A new breach involving data from nine million AT&T customers is a fresh reminder that your mobile provider likely collects and shares a great deal of information about where you go and what you do with your mobile device — unless and until you affirmatively opt out of this data collection. Here’s a primer on why you might want to do that, and how.

Image: Shutterstock

Telecommunications giant AT&T disclosed this month that a breach at a marketing vendor exposed certain account information for nine million customers. AT&T said the data exposed did not include sensitive information, such as credit card or Social Security numbers, or account passwords, but was limited to “Customer Proprietary Network Information” (CPNI), such as the number of lines on an account.

Certain questions may be coming to mind right now, like “What the heck is CPNI?” And, ‘If it’s so ‘customer proprietary,’ why is AT&T sharing it with marketers?” Also maybe, “What can I do about it?” Read on for answers to all three questions.

AT&T’s disclosure said the information exposed included customer first name, wireless account number, wireless phone number and email address. In addition, a small percentage of customer records also exposed the rate plan name, past due amounts, monthly payment amounts and minutes used.

CPNI refers to customer-specific “metadata” about the account and account usage, and may include:

-Called phone numbers

-Time of calls

-Length of calls

-Cost and billing of calls

-Service features

-Premium services, such as directory call assistance

According to a succinct CPNI explainer at TechTarget, CPNI is private and protected information that cannot be used for advertising or marketing directly.

“An individual’s CPNI can be shared with other telecommunications providers for network operating reasons,” wrote TechTarget’s Gavin Wright. “So, when the individual first signs up for phone service, this information is automatically shared by the phone provider to partner companies.”

Is your mobile Internet usage covered by CPNI laws? That’s less clear, as the CPNI rules were established before mobile phones and wireless Internet access were common. TechTarget’s CPNI primer explains:

“Under current U.S. law, cellphone use is only protected as CPNI when it is being used as a telephone. During this time, the company is acting as a telecommunications provider requiring CPNI rules. Internet use, websites visited, search history or apps used are not protected CPNI because the company is acting as an information services provider not subject to these laws.”

Hence, the carriers can share and sell this data because they’re not explicitly prohibited from doing so. All three major carriers say they take steps to anonymize the customer data they share, but researchers have shown it is not terribly difficult to de-anonymize supposedly anonymous web-browsing data.

“Your phone, and consequently your mobile provider, know a lot about you,” wrote Jack Morse for Mashable. “The places you go, apps you use, and the websites you visit potentially reveal all kinds of private information — e.g. religious beliefs, health conditions, travel plans, income level, and specific tastes in pornography. This should bother you.”

Happily, all of the U.S. carriers are required to offer customers ways to opt out of having data about how they use their devices shared with marketers. Here’s a look at some of the carrier-specific practices and opt-out options.

AT&T’s policy says it shares device or “ad ID”, combined with demographics including age range, gender, and ZIP code information with third parties which explicitly include advertisers, programmers, and networks, social media networks, analytics firms, ad networks and other similar companies that are involved in creating and delivering advertisements.

AT&T said the data exposed on 9 million customers was several years old, and mostly related to device upgrade eligibility. This may sound like the data went to just one of its partners who experienced a breach, but in all likelihood it also went to hundreds of AT&T’s partners.

AT&T’s CPNI opt-out page says it shares CPNI data with several of its affiliates, including WarnerMedia, DirecTV and Cricket Wireless. Until recently, AT&T also shared CPNI data with Xandr, whose privacy policy in turn explains that it shares data with hundreds of other advertising firms. Microsoft bought Xandr from AT&T last year.

According to the Electronic Privacy Information Center (EPIC), T-Mobile seems to be the only company out of the big three to extend to all customers the rights conferred by the California Consumer Privacy Act (CCPA).

EPIC says T-Mobile customer data sold to third parties uses another unique identifier called mobile advertising IDs or “MAIDs.” T-Mobile claims that MAIDs don’t directly identify consumers, but under the CCPA MAIDs are considered “personal information” that can be connected to IP addresses, mobile apps installed or used with the device, any video or content viewing information, and device activity and attributes.

T-Mobile customers can opt out by logging into their account and navigating to the profile page, then to “Privacy and Notifications.” From there, toggle off the options for “Use my data for analytics and reporting” and “Use my data to make ads more relevant to me.”

Verizon’s privacy policy says it does not sell information that personally identities customers (e.g., name, telephone number or email address), but it does allow third-party advertising companies to collect information about activity on Verizon websites and in Verizon apps, through MAIDs, pixels, web beacons and social network plugins.

According to Wired.com’s tutorial, Verizon users can opt out by logging into their Verizon account through a web browser or the My Verizon mobile app. From there, select the Account tab, then click Account Settings and Privacy Settings on the web. For the mobile app, click the gear icon in the upper right corner and then Manage Privacy Settings.

On the privacy preferences page, web users can choose “Don’t use” under the Custom Experience section. On the My Verizon app, toggle any green sliders to the left.

EPIC notes that all three major carriers say resetting the consumer’s device ID and/or clearing cookies in the browser will similarly reset any opt-out preferences (i.e., the customer will need to opt out again), and that blocking cookies by default may also block the opt-out cookie from being set.

T-Mobile says its opt out is device-specific and/or browser-specific. “In most cases, your opt-out choice will apply only to the specific device or browser on which it was made. You may need to separately opt out from your other devices and browsers.”

Both AT&T and Verizon offer opt-in programs that gather and share far more information, including device location, the phone numbers you call, and which sites you visit using your mobile and/or home Internet connection. AT&T calls this their Enhanced Relevant Advertising Program; Verizon’s is called Custom Experience Plus.

In 2021, multiple media outlets reported that some Verizon customers were being automatically enrolled in Custom Experience Plus — even after those customers had already opted out of the same program under its previous name — “Verizon Selects.”

If none of the above opt out options work for you, at a minimum you should be able to opt out of CPNI sharing by calling your carrier, or by visiting one of their stores.

Why should you opt out of sharing CPNI data? For starters, some of the nation’s largest wireless carriers don’t have a great track record in terms of protecting the sensitive information that you give them solely for the purposes of becoming a customer — let alone the information they collect about your use of their services after that point.

In January 2023, T-Mobile disclosed that someone stole data on 37 million customer accounts, including customer name, billing address, email, phone number, date of birth, T-Mobile account number and plan details. In August 2021, T-Mobile acknowledged that hackers made off with the names, dates of birth, Social Security numbers and driver’s license/ID information on more than 40 million current, former or prospective customers who applied for credit with the company.

Last summer, a cybercriminal began selling the names, email addresses, phone numbers, SSNs and dates of birth on 23 million Americans. An exhaustive analysis of the data strongly suggested it all belonged to customers of one AT&T company or another. AT&T stopped short of saying the data wasn’t theirs, but said the records did not appear to have come from its systems and may be tied to a previous data incident at another company.

However frequently the carriers may alert consumers about CPNI breaches, it’s probably nowhere near often enough. Currently, the carriers are required to report a consumer CPNI breach only in cases “when a person, without authorization or exceeding authorization, has intentionally gained access to, used or disclosed CPNI.”

But that definition of breach was crafted eons ago, back when the primary way CPNI was exposed was through “pretexting,” such when the phone company’s employees are tricked into giving away protected customer data.

In January, regulators at the U.S. Federal Communications Commission (FCC) proposed amending the definition of “breach” to include things like inadvertent disclosure — such as when companies expose CPNI data on a poorly-secured server in the cloud. The FCC is accepting public comments on the matter until March 24, 2023.

While it’s true that the leak of CPNI data does not involve sensitive information like Social Security or credit card numbers, one thing AT&T’s breach notice doesn’t mention is that CPNI data — such as balances and payments made — can be abused by fraudsters to make scam emails and text messages more believable when they’re trying to impersonate AT&T and phish AT&T customers.

The other problem with letting companies share or sell your CPNI data is that the wireless carriers can change their privacy policies at any time, and you are assumed to be okay with those changes as long as you keep using their services.

For example, location data from your wireless device is most definitely CPNI, and yet until very recently all of the major carriers sold their customers’ real-time location data to third party data brokers without customer consent.

What was their punishment? In 2020, the FCC proposed fines totaling $208 million against all of the major carriers for selling their customers’ real-time location data. If that sounds like a lot of money, consider that all of the major wireless providers reported tens of billions of dollars in revenue last year (e.g., Verizon’s consumer revenue alone was more than $100 billion last year).

If the United States had federal privacy laws that were at all consumer-friendly and relevant to today’s digital economy, this kind of data collection and sharing would always be opt-in by default. In such a world, the enormously profitable wireless industry would likely be forced to offer clear financial incentives to customers who choose to share this information.

But until that day arrives, understand that the carriers can change their data collection and sharing policies when it suits them. And regardless of whether you actually read any notices about changes to their privacy policies, you will have agreed to those changes as long as you continue using their service.

Millions of Americans receiving food assistance benefits just earned a new right that they can’t yet enforce: The right to be reimbursed if funds on their Electronic Benefit Transfer (EBT) cards are stolen by card skimming devices secretly installed at cash machines and grocery store checkout lanes.

![]()

On December 29, 2022, President Biden signed into law the Consolidated Appropriations Act of 2023, which — for the first time ever — includes provisions for the replacement of stolen EBT benefits. This is a big deal because in 2022, organized crime groups began massively targeting EBT accounts — often emptying affected accounts at ATMs immediately after the states disperse funds each month.

EBT cards can be used along with a personal identification number (PIN) to pay for goods at participating stores, and to withdraw cash from an ATM. However, EBT cards differ from debit cards issued to most Americans in two important ways. First, most states do not equip EBT cards with smart chip technology, which can make the cards more difficult and expensive for skimming thieves to clone.

More critically, EBT participants traditionally have had little hope of recovering food assistance funds when their cards were copied by card-skimming devices and used for fraud. That’s because while the EBT programs are operated by individually by the states, those programs are funded by the U.S. Department of Agriculture (USDA), which until late last year was barred from reimbursing states for stolen EBT funds.

The protections passed in the 2023 Appropriations Act allow states to use federal funds to replace stolen EBT benefits, and they permit states to seek reimbursement for any skimmed EBT funds they may have replaced from their own coffers (dating back to Oct. 1, 2022).

But first, all 50 states must each submit a plan for how they are going to protect and replace food benefits stolen via card skimming. Guidance for the states in drafting those plans was issued by the USDA on Jan. 31 (PDF), and states that don’t get them done before Feb. 27, 2023 risk losing the ability to be reimbursed for EBT fraud losses.

Deborah Harris is a staff attorney at The Massachusetts Law Reform Institute (MLRI), a nonprofit legal assistance organization that has closely tracked the EBT skimming epidemic. In November 2022, the MLRI filed a class-action lawsuit against Massachusetts on behalf of thousands of low-income families who were collectively robbed of more than $1 million in food assistance benefits by card skimming devices secretly installed at cash machines and grocery store checkout lanes across the state.

Harris said she’s pleased that the USDA guidelines were issued so promptly, and that the guidance for states was not overly prescriptive. For example, some security experts have suggested that adding contactless capability to EBT cards could help participants avoid skimming devices altogether. But Harris said contactless cards do not require a PIN, which is the only thing that stops EBT cards from being drained at the ATM when a participant’s card is lost or stolen.

Then again, nothing in the guidance even mentions chip-based cards, or any other advice for improving the physical security of EBT cards. Rather, it suggests states should seek to develop the capability to perform basic fraud detection and alerting on suspicious transactions, such as when an EBT card that is normally used only in one geographic area suddenly is used to withdraw cash at an ATM halfway across the country.

“Besides having the states move fast to approve their plans, we’d also like to see a focused effort to move states from magstripe-only cards to chip, and also assisting states to develop the algorithms that will enable them to identify likely incidents of stolen benefits,” Harris said.

Harris said Massachusetts has begun using algorithms to look for these suspicious transaction patterns throughout its EBT network, and now has the ability to alert households and verify transactions. But she said most states do not have this capability.

“We have heard that other states aren’t currently able to do that,” Harris said. “But encouraging states to more affirmatively identify instances of likely theft and assisting with the claims and verification process is critical. Most households can’t do that on their own, and in Massachusetts it’s very hard for a person to get a copy of their transaction history. Some states can do that through third-party apps, but something so basic should not be on the burden of EBT households.”

Some states aren’t waiting for direction from the federal government to beef up EBT card security. Like Maryland, which identified more than 1,400 households hit by EBT skimming attacks last year — a tenfold increase over 2021.

Advocates for EBT beneficiaries in Maryland are backing Senate Bill 401 (PDF), which would require the use of chip technology and ongoing monitoring for suspicious activity (a hearing on SB401 is scheduled in the Maryland Senate Finance Commission for Thursday, Feb. 23, at 1 p.m.).

Michelle Salomon Madaio is a director at the Homeless Persons Representation Project, a legal assistance organization based in Silver Spring, Md. Madaio said the bill would require the state Department of Human Services to replace skimmed benefits, not only after the bill goes into effect but also retroactively from January 2020 to the present.

Madaio said the bill also would require the state to monitor for patterns of suspicious activity on EBT cards, and to develop a mechanism to contact potentially affected households.

“For most of the skimming victims we’ve worked with, the fraudulent transactions would be pretty easy to spot because they mostly happened in the middle of the night or out of state, or both,” Madaio said. “To make matters worse, a lot of families whose benefits were scammed then incurred late fees on many other things as a result.”

It is not difficult to see why organized crime groups have pounced on EBT cards as easy money. In most traditional payment card transactions, there are usually several parties that have a financial interest in minimizing fraud and fraud losses, including the bank that issued the card, the card network (Visa, MasterCard, Discover, etc.), and the merchant.

But that infrastructure simply does not exist within state EBT programs, and it certainly isn’t a thing at the inter-state level. What that means is that the vast majority of EBT cards have zero fraud controls, which is exactly what continues to make them so appealing to thieves.

For now, the only fraud controls available to most EBT cardholders include being especially paranoid about where they use their cards, and frequently changing their PINs.

According to USDA guidance issued prior to the passage of the appropriations act, EBT cardholders should consider changing their card PIN at least once a month.

“By changing PINs frequently, at least monthly, and doing so before benefit issuance dates, households can minimize their risk of stolen benefits from a previously skimmed EBT card,” the USDA advised.

Authorities in the United States and United Kingdom today levied financial sanctions against seven men accused of operating “Trickbot,” a cybercrime-as-a-service platform based in Russia that has enabled countless ransomware attacks and bank account takeovers since its debut in 2016. The U.S. Department of the Treasury says the Trickbot group is associated with Russian intelligence services, and that this alliance led to the targeting of many U.S. companies and government entities.

Initially a stealthy trojan horse program delivered via email and used to steal passwords, Trickbot evolved into “a highly modular malware suite that provides the Trickbot Group with the ability to conduct a variety of illegal cyber activities, including ransomware attacks,” the Treasury Department said.

A spam email from 2020 containing a Trickbot-infected attachment. Image: Microsoft.

“During the height of the COVID-19 pandemic in 2020, Trickbot targeted hospitals and healthcare centers, launching a wave of ransomware attacks against hospitals across the United States,” the sanctions notice continued. “In one of these attacks, the Trickbot Group deployed ransomware against three Minnesota medical facilities, disrupting their computer networks and telephones, and causing a diversion of ambulances. Members of the Trickbot Group publicly gloated over the ease of targeting the medical facilities and the speed with which the ransoms were paid to the group.”

Only one of the men sanctioned today is known to have been criminally charged in connection with hacking activity. According to the Treasury Department, the alleged senior leader of the Trickbot group is 34-year-old Russian national Vitaly “Bentley” Kovalev.

A New Jersey grand jury indicted Kovalev in 2012 after an investigation by the U.S. Secret Service determined that he ran a massive “money mule” scheme, which used phony job offers to trick people into laundering money stolen from hacked small to mid-sized businesses in the United States. The 2012 indictment against Kovalev relates to cybercrimes he allegedly perpetrated prior to the creation of Trickbot.

In 2015, Kovalev reportedly began filming a movie in Russia about cybercrime called “Botnet.” According to a 2016 story from Forbes.ru, Botnet’s opening scene was to depict the plight of Christina Svechinskaya, a Russian student arrested by FBI agents in September 2010.

Christina Svechinskaya, a money mule hired by Bentley who was arrested by the FBI in 2010.

Svechinskaya was one of Bentley’s money mules, most of whom were young Russian students on temporary travel visas in the United States. She was among 37 alleged mules charged with aiding an international cybercrime operation — basically, setting up phony corporate bank accounts for the sole purpose of laundering stolen funds.

Although she possessed no real hacking skills, Svechinskaya’s mugshot and social media photos went viral online and she was quickly dubbed “the world’s sexiest computer hacker” by the tabloids.

Kovalev’s Botnet film project was disrupted after Russian authorities raided the film production company’s offices as part of a cybercrime investigation. In February 2016, Reuters reported that the raid was connected to a crackdown on “Dyre,” a sophisticated trojan that U.S. federal investigators say was the precursor to the Trickbot malware. The Forbes.ru article cited sources close to the investigation who said the film studio was operating as a money-laundering front for the cybercrooks behind Dyre.

But shifting political winds in Russia would soon bring high treason charges against three of the Russian cybercrime investigators tied to the investigation into the film studio. In a major shakeup in 2017, the Kremlin levied treason charges against Sergey Mikhaylov, then deputy chief of Russia’s top anti-cybercrime unit.

Also charged with treason was Ruslan Stoyanov, then a senior employee at Russian security firm Kaspersky Lab [the Forbes.ru report from 2016 said investigators from Mikhaylov’s unit and Kaspersky Lab were present at the film company raid].

Russian media outlets have speculated that the men were accused of treason for helping American cybercrime investigators pursue top Russian hackers. However, the charges against both men were classified and have never been officially revealed. After their brief, closed trial, both men were convicted of treason. Mikhaylov was given a 22 year prison sentence; Stoyanov was sentenced to 14 years in prison.

In September 2021, the Kremlin issued treason charges against Ilya Sachkov, formerly head of the cybersecurity firm Group-IB. According to Reuters, Sachkov and his company were hired by the film studio “to advise the Botnet director and writers on the finer points of cybercrime.” Sachkov remains imprisoned in Russia pending his treason trial.

Trickbot was heavily used by Conti and Ryuk, two of Russia’s most ruthless and successful ransomware groups. Blockchain analysis firm Chainalysis estimates that in 2021 alone, Conti extorted more than USD $100 million from its hacking victims; Chainalysis estimates Ryuk extorted more than USD $150 million from its ransomware victims.

The U.S. cybersecurity firm CrowdStrike has long tracked the activities of Trickbot, Ryuk and Conti under the same moniker — “Wizard Spider” — which CrowdStrike describes as “a Russia-nexus cybercriminal group behind the core development and distribution of a sophisticated arsenal of criminal tools, that allow them to run multiple different types of operations.”

“CrowdStrike Intelligence has observed WIZARD SPIDER targeting multiple countries and industries such as academia, energy, financial services, government, and more,” said Adam Meyers, head of intelligence at CrowdStrike.

This is not the U.S. government’s first swipe at the Trickbot group. In early October 2020, KrebsOnSecurity broke the news that someone had launched a series of coordinated attacks designed to disrupt the Trickbot botnet. A week later, The Washington Post ran a story saying the attack on Trickbot was the work of U.S. Cyber Command, a branch of the Department of Defense headed by the director of the U.S. National Security Agency (NSA).

Days after Russia invaded Ukraine in February 2022, a Ukrainian researcher leaked several years of internal chat logs from the Conti ransomware gang. Those candid conversations offer a fascinating view into the challenges of running a sprawling criminal enterprise with more than 100 salaried employees. They also showed that Conti enjoyed protection from prosecution by Russian authorities, as long as the hacker group took care not to target Russian organizations.

In addition, the leaked Conti chats confirmed there was considerable overlap in the operation and leadership of Conti, Trickbot and Ryuk.

Michael DeBolt, chief intelligence officer at cybersecurity firm Intel 471, said the leaked Conti chats showed Bentley oversaw a team of coders tasked with ensuring that the Trickbot and Conti malware remained undetected by the different antivirus and security software vendors.

In the years prior to the emergence of Trickbot in 2016, Bentley worked closely on the Gameover ZeuS trojan, a peer-to-peer malware threat that infected between 500,000 and a million computers with an automated ransomware strain called Cryptolocker, DeBolt said.

The FBI has a standing $3 million bounty offered for the capture of Evgeny “Slavik” Bogachev, the alleged author of the Zeus trojan. And there are indications that Bentley worked directly with Bogachev. DeBolt pointed to an October 2014 discussion on the exclusive Russian hacking forum Mazafaka that included a complaint by a Russian hosting firm against a forum user by the name “Ferrari” who had failed to pay a $30,000 hosting bill.

In that discussion thread, it emerged that the hosting company thought it was filing a complaint against Slavik. But the Mazafaka member who vouched for Ferrari’s membership on the forum said they knew Ferrari as Bentley the mule handler, and at some point Slavik and Bentley must have been sharing the Ferrari user account.

“It is likely that Slavik (aka. Bogachev) and Bentley (aka. Kovalev) shared the same ‘Ferrari’ handle on the Mazafaka forum circa 2014, which suggests the two had a working relationship at that time, and supports the recent US and UK Government announcements regarding Kovalev’s past involvement in cybercrime predating Dyre or the Trickbot Group,” DeBolt said.

CrowdStrike’s Meyers said while Wizard Spider operations have significantly reduced following the demise of Conti in June 2022, today’s sanctions will likely cause temporary disruptions for the cybercriminal group while they look for ways to circumvent the financial restrictions — which make it illegal to transact with or hold the assets of sanctioned persons or entities.

“Often, when cybercriminal groups are disrupted, they will go dark for a time only to rebrand under a new name,” Meyers said.

The prosecution of Kovalev is being handled by the U.S. Attorney’s Office in New Jersey. A copy of the now-unsealed 2012 indictment of Kovalev is here (PDF).

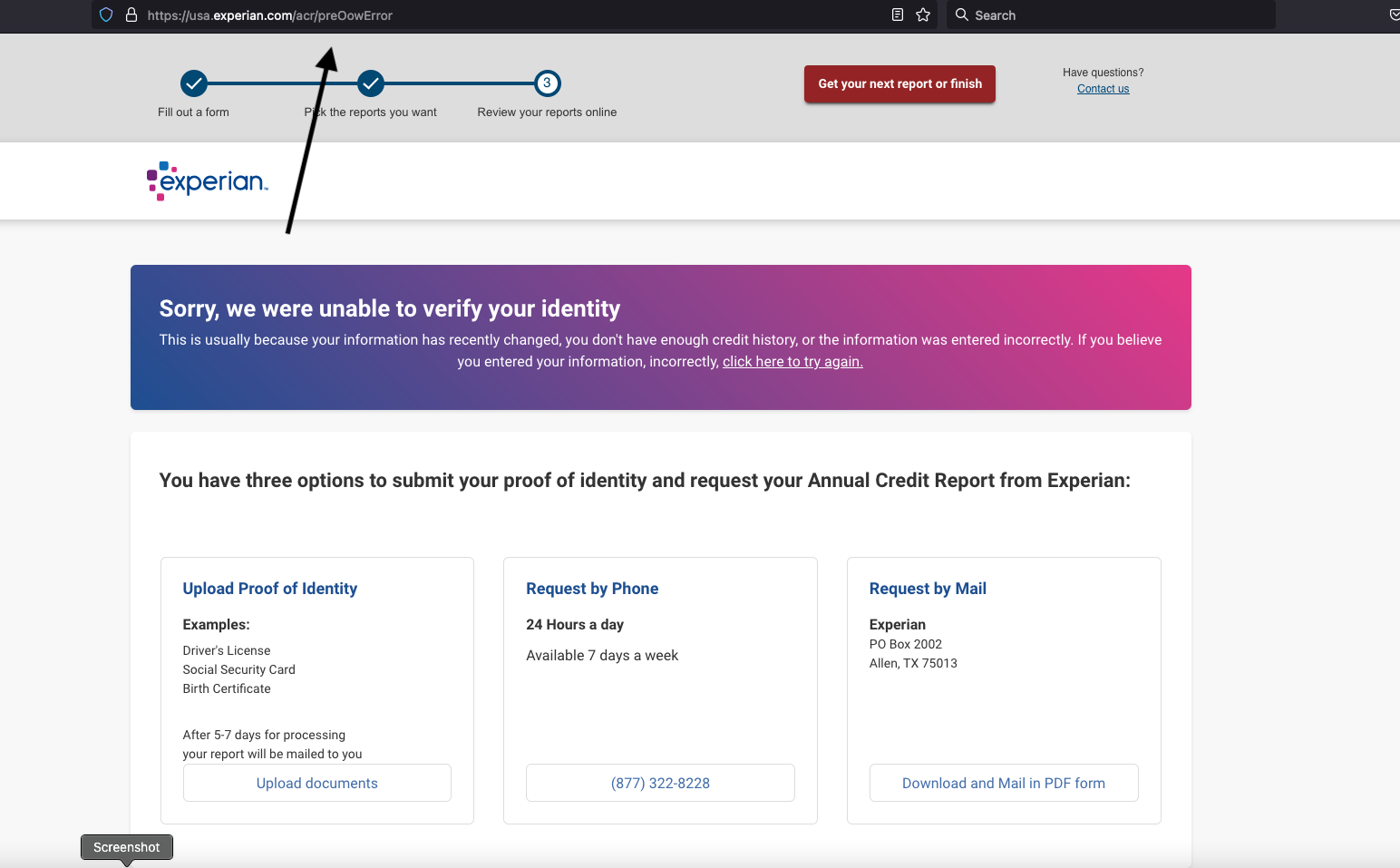

On Dec. 23, 2022, KrebsOnSecurity alerted big-three consumer credit reporting bureau Experian that identity thieves had worked out how to bypass its security and access any consumer’s full credit report — armed with nothing more than a person’s name, address, date of birth, and Social Security number. Experian fixed the glitch, but remained silent about the incident for a month. This week, however, Experian acknowledged that the security failure persisted for nearly seven weeks, between Nov. 9, 2022 and Dec. 26, 2022.

![]()

The tip about the Experian weakness came from Jenya Kushnir, a security researcher living in Ukraine who said he discovered the method being used by identity thieves after spending time on Telegram chat channels dedicated to cybercrime.

Normally, Experian’s website will ask a series of multiple-choice questions about one’s financial history, as a way of validating the identity of the person requesting the credit report. But Kushnir said the crooks learned they could bypass those questions and trick Experian into giving them access to anyone’s credit report, just by editing the address displayed in the browser URL bar at a specific point in Experian’s identity verification process.

When I tested Kushnir’s instructions on my own identity at Experian, I found I was able to see my report even though Experian’s website told me it didn’t have enough information to validate my identity. A security researcher friend who tested it at Experian found she also could bypass Experian’s four or five multiple-choice security questions and go straight to her full credit report at Experian.

Experian acknowledged receipt of my Dec. 23 report four days later on Dec. 27, a day after Kushnir’s method stopped working on Experian’s website (the exploit worked as long as you came to Experian’s website via annualcreditreport.com — the site mandated to provide a free copy of your credit report from each of the major bureaus once a year).

Experian never did respond to official requests for comment on that story. But earlier this week, I received an otherwise unhelpful letter via snail mail from Experian (see image above), which stated that the weakness we reported persisted between Nov. 9, 2022 and Dec. 26, 2022.

“During this time period, we experienced an isolated technical issue where a security feature may not have functioned,” Experian explained.

It’s not entirely clear whether Experian sent me this paper notice because they legally had to, or if they felt I deserved a response in writing and thought maybe they’d kill two birds with one stone. But it’s pretty crazy that it took them a full month to notify me about the potential impact of a security failure that I notified them about.

It’s also a little nuts that Experian didn’t simply include a copy of my current credit report along with this letter, which is confusingly worded and reads like they suspect someone other than me may have been granted access to my credit report without any kind of screening or authorization.

After all, if I hadn’t authorized the request for my credit file that apparently prompted this letter (I had), that would mean the thieves already had my report. Shouldn’t I be granted the same visibility into my own credit file as them?

Instead, their woefully inadequate letter once again puts the onus on me to wait endlessly on hold for an Experian representative over the phone, or sign up for a free year’s worth of Experian monitoring my credit report.

As it stands, using Kushnir’s exploit was the only time I’ve ever been able to get Experian’s website to cough up a copy of my credit report. To make matters worse, a majority of the information in that credit report is not mine. So I’ve got that to look forward to.

If there is a silver lining here, I suppose that if I were Experian, I probably wouldn’t want to show Brian Krebs his credit file either. Because it’s clear this company has no idea who I really am. And in a weird, kind of sad way I guess, that makes me happy.

For thoughts on what you can do to minimize your victimization by and overall worth to the credit bureaus, see this section of the most recent Experian story.

Identity thieves have been exploiting a glaring security weakness in the website of Experian, one of the big three consumer credit reporting bureaus. Normally, Experian requires that those seeking a copy of their credit report successfully answer several multiple choice questions about their financial history. But until the end of 2022, Experian’s website allowed anyone to bypass these questions and go straight to the consumer’s report. All that was needed was the person’s name, address, birthday and Social Security number.

The vulnerability in Experian’s website was exploitable after one applied to see their credit file via annualcreditreport.com.

In December, KrebsOnSecurity heard from Jenya Kushnir, a security researcher living in Ukraine who said he discovered the method being used by identity thieves after spending time on Telegram chat channels dedicated to the cashing out of compromised identities.

“I want to try and help to put a stop to it and make it more difficult for [ID thieves] to access, since [Experian is] not doing shit and regular people struggle,” Kushnir wrote in an email to KrebsOnSecurity explaining his motivations for reaching out. “If somehow I can make small change and help to improve this, inside myself I can feel that I did something that actually matters and helped others.”

Kushnir said the crooks learned they could trick Experian into giving them access to anyone’s credit report, just by editing the address displayed in the browser URL bar at a specific point in Experian’s identity verification process.

Following Kushnir’s instructions, I sought a copy of my credit report from Experian via annualcreditreport.com — a website that is required to provide all Americans with a free copy of their credit report from each of the three major reporting bureaus, once per year.

Annualcreditreport.com begins by asking for your name, address, SSN and birthday. After I supplied that and told Annualcreditreport.com I wanted my report from Experian, I was taken to Experian.com to complete the identity verification process.

![]()

Normally at this point, Experian’s website would present four or five multiple-guess questions, such as “Which of the following addresses have you lived at?”

Kushnir told me that when the questions page loads, you simply change the last part of the URL from “/acr/oow/” to “/acr/report,” and the site would display the consumer’s full credit report.

But when I tried to get my report from Experian via annualcreditreport.com, Experian’s website said it didn’t have enough information to validate my identity. It wouldn’t even show me the four multiple-guess questions. Experian said I had three options for a free credit report at this point: Mail a request along with identity documents, call a phone number for Experian, or upload proof of identity via the website.

But that didn’t stop Experian from showing me my full credit report after I changed the Experian URL as Kushnir had instructed — modifying the error page’s trailing URL from “/acr/OcwError” to simply “/acr/report”.

Experian’s website then immediately displayed my entire credit file.

Even though Experian said it couldn’t tell that I was actually me, it still coughed up my report. And thank goodness it did. The report contains so many errors that it’s probably going to take a good deal of effort on my part to straighten out.

Now I know why Experian has NEVER let me view my own file via their website. For example, there were four phone numbers on my Experian credit file: Only one of them was mine, and that one hasn’t been mine for ages.

I was so dumbfounded by Experian’s incompetence that I asked a close friend and trusted security source to try the method on her identity file at Experian. Sure enough, when she got to the part where Experian asked questions, changing the last part of the URL in her address bar to “/report” bypassed the questions and immediately displayed her full credit report. Her report also was replete with errors.

KrebsOnSecurity shared Kushnir’s findings with Experian on Dec. 23, 2022. On Dec. 27, 2022, Experian’s PR team acknowledged receipt of my Dec. 23 notification, but the company has so far ignored multiple requests for comment or clarification.

By the time Experian confirmed receipt of my report, the “exploit” Kushnir said he learned from the identity thieves on Telegram had been patched and no longer worked. But it remains unclear how long Experian’s website was making it so easy to access anyone’s credit report.

In response to information shared by KrebsOnSecurity, Senator Ron Wyden (D-Ore.) said he was disappointed — but not at all surprised — to hear about yet another cybersecurity lapse at Experian.

“The credit bureaus are poorly regulated, act as if they are above the law and have thumbed their noses at Congressional oversight,” Wyden said in a written statement. “Just last year, Experian ignored repeated briefing requests from my office after you revealed another cybersecurity lapse the company.”

Sen. Wyden’s quote above references a story published here in July 2022, which broke the news that identity thieves were hijacking consumer accounts at Experian.com just by signing up as them at Experian once more, supplying the target’s static, personal information (name, DoB/SSN, address) but a different email address.

From interviews with multiple victims who contacted KrebsOnSecurity after that story, it emerged that Experian’s own customer support representatives were actually telling consumers who got locked out of their Experian accounts to recreate their accounts using their personal information and a new email address. This was Experian’s advice even for people who’d just explained that this method was what identity thieves had used to lock them in out in the first place.

Clearly, Experian found it simpler to respond this way, rather than acknowledging the problem and addressing the root causes (lazy authentication and abhorrent account recovery practices). It’s also worth mentioning that reports of hijacked Experian.com accounts persisted into late 2022. That screw-up has since prompted a class action lawsuit against Experian.

Sen. Wyden said the Federal Trade Commission (FTC) and Consumer Financial Protection Bureau (CFPB) need to do much more to protect Americans from screw-ups by the credit bureaus.

“If they don’t believe they have the authority to do so, they should endorse legislation like my Mind Your Own Business Act, which gives the FTC power to set tough mandatory cybersecurity standards for companies like Experian,” Wyden said.

Sadly, none of this is terribly shocking behavior for Experian, which has shown itself a completely negligent custodian of obscene amounts of highly sensitive consumer information.

In April 2021, KrebsOnSecurity revealed how identity thieves were exploiting lax authentication on Experian’s PIN retrieval page to unfreeze consumer credit files. In those cases, Experian failed to send any notice via email when a freeze PIN was retrieved, nor did it require the PIN to be sent to an email address already associated with the consumer’s account.

A few days after that April 2021 story, KrebsOnSecurity broke the news that an Experian API was exposing the credit scores of most Americans.

It’s bad enough that we can’t really opt out of companies like Experian making $2.6 billion each quarter collecting and selling gobs of our personal and financial information. But there has to be some meaningful accountability when these monopolistic companies engage in negligent and reckless behavior with the very same consumer data that feeds their quarterly profits. Or when security and privacy shortcuts are found to be intentional, like for cost-saving reasons.

And as we saw with Equifax’s consolidated class-action settlement in response to letting state-sponsored hackers from China steal data on nearly 150 million Americans back in 2017, class-actions and more laughable “free credit monitoring” services from the very same companies that created the problem aren’t going to cut it.

It is easy to adopt a defeatist attitude with the credit bureaus, who often foul things up royally even for consumers who are quite diligent about watching their consumer credit files and disputing any inaccuracies.

But there are some concrete steps that everyone can take which will dramatically lower the risk that identity thieves will ruin your financial future. And happily, most of these steps have the side benefit of costing the credit bureaus money, or at least causing the data they collect about you to become less valuable over time.

The first step is awareness. Find out what these companies are saying about you behind your back. Keep in mind that — fair or not — your credit score as collectively determined by these bureaus can affect whether you get that loan, apartment, or job. In that context, even small, unintentional errors that are unrelated to identity theft can have outsized consequences for consumers down the road.

Each bureau is required to provide a free copy of your credit report every year. The easiest way to get yours is through annualcreditreport.com.

Some consumers report that this site never works for them, and that each bureau will insist they don’t have enough information to provide a report. I am definitely in this camp. Thankfully, a financial institution that I already have a relationship with offers the ability to view your credit file through them. Your mileage on this front may vary, and you may end up having to send copies of your identity documents through the mail or website.

When you get your report, look for anything that isn’t yours, and then document and file a dispute with the corresponding credit bureau. And after you’ve reviewed your report, set a calendar reminder to recur every four months, reminding you it’s time to get another free copy of your credit file.

If you haven’t already done so, consider making 2023 the year that you freeze your credit files at the three major reporting bureaus, including Experian, Equifax and TransUnion. It is now free to people in all 50 U.S. states to place a security freeze on their credit files. It is also free to do this for your partner and/or your dependents.

Freezing your credit means no one who doesn’t already have a financial relationship with you can view your credit file, making it unlikely that potential creditors will grant new lines of credit in your name to identity thieves. Freezing your credit file also means Experian and its brethren can no longer sell peeks at your credit history to others.

Anytime you wish to apply for new credit or a new job, or open an account at a utility or communications provider, you can quickly thaw a freeze on your credit file, and set it to freeze automatically again after a specified length of time.

Please don’t confuse a credit freeze (a.k.a. “security freeze”) with the alternative that the bureaus will likely steer you towards when you ask for a freeze: “Credit lock” services.

The bureaus pitch these credit lock services as a way for consumers to easily toggle their credit file availability with push of a button on a mobile app, but they do little to prevent the bureaus from continuing to sell your information to others.

My advice: Ignore the lock services, and just freeze your credit files already.

One final note. Frequent readers here will have noticed that I’ve criticized these so-called “knowledge-based authentication” or KBA questions that Experian’s website failed to ask as part of its consumer verification process.

KrebsOnSecurity has long assailed KBA as weak authentication because the questions and answers are drawn largely from consumer records that are public and easily accessible to organized identity theft groups.

That said, given that these KBA questions appear to be the ONLY thing standing between me and my Experian credit report, it seems like maybe they should at least take care to ensure that those questions actually get asked.

Photo: BrandonKleinPhoto / Shutterstock.com

Two U.S. men have been charged with hacking into the Ring home security cameras of a dozen random people and then “swatting” them — falsely reporting a violent incident at the target’s address to trick local police into responding with force. Prosecutors say the duo used the compromised Ring devices to stream live video footage on social media of police raiding their targets’ homes, and to taunt authorities when they arrived.

Prosecutors in Los Angeles allege 20-year-old James Thomas Andrew McCarty, a.k.a. “Aspertaine,” of Charlotte, N.C., and Kya Christian Nelson, a.k.a. “ChumLul,” 22, of Racine, Wisc., conspired to hack into Yahoo email accounts belonging to victims in the United States. From there, the two allegedly would check how many of those Yahoo accounts were associated with Ring accounts, and then target people who used the same password for both accounts.

An indictment unsealed this week says that in the span of just one week in November 2020, McCarty and Nelson identified and swatted at least a dozen different victims across the country.

“The defendants then allegedly accessed without authorization the victims’ Ring devices and transmitted the audio and video from those devices on social media during the police response,” reads a statement from Martin Estrada, the U.S. Attorney for the Central District of California. “They also allegedly verbally taunted responding police officers and victims through the Ring devices during several of the incidents.”

James Thomas Andrew McCarty.

The indictment charges that McCarty continued his swatting spree in 2021 from his hometown in Kayenta, Ariz., where he called in bomb threats or phony hostage situations on more than two dozen occasions.

The Telegram and Discord aliases allegedly used by McCarty — “Aspertaine” and “Couch,” among others — correspond to an identity that was active in certain channels dedicated to SIM-swapping, a crime that involves stealing wireless phone numbers and hijacking the online financial and social media accounts tied to those numbers.

Aspertaine bragged on Discord that he’d amassed more than $330,000 in virtual currency. On Telegram, the Aspertaine/Couch alias frequented several popular SIM-swapping channels, where they initially were active as a “holder” — a SIM-swapping group member who agrees to hold SIM cards used in the heist after an account takeover is completed. Aspertaine later claimed more direct involvement in individual SIM-swapping attacks.

In September, KrebsOnSecurity broke the news about a wide-ranging federal investigation into “violence-as-a-service” offerings on Telegram and other social media networks, wherein people can settle scores by hiring total strangers to carry out physical attacks such as brickings, shootings, and firebombings at a target’s address.

The story observed that SIM swappers were especially enamored of these “IRL” or “In Real Life” violence services, which they frequently used to target one another in response to disagreements over how stolen money should be divided amongst themselves. And a number of Aspertaine’s peers on these SIM-swapping channels claimed they’d been ripped off after Aspertaine took more than a fair share from them.

In August, a member of a popular SIM-swapping group on Telegram who was slighted by Aspertaine put out the word that he was looking for some physical violence to be visited on McCarty’s address in North Carolina. “Anyone live near here and wants to [do] a job for me,” the job ad with McCarty’s home address read. “Jobs range from $1k-$50k. Payment in BTC [bitcoin].” It’s unclear if anyone responded to that job offer.

![]()

Ring, Inc., which is owned by Amazon, said it learned bad actors used stolen customer email credentials obtained from external (non-Ring) services to access other accounts, and took immediate steps to help those customers secure their Ring accounts.

“We also supported the FBI in identifying the individuals responsible,” the company said in a written statement. “We take the security of our customers extremely seriously — that’s why we made two-step verification mandatory, conduct regular scans for Ring passwords compromised in non-Ring breaches, and continually invest in new security protections to harden our systems. We are committed to continuing to protect our customers and vigorously going after those who seek to harm them.”

KrebsOnSecurity recently published The Wages of Password ReUse: Your Money or Your Life, which noted that when normal computer users fall into the nasty habit of recycling passwords, the result is most often some type of financial loss. Whereas, when cybercriminals reuse passwords, it often costs them their freedom.

But perhaps that story should be updated, because it’s now clear that password reuse can also put you in mortal danger. Swatting attacks are dangerous, expensive hoaxes that sometimes end in tragedy.

In June 2021, an 18-year-old serial swatter from Tennessee was sentenced to five years in prison for his role in a fraudulent swatting attack that led to the death of a 60-year-old man.

In 2019, prosecutors handed down a 20-year sentence to Tyler Barriss, a then 26-year-old serial swatter from California who admitted making a phony emergency call to police in late 2017 that led to the shooting death of an innocent Kansas man.

McCarty was arrested last week, and charged with conspiracy to intentionally access computers without authorization. Prosecutors said Nelson is currently incarcerated in Kentucky in connection with unrelated investigation.

If convicted on the conspiracy charge, both defendants would face a statutory maximum penalty of five years in federal prison. The charge of intentionally accessing without authorization a computer carries a maximum possible sentence of five years. A conviction on the additional charge against Nelson — aggravated identity theft — carries a mandatory two-year consecutive sentence.

Update, 11:48 a.m., Dec. 20: Added statement from Ring. Modified description of a “holder” in the SIM-swapping parlance.

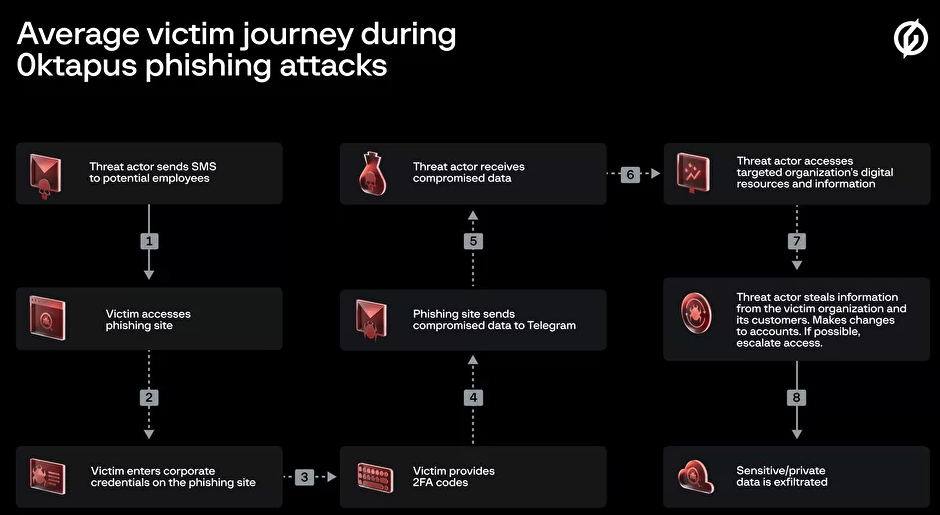

Phishers are enjoying remarkable success using text messages to steal remote access credentials and one-time passcodes from employees at some of the world’s largest technology companies and customer support firms. A recent spate of SMS phishing attacks from one cybercriminal group has spawned a flurry of breach disclosures from affected companies, which are all struggling to combat the same lingering security threat: The ability of scammers to interact directly with employees through their mobile devices.

![]()

In mid-June 2022, a flood of SMS phishing messages began targeting employees at commercial staffing firms that provide customer support and outsourcing to thousands of companies. The missives asked users to click a link and log in at a phishing page that mimicked their employer’s Okta authentication page. Those who submitted credentials were then prompted to provide the one-time password needed for multi-factor authentication.

The phishers behind this scheme used newly-registered domains that often included the name of the target company, and sent text messages urging employees to click on links to these domains to view information about a pending change in their work schedule.

The phishing sites leveraged a Telegram instant message bot to forward any submitted credentials in real-time, allowing the attackers to use the phished username, password and one-time code to log in as that employee at the real employer website. But because of the way the bot was configured, it was possible for security researchers to capture the information being sent by victims to the public Telegram server.

This data trove was first reported by security researchers at Singapore-based Group-IB, which dubbed the campaign “0ktapus” for the attackers targeting organizations using identity management tools from Okta.com.

“This case is of interest because despite using low-skill methods it was able to compromise a large number of well-known organizations,” Group-IB wrote. “Furthermore, once the attackers compromised an organization they were quickly able to pivot and launch subsequent supply chain attacks, indicating that the attack was planned carefully in advance.”

It’s not clear how many of these phishing text messages were sent out, but the Telegram bot data reviewed by KrebsOnSecurity shows they generated nearly 10,000 replies over approximately two months of sporadic SMS phishing attacks targeting more than a hundred companies.

A great many responses came from those who were apparently wise to the scheme, as evidenced by the hundreds of hostile replies that included profanity or insults aimed at the phishers: The very first reply recorded in the Telegram bot data came from one such employee, who responded with the username “havefuninjail.”

Still, thousands replied with what appear to be legitimate credentials — many of them including one-time codes needed for multi-factor authentication. On July 20, the attackers turned their sights on internet infrastructure giant Cloudflare.com, and the intercepted credentials show at least three employees fell for the scam.

Image: Cloudflare.com

In a blog post earlier this month, Cloudflare said it detected the account takeovers and that no Cloudflare systems were compromised. Cloudflare said it does not rely on one-time passcodes as a second factor, so there was nothing to provide to the attackers. But Cloudflare said it wanted to call attention to the phishing attacks because they would probably work against most other companies.

“This was a sophisticated attack targeting employees and systems in such a way that we believe most organizations would be likely to be breached,” Cloudflare CEO Matthew Prince wrote. “On July 20, 2022, the Cloudflare Security team received reports of employees receiving legitimate-looking text messages pointing to what appeared to be a Cloudflare Okta login page. The messages began at 2022-07-20 22:50 UTC. Over the course of less than 1 minute, at least 76 employees received text messages on their personal and work phones. Some messages were also sent to the employees family members.”

On three separate occasions, the phishers targeted employees at Twilio.com, a San Francisco based company that provides services for making and receiving text messages and phone calls. It’s unclear how many Twilio employees received the SMS phishes, but the data suggest at least four Twilio employees responded to a spate of SMS phishing attempts on July 27, Aug. 2, and Aug. 7.

![]()

On that last date, Twilio disclosed that on Aug. 4 it became aware of unauthorized access to information related to a limited number of Twilio customer accounts through a sophisticated social engineering attack designed to steal employee credentials.

“This broad based attack against our employee base succeeded in fooling some employees into providing their credentials,” Twilio said. “The attackers then used the stolen credentials to gain access to some of our internal systems, where they were able to access certain customer data.”

That “certain customer data” included information on roughly 1,900 users of the secure messaging app Signal, which relied on Twilio to provide phone number verification services. In its disclosure on the incident, Signal said that with their access to Twilio’s internal tools the attackers were able to re-register those users’ phone numbers to another device.

On Aug. 25, food delivery service DoorDash disclosed that a “sophisticated phishing attack” on a third-party vendor allowed attackers to gain access to some of DoorDash’s internal company tools. DoorDash said intruders stole information on a “small percentage” of users that have since been notified. TechCrunch reported last week that the incident was linked to the same phishing campaign that targeted Twilio.

This phishing gang apparently had great success targeting employees of all the major mobile wireless providers, but most especially T-Mobile. Between July 10 and July 16, dozens of T-Mobile employees fell for the phishing messages and provided their remote access credentials.

“Credential theft continues to be an ongoing issue in our industry as wireless providers are constantly battling bad actors that are focused on finding new ways to pursue illegal activities like this,” T-Mobile said in a statement. “Our tools and teams worked as designed to quickly identify and respond to this large-scale smishing attack earlier this year that targeted many companies. We continue to work to prevent these types of attacks and will continue to evolve and improve our approach.”

This same group saw hundreds of responses from employees at some of the largest customer support and staffing firms, including Teleperformanceusa.com, Sitel.com and Sykes.com. Teleperformance did not respond to requests for comment. KrebsOnSecurity did hear from Christopher Knauer, global chief security officer at Sitel Group, the customer support giant that recently acquired Sykes. Knauer said the attacks leveraged newly-registered domains and asked employees to approve upcoming changes to their work schedules.

Image: Group-IB.

Knauer said the attackers set up the phishing domains just minutes in advance of spamming links to those domains in phony SMS alerts to targeted employees. He said such tactics largely sidestep automated alerts generated by companies that monitor brand names for signs of new phishing domains being registered.

“They were using the domains as soon as they became available,” Knauer said. “The alerting services don’t often let you know until 24 hours after a domain has been registered.”

On July 28 and again on Aug. 7, several employees at email delivery firm Mailchimp provided their remote access credentials to this phishing group. According to an Aug. 12 blog post, the attackers used their access to Mailchimp employee accounts to steal data from 214 customers involved in cryptocurrency and finance.

On Aug. 15, the hosting company DigitalOcean published a blog post saying it had severed ties with MailChimp after its Mailchimp account was compromised. DigitalOcean said the MailChimp incident resulted in a “very small number” of DigitalOcean customers experiencing attempted compromises of their accounts through password resets.

According to interviews with multiple companies hit by the group, the attackers are mostly interested in stealing access to cryptocurrency, and to companies that manage communications with people interested in cryptocurrency investing. In an Aug. 3 blog post from email and SMS marketing firm Klaviyo.com, the company’s CEO recounted how the phishers gained access to the company’s internal tools, and used that to download information on 38 crypto-related accounts.

A flow chart of the attacks by the SMS phishing group known as 0ktapus and ScatterSwine. Image: Amitai Cohen for Wiz.io. twitter.com/amitaico.

The ubiquity of mobile phones became a lifeline for many companies trying to manage their remote employees throughout the Coronavirus pandemic. But these same mobile devices are fast becoming a liability for organizations that use them for phishable forms of multi-factor authentication, such as one-time codes generated by a mobile app or delivered via SMS.

Because as we can see from the success of this phishing group, this type of data extraction is now being massively automated, and employee authentication compromises can quickly lead to security and privacy risks for the employer’s partners or for anyone in their supply chain.

Unfortunately, a great many companies still rely on SMS for employee multi-factor authentication. According to a report this year from Okta, 47 percent of workforce customers deploy SMS and voice factors for multi-factor authentication. That’s down from 53 percent that did so in 2018, Okta found.

Some companies (like Knauer’s Sitel) have taken to requiring that all remote access to internal networks be managed through work-issued laptops and/or mobile devices, which are loaded with custom profiles that can’t be accessed through other devices.

Others are moving away from SMS and one-time code apps and toward requiring employees to use physical FIDO multi-factor authentication devices such as security keys, which can neutralize phishing attacks because any stolen credentials can’t be used unless the phishers also have physical access to the user’s security key or mobile device.

This came in handy for Twitter, which announced last year that it was moving all of its employees to using security keys, and/or biometric authentication via their mobile device. The phishers’ Telegram bot reported that on June 16, 2022, five employees at Twitter gave away their work credentials. In response to questions from KrebsOnSecurity, Twitter confirmed several employees were relieved of their employee usernames and passwords, but that its security key requirement prevented the phishers from abusing that information.

Twitter accelerated its plans to improve employee authentication following the July 2020 security incident, wherein several employees were phished and relieved of credentials for Twitter’s internal tools. In that intrusion, the attackers used Twitter’s tools to hijack accounts for some of the world’s most recognizable public figures, executives and celebrities — forcing those accounts to tweet out links to bitcoin scams.

“Security keys can differentiate legitimate sites from malicious ones and block phishing attempts that SMS 2FA or one-time password (OTP) verification codes would not,” Twitter said in an Oct. 2021 post about the change. “To deploy security keys internally at Twitter, we migrated from a variety of phishable 2FA methods to using security keys as our only supported 2FA method on internal systems.”

Update, 6:02 p.m. ET: Clarified that Cloudflare does not rely on TOTP (one-time multi-factor authentication codes) as a second factor for employee authentication.

It’s been seven years since the online cheating site AshleyMadison.com was hacked and highly sensitive data about its users posted online. The leak led to the public shaming and extortion of many Ashley Madison users, and to at least two suicides. To date, little is publicly known about the perpetrators or the true motivation for the attack. But a recent review of Ashley Madison mentions across Russian cybercrime forums and far-right websites in the months leading up to the hack revealed some previously unreported details that may deserve further scrutiny.

![]()

As first reported by KrebsOnSecurity on July 19, 2015, a group calling itself the “Impact Team” released data sampled from millions of users, as well as maps of internal company servers, employee network account information, company bank details and salary information.

The Impact Team said it decided to publish the information because ALM “profits on the pain of others,” and in response to a paid “full delete” service Ashley Madison parent firm Avid Life Media offered that allowed members to completely erase their profile information for a $19 fee.

According to the hackers, although the delete feature promised “removal of site usage history and personally identifiable information from the site,” users’ purchase details — including real name and address — weren’t actually scrubbed.

“Full Delete netted ALM $1.7mm in revenue in 2014. It’s also a complete lie,” the hacking group wrote. “Users almost always pay with credit card; their purchase details are not removed as promised, and include real name and address, which is of course the most important information the users want removed.”

A snippet of the message left behind by the Impact Team.

The Impact Team said ALM had one month to take Ashley Madison offline, along with a sister property called Established Men. The hackers promised that if a month passed and the company did not capitulate, it would release “all customer records, including profiles with all the customers’ secret sexual fantasies and matching credit card transactions, real names and addresses, and employee documents and emails.”

Exactly 30 days later, on Aug. 18, 2015, the Impact Team posted a “Time’s up!” message online, along with links to 60 gigabytes of Ashley Madison user data.

One aspect of the Ashley Madison breach that’s always bothered me is how the perpetrators largely cast themselves as fighting a crooked company that broke their privacy promises, and how this narrative was sustained at least until the Impact Team decided to leak all of the stolen user account data in August 2015.

Granted, ALM had a lot to answer for. For starters, after the breach it became clear that a great many of the female Ashley Madison profiles were either bots or created once and never used again. Experts combing through the leaked user data determined that fewer than one percent of the female profiles on Ashley Madison had been used on a regular basis, and the rest were used just once — on the day they were created. On top of that, researchers found 84 percent of the profiles were male.

But the Impact Team had to know that ALM would never comply with their demands to dismantle Ashley Madison and Established Men. In 2014, ALM reported revenues of $115 million. There was little chance the company was going to shut down some of its biggest money machines.

Hence, it appears the Impact Team’s goal all along was to create prodigious amounts of drama and tension by announcing the hack of a major cheating website, and then letting that drama play out over the next few months as millions of exposed Ashley Madison users freaked out and became the targets of extortion attacks and public shaming.

Robert Graham, CEO of Errata Security, penned a blog post in 2015 concluding that the moral outrage professed by the Impact Team was pure posturing.

“They appear to be motivated by the immorality of adultery, but in all probability, their motivation is that #1 it’s fun and #2 because they can,” Graham wrote.

Per Thorsheim, a security researcher in Norway, told Wired at the time that he believed the Impact Team was motivated by an urge to destroy ALM with as much aggression as they could muster.

“It’s not just for the fun and ‘because we can,’ nor is it just what I would call ‘moralistic fundamentalism,'” Thorsheim told Wired. “Given that the company had been moving toward an IPO right before the hack went public, the timing of the data leaks was likely no coincidence.”

As the seventh anniversary of the Ashley Madison hack rolled around, KrebsOnSecurity went back and looked for any mentions of Ashley Madison or ALM on cybercrime forums in the months leading up to the Impact Team’s initial announcement of the breach on July 19, 2015. There wasn’t much, except a Russian guy offering to sell payment and contact information on 32 million AshleyMadison users, and a bunch of Nazis upset about a successful Jewish CEO promoting adultery.

![]()

Cyber intelligence firm Intel 471 recorded a series of posts by a user with the handle “Brutium” on the Russian-language cybercrime forum Antichat between 2014 and 2016. Brutium routinely advertised the sale of large, hacked databases, and on Jan. 24, 2015, this user posted a thread offering to sell data on 32 million Ashley Madison users:

“Data from July 2015

Total ~32 Million contacts:

full name; email; phone numbers; payment, etc.”

It’s unclear whether the postdated “July 2015” statement was a typo, or if Brutium updated that sales thread at some point. There is also no indication whether anyone purchased the information. Brutium’s profile has since been removed from the Antichat forum.

Flashpoint is a threat intelligence company in New York City that keeps tabs on hundreds of cybercrime forums, as well as extremist and hate websites. A search in Flashpoint for mentions of Ashley Madison or ALM prior to July 19, 2015 shows that in the six months leading up to the hack, Ashley Madison and its then-CEO Noel Biderman became a frequent subject of derision across multiple neo-Nazi websites.

On Jan. 14, 2015, a member of the neo-Nazi forum Stormfront posted a lively thread about Ashley Madison in the general discussion area titled, “Jewish owned dating website promoting adultery.”

On July 3, 2015, Andrew Anglin, the editor of the alt-right publication Daily Stormer, posted excerpts about Biderman from a story titled, “Jewish Hyper-Sexualization of Western Culture,” which referred to Biderman as the “Jewish King of Infidelity.”

On July 10, a mocking montage of Biderman photos with racist captions was posted to the extremist website Vanguard News Network, as part of a thread called “Jews normalize sexual perversion.”

“Biderman himself says he’s a happily married father of two and does not cheat,” reads the story posted by Anglin on the Daily Stormer. “In an interview with the ‘Current Affair’ program in Australia, he admitted that if he found out his own wife was accessing his cheater’s site, ‘I would be devastated.'”

The leaked AshleyMadison data included more than three years’ worth of emails stolen from Biderman. The hackers told Motherboard in 2015 they had 300 GB worth of employee emails, but that they saw no need to dump the inboxes of other company employees.

Several media outlets pounced on salacious exchanges in Biderman’s emails as proof he had carried on multiple affairs. Biderman resigned as CEO on Aug. 28, 2015. The last message in the archive of Biderman’s stolen emails was dated July 7, 2015 — almost two weeks before the Impact Team would announce their hack.

Biderman told KrebsOnSecurity on July 19, 2015 that the company believed the hacker was some type of insider.

“We’re on the doorstep of [confirming] who we believe is the culprit, and unfortunately that may have triggered this mass publication,” Biderman said. “I’ve got their profile right in front of me, all their work credentials. It was definitely a person here that was not an employee but certainly had touched our technical services.”

Certain language in the Impact Team’s manifesto seemed to support this theory, such as the line: “For a company whose main promise is secrecy, it’s like you didn’t even try, like you thought you had never pissed anyone off.”

But despite ALM offering a belated $500,000 reward for information leading to the arrest and conviction of those responsible, to this day no one has been charged in connection with the hack.

Twice in the past month KrebsOnSecurity has heard from readers who had their accounts at big-three credit bureau Experian hacked and updated with a new email address that wasn’t theirs. In both cases the readers used password managers to select strong, unique passwords for their Experian accounts. Research suggests identity thieves were able to hijack the accounts simply by signing up for new accounts at Experian using the victim’s personal information and a different email address.

![]()

John Turner is a software engineer based in Salt Lake City. Turner said he created the account at Experian in 2020 to place a security freeze on his credit file, and that he used a password manager to select and store a strong, unique password for his Experian account.

Turner said that in early June 2022 he received an email from Experian saying the email address on his account had been changed. Experian’s password reset process was useless at that point because any password reset links would be sent to the new (impostor’s) email address.

An Experian support person Turner reached via phone after a lengthy hold time asked for his Social Security Number (SSN) and date of birth, as well as his account PIN and answers to his secret questions. But the PIN and secret questions had already been changed by whoever re-signed up as him at Experian.

“I was able to answer the credit report questions successfully, which authenticated me to their system,” Turner said. “At that point, the representative read me the current stored security questions and PIN, and they were definitely not things I would have used.”

Turner said he was able to regain control over his Experian account by creating a new account. But now he’s wondering what else he could do to prevent another account compromise.

“The most frustrating part of this whole thing is that I received multiple ‘here’s your login information’ emails later that I attributed to the original attackers coming back and attempting to use the ‘forgot email/username’ flow, likely using my SSN and DOB, but it didn’t go to their email that they were expecting,” Turner said. “Given that Experian doesn’t support two-factor authentication of any kind — and that I don’t know how they were able to get access to my account in the first place — I’ve felt very helpless ever since.”

Arthur Rishi is a musician and co-executive director of the Boston Landmarks Orchestra. Rishi said he recently discovered his Experian account had been hijacked after receiving an alert from his credit monitoring service (not Experian’s) that someone had tried to open an account in his name at JPMorgan Chase.

Rishi said the alert surprised him because his credit file at Experian was frozen at the time, and Experian did not notify him about any activity on his account. Rishi said Chase agreed to cancel the unauthorized account application, and even rescinded its credit inquiry (each credit pull can ding your credit score slightly).

But he never could get anyone from Experian’s support to answer the phone, despite spending what seemed like eternity trying to progress through the company’s phone-based system. That’s when Rishi decided to see if he could create a new account for himself at Experian.

“I was able to open a new account at Experian starting from scratch, using my SSN, date of birth and answering some really basic questions, like what kind of car did you take out a loan for, or what city did you used to live in,’ Rishi said.

Upon completing the sign-up, Rishi noticed that his credit was unfrozen.

Like Turner, Rishi is now worried that identity thieves will just hijack his Experian account once more, and that there is nothing he can do to prevent such a scenario. For now, Rishi has decided to pay Experian $25.99 a month to more closely monitor his account for suspicious activity. Even using the paid Experian service, there were no additional multi-factor authentication options available, although he said Experian did send a one-time code to his phone via SMS recently when he logged on.

“Experian now sometimes does require MFA for me if I use a new browser or have my VPN on,” Rishi said, but he’s not sure if Experian’s free service would have operated differently.

“I get so angry when I think about all this,” he said. “I have no confidence this won’t happen again.”

In a written statement, Experian suggested that what happened to Rishi and Turner was not a normal occurrence, and that its security and identity verification practices extend beyond what is visible to the user.

“We believe these are isolated incidents of fraud using stolen consumer information,” Experian’s statement reads. “Specific to your question, once an Experian account is created, if someone attempts to create a second Experian account, our systems will notify the original email on file.”

“We go beyond reliance on personally identifiable information (PII) or a consumer’s ability to answer knowledge-based authentication questions to access our systems,” the statement continues. “We do not disclose additional processes for obvious security reasons; however, our data and analytical capabilities verify identity elements across multiple data sources and are not visible to the consumer. This is designed to create a more positive experience for our consumers and to provide additional layers of protection. We take consumer privacy and security seriously, and we continually review our security processes to guard against constant and evolving threats posed by fraudsters.”

KrebsOnSecurity sought to replicate Turner and Rishi’s experience — to see if Experian would allow me to re-create my account using my personal information but a different email address. The experiment was done from a different computer and Internet address than the one that created the original account years ago.

After providing my Social Security Number (SSN), date of birth, and answering several multiple choice questions whose answers are derived almost entirely from public records, Experian promptly changed the email address associated with my credit file. It did so without first confirming that new email address could respond to messages, or that the previous email address approved the change.

Experian’s system then sent an automated message to the original email address on file, saying the account’s email address had been changed. The only recourse Experian offered in the alert was to sign in, or send an email to an Experian inbox that replies with the message, “this email address is no longer monitored.”

![]()

After that, Experian prompted me to select new secret questions and answers, as well as a new account PIN — effectively erasing the account’s previously chosen PIN and recovery questions. Once I’d changed the PIN and security questions, Experian’s site helpfully reminded me that I have a security freeze on file, and would I like to remove or temporarily lift the security freeze?

To be clear, Experian does have a business unit that sells one-time password services to businesses. While Experian’s system did ask for a mobile number when I signed up a second time, at no time did that number receive a notification from Experian. Also, I could see no option in my account to enable multi-factor authentication for all logins.

How does Experian differ from the practices of Equifax and TransUnion, the other two big consumer credit reporting bureaus? When KrebsOnSecurity tried to re-create an existing account at TransUnion using my Social Security number, TransUnion rejected the application, noting that I already had an account and prompting me to proceed through its lost password flow. The company also appears to send an email to the address on file asking to validate account changes.

Likewise, trying to recreate an existing account at Equifax using personal information tied to my existing account prompts Equifax’s systems to report that I already have an account, and to use their password reset process (which involves sending a verification email to the address on file).