attempts that mimic legitimate email alerts the company sends when it detects unusual activity on a customer account.

“We are aware of a phishing campaign that mimics ConnectWise Control New Login Alert emails and has the potential to lead to unauthorized access to legitimate Control instances,” the company said.

ConnectWise said it released software updates last month that included new protections against the misdirection vulnerability that Pyle reported. But the company said there is no reason to believe the phishers they warned about are exploiting any of the issues reported by Pyle.

“Our team quickly triaged the report and determined the risk to partners to be minimal,” said Patrick Beggs, ConnectWise’s chief information security officer. “Nevertheless, the mitigation was simple and presented no risk to partner experience, so we put it into the then-stable 22.8 build and the then-canary 22.9 build, which were released as part of our normal release processes. Due to the low severity of the issue, we didn’t (and don’t plan to) issue a security advisory or alert, since we reserve those notifications for serious security issues.”

Beggs said the phishing attacks that sparked their advisory stemmed from an instance that was not hosted by ConnectWise.

“So we can confirm they are unrelated,” he said. “Unfortunately, phishing attacks happen far too regularly across a variety of industries and products. The timing of our advisory and Mr. Pyle’s blog were coincidental. That said, we’re all for raising more awareness of the seriousness of phishing attacks and the general importance of staying alert and aware of potentially dangerous content.”

The ConnectWise advisory warned users that before clicking any link that appears to come from their service, users should validate the content includes “domains owned by trusted sources,” and “links to go to places you recognize.”

But Pyle said this advice is not terribly useful for customers targeted in his attack scenario because the phishers can send emails directly from ConnectWise, and the short link that gets presented to the user is a wildcard domain that ends in ConnectWise Control’s own domain name — screenconnect.com. What’s more, examining the exceedingly long link generated by ConnectWise’s systems offers few insights to the average user.

“It’s signed by ConnectWise and comes from them, and if you sign up for a free trial instance, you can email people invites directly from them,” Pyle said.

ConnectWise’s warnings come amid breach reports from another major provider of remote support technologies: GoTo disclosed on Nov. 30 that it is investigating a security incident involving “unusual activity within our development environment and third-party cloud storage services. The third-party cloud storage service is currently shared by both GoTo and its affiliate, the password manager service LastPass.

In its own advisory on the incident, LastPass said they believe the intruders leveraged information stolen during a previous intrusion in August 2022 to gain access to “certain elements of our customers’ information.” However, LastPass maintains that its “customer passwords remain safely encrypted due to LastPass’s Zero Knowledge architecture.”

In short, that architecture means if you lose or forget your all-important master LastPass password — the one needed to unlock access to all of your other passwords stored with them — LastPass can’t help you with that, because they don’t store it. But that same architecture theoretically means that hackers who might break into LastPass’s networks can’t access that information either.

Update, 7:25 p.m. ET: Included statement from ConnectWise CISO.