It’s not unusual for the data brokers behind people-search websites to use pseudonyms in their day-to-day lives (you would, too). Some of these personal data purveyors even try to reinvent their online identities in a bid to hide their conflicts of interest. But it’s not every day you run across a US-focused people-search network based in China whose principal owners all appear to be completely fabricated identities.

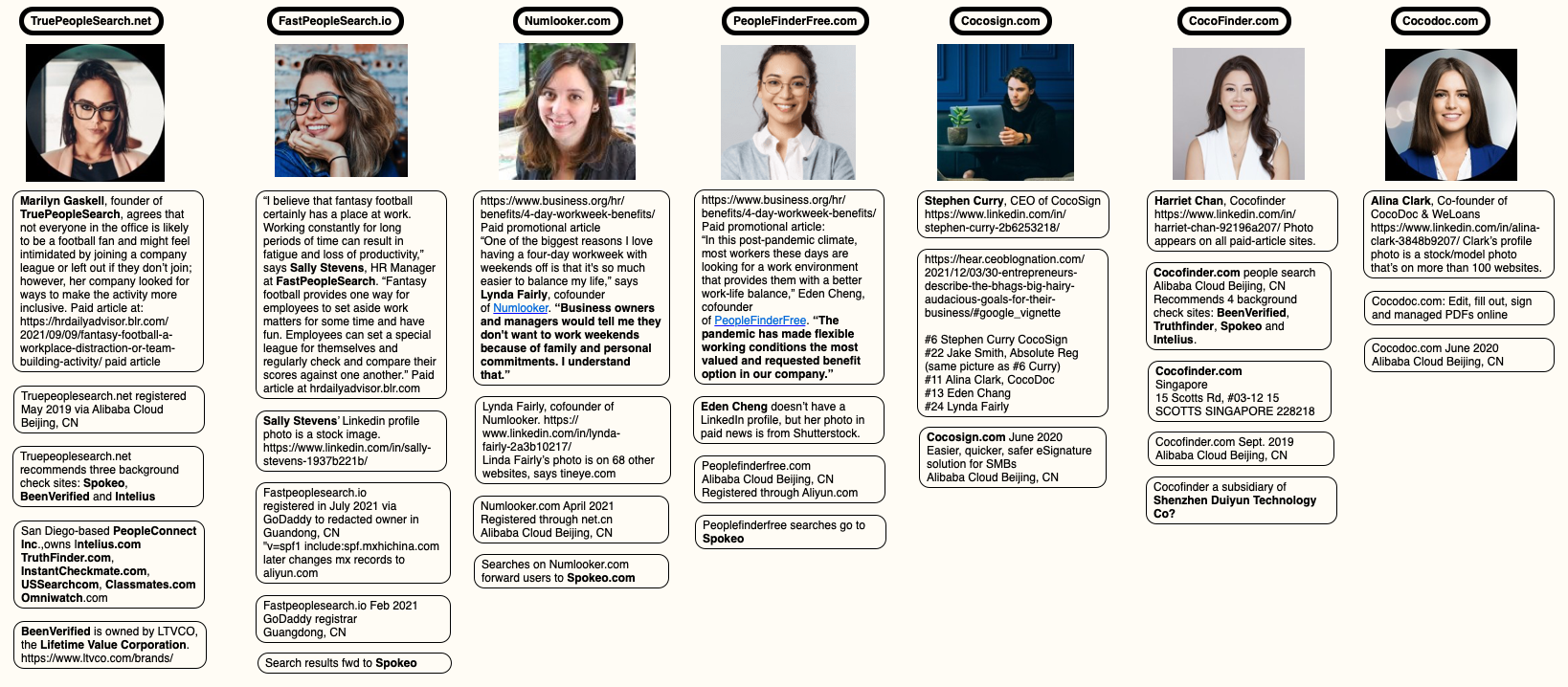

Responding to a reader inquiry concerning the trustworthiness of a site called TruePeopleSearch[.]net, KrebsOnSecurity began poking around. The site offers to sell reports containing photos, police records, background checks, civil judgments, contact information “and much more!” According to LinkedIn and numerous profiles on websites that accept paid article submissions, the founder of TruePeopleSearch is Marilyn Gaskell from Phoenix, Ariz.

The saucy yet studious LinkedIn profile for Marilyn Gaskell.

Ms. Gaskell has been quoted in multiple “articles” about random subjects, such as this article at HRDailyAdvisor about the pros and cons of joining a company-led fantasy football team.

“Marilyn Gaskell, founder of TruePeopleSearch, agrees that not everyone in the office is likely to be a football fan and might feel intimidated by joining a company league or left out if they don’t join; however, her company looked for ways to make the activity more inclusive,” this paid story notes.

Also quoted in this article is Sally Stevens, who is cited as HR Manager at FastPeopleSearch[.]io.

Sally Stevens, the phantom HR Manager for FastPeopleSearch.

“Fantasy football provides one way for employees to set aside work matters for some time and have fun,” Stevens contributed. “Employees can set a special league for themselves and regularly check and compare their scores against one another.”

Imagine that: Two different people-search companies mentioned in the same story about fantasy football. What are the odds?

Both TruePeopleSearch and FastPeopleSearch allow users to search for reports by first and last name, but proceeding to order a report prompts the visitor to purchase the file from one of several established people-finder services, including BeenVerified, Intelius, and Spokeo.

DomainTools.com shows that both TruePeopleSearch and FastPeopleSearch appeared around 2020 and were registered through Alibaba Cloud, in Beijing, China. No other information is available about these domains in their registration records, although both domains appear to use email servers based in China.

Sally Stevens’ LinkedIn profile photo is identical to a stock image titled “beautiful girl” from Adobe.com. Ms. Stevens is also quoted in a paid blog post at ecogreenequipment.com, as is Alina Clark, co-founder and marketing director of CocoDoc, an online service for editing and managing PDF documents.

The profile photo for Alina Clark is a stock photo appearing on more than 100 websites.

Scouring multiple image search sites reveals Ms. Clark’s profile photo on LinkedIn is another stock image that is currently on more than 100 different websites, including Adobe.com. Cocodoc[.]com was registered in June 2020 via Alibaba Cloud Beijing in China.

The same Alina Clark and photo materialized in a paid article at the website Ceoblognation, which in 2021 included her at #11 in a piece called “30 Entrepreneurs Describe The Big Hairy Audacious Goals (BHAGs) for Their Business.” It’s also worth noting that Ms. Clark is currently listed as a “former Forbes Council member” at the media outlet Forbes.com.

Entrepreneur #6 is Stephen Curry, who is quoted as CEO of CocoSign[.]com, a website that claims to offer an “easier, quicker, safer eSignature solution for small and medium-sized businesses.” Incidentally, the same photo for Stephen Curry #6 is also used in this “article” for #22 Jake Smith, who is named as the owner of a different company.

Stephen Curry, aka Jake Smith, aka no such person.

Mr. Curry’s LinkedIn profile shows a young man seated at a table in front of a laptop, but an online image search shows this is another stock photo. Cocosign[.]com was registered in June 2020 via Alibaba Cloud Beijing. No ownership details are available in the domain registration records.

Listed at #13 in that 30 Entrepreneurs article is Eden Cheng, who is cited as co-founder of PeopleFinderFree[.]com. KrebsOnSecurity could not find a LinkedIn profile for Ms. Cheng, but a search on her profile image from that Entrepreneurs article shows the same photo for sale at Shutterstock and other stock photo sites.

DomainTools says PeopleFinderFree was registered through Alibaba Cloud, Beijing. Attempts to purchase reports through PeopleFinderFree produce a notice saying the full report is only available via Spokeo.com.

Lynda Fairly is Entrepreneur #24, and she is quoted as co-founder of Numlooker[.]com, a domain registered in April 2021 through Alibaba in China. Searches for people on Numlooker forward visitors to Spokeo.

![]()

The photo next to Ms. Fairly’s quote in Entrepreneurs matches that of a LinkedIn profile for Lynda Fairly. But a search on that photo shows this same portrait has been used by many other identities and names, including a woman from the United Kingdom who’s a cancer survivor and mother of five; a licensed marriage and family therapist in Canada; a software security engineer at Quora; a journalist on Twitter/X; and a marketing expert in Canada.

Cocofinder[.]com is a people-search service that launched in Sept. 2019, through Alibaba in China. Cocofinder lists its market officer as Harriet Chan, but Ms. Chan’s LinkedIn profile is just as sparse on work history as the other people-search owners mentioned already. An image search online shows that outside of LinkedIn, the profile photo for Ms. Chan has only ever appeared in articles at pay-to-play media sites, like this one from outbackteambuilding.com.

Perhaps because Cocodoc and Cocosign both sell software services, they are actually tied to a physical presence in the real world — in Singapore (15 Scotts Rd. #03-12 15, Singapore). But it’s difficult to discern much from this address alone.

Who’s behind all this people-search chicanery? A January 2024 review of various people-search services at the website techjury.com states that Cocofinder is a wholly-owned subsidiary of a Chinese company called Shenzhen Duiyun Technology Co.

“Though it only finds results from the United States, users can choose between four main search methods,” Techjury explains. Those include people search, phone, address and email lookup. This claim is supported by a Reddit post from three years ago, wherein the Reddit user “ProtectionAdvanced” named the same Chinese company.

Is Shenzhen Duiyun Technology Co. responsible for all these phony profiles? How many more fake companies and profiles are connected to this scheme? KrebsOnSecurity found other examples that didn’t appear directly tied to other fake executives listed here, but which nevertheless are registered through Alibaba and seek to drive traffic to Spokeo and other data brokers. For example, there’s the winsome Daniela Sawyer, founder of FindPeopleFast[.]net, whose profile is flogged in paid stories at entrepreneur.org.

Google currently turns up nothing else for in a search for Shenzhen Duiyun Technology Co. Please feel free to sound off in the comments if you have any more information about this entity, such as how to contact it. Or reach out directly at krebsonsecurity @ gmail.com.

A mind map highlighting the key points of research in this story. Click to enlarge. Image: KrebsOnSecurity.com

It appears the purpose of this network is to conceal the location of people in China who are seeking to generate affiliate commissions when someone visits one of their sites and purchases a people-search report at Spokeo, for example. And it is clear that Spokeo and others have created incentives wherein anyone can effectively white-label their reports, and thereby make money brokering access to peoples’ personal information.

Spokeo’s Wikipedia page says the company was founded in 2006 by four graduates from Stanford University. Spokeo co-founder and current CEO Harrison Tang has not yet responded to requests for comment.

Intelius is owned by San Diego based PeopleConnect Inc., which also owns Classmates.com, USSearch, TruthFinder and Instant Checkmate. PeopleConnect Inc. in turn is owned by H.I.G. Capital, a $60 billion private equity firm. Requests for comment were sent to H.I.G. Capital. This story will be updated if they respond.

BeenVerified is owned by a New York City based holding company called The Lifetime Value Co., a marketing and advertising firm whose brands include PeopleLooker, NeighborWho, Ownerly, PeopleSmart, NumberGuru, and Bumper, a car history site.

Ross Cohen, chief operating officer at The Lifetime Value Co., said it’s likely the network of suspicious people-finder sites was set up by an affiliate. Cohen said Lifetime Value would investigate to determine if this particular affiliate was driving them any sign-ups.

All of the above people-search services operate similarly. When you find the person you’re looking for, you are put through a lengthy (often 10-20 minute) series of splash screens that require you to agree that these reports won’t be used for employment screening or in evaluating new tenant applications. Still more prompts ask if you are okay with seeing “potentially shocking” details about the subject of the report, including arrest histories and photos.

Only at the end of this process does the site disclose that viewing the report in question requires signing up for a monthly subscription, which is typically priced around $35. Exactly how and from where these major people-search websites are getting their consumer data — and customers — will be the subject of further reporting here.

The main reason these various people-search sites require you to affirm that you won’t use their reports for hiring or vetting potential tenants is that selling reports for those purposes would classify these firms as consumer reporting agencies (CRAs) and expose them to regulations under the Fair Credit Reporting Act (FCRA).

These data brokers do not want to be treated as CRAs, and for this reason their people search reports typically don’t include detailed credit histories, financial information, or full Social Security Numbers (Radaris reports include the first six digits of one’s SSN).

But in September 2023, the U.S. Federal Trade Commission found that TruthFinder and Instant Checkmate were trying to have it both ways. The FTC levied a $5.8 million penalty against the companies for allegedly acting as CRAs because they assembled and compiled information on consumers into background reports that were marketed and sold for employment and tenant screening purposes.

The FTC also found TruthFinder and Instant Checkmate deceived users about background report accuracy. The FTC alleges these companies made millions from their monthly subscriptions using push notifications and marketing emails that claimed that the subject of a background report had a criminal or arrest record, when the record was merely a traffic ticket.

The FTC said both companies deceived customers by providing “Remove” and “Flag as Inaccurate” buttons that did not work as advertised. Rather, the “Remove” button removed the disputed information only from the report as displayed to that customer; however, the same item of information remained visible to other customers who searched for the same person.

The FTC also said that when a customer flagged an item in the background report as inaccurate, the companies never took any steps to investigate those claims, to modify the reports, or to flag to other customers that the information had been disputed.

There are a growing number of online reputation management companies that offer to help customers remove their personal information from people-search sites and data broker databases. There are, no doubt, plenty of honest and well-meaning companies operating in this space, but it has been my experience that a great many people involved in that industry have a background in marketing or advertising — not privacy.

Also, some so-called data privacy companies may be wolves in sheep’s clothing. On March 14, KrebsOnSecurity published an abundance of evidence indicating that the CEO and founder of the data privacy company OneRep.com was responsible for launching dozens of people-search services over the years.

Finally, some of the more popular people-search websites are notorious for ignoring requests from consumers seeking to remove their information, regardless of which reputation or removal service you use. Some force you to create an account and provide more information before you can remove your data. Even then, the information you worked hard to remove may simply reappear a few months later.

This aptly describes countless complaints lodged against the data broker and people search giant Radaris. On March 8, KrebsOnSecurity profiled the co-founders of Radaris, two Russian brothers in Massachusetts who also operate multiple Russian-language dating services and affiliate programs.

The truth is that these people-search companies will continue to thrive unless and until Congress begins to realize it’s time for some consumer privacy and data protection laws that are relevant to life in the 21st century. Duke University adjunct professor Justin Sherman says virtually all state privacy laws exempt records that might be considered “public” or “government” documents, including voting registries, property filings, marriage certificates, motor vehicle records, criminal records, court documents, death records, professional licenses, bankruptcy filings, and more.

“Consumer privacy laws in California, Colorado, Connecticut, Delaware, Indiana, Iowa, Montana, Oregon, Tennessee, Texas, Utah, and Virginia all contain highly similar or completely identical carve-outs for ‘publicly available information’ or government records,” Sherman said.

![]()

When U.S. consumers have their online bank accounts hijacked and plundered by hackers, U.S. financial institutions are legally obligated to reverse any unauthorized transactions as long as the victim reports the fraud in a timely manner. But new data released this week suggests that for some of the nation’s largest banks, reimbursing account takeover victims has become more the exception than the rule.

The findings came in a report released by Sen. Elizabeth Warren (D-Mass.), who in April 2022 opened an investigation into fraud tied to Zelle, the “peer-to-peer” digital payment service used by many financial institutions that allows customers to quickly send cash to friends and family.

Zelle is run by Early Warning Services LLC (EWS), a private financial services company which is jointly owned by Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank, and Wells Fargo. Zelle is enabled by default for customers at over 1,000 different financial institutions, even if a great many customers still don’t know it’s there.

Sen. Warren said several of the EWS owner banks — including Capital One, JPMorgan and Wells Fargo — failed to provide all of the requested data. But Warren did get the requested information from PNC, Truist and U.S. Bank.

“Overall, the three banks that provided complete data sets reported 35,848 cases of scams, involving over $25.9 million of payments in 2021 and the first half of 2022,” the report summarized. “In the vast majority of these cases, the banks did not repay the customers that reported being scammed. Overall these three banks reported repaying customers in only 3,473 cases (representing nearly 10% of scam claims) and repaid only $2.9 million.”

Importantly, the report distinguishes between cases that involve straight up bank account takeovers and unauthorized transfers (fraud), and those losses that stem from “fraudulently induced payments,” where the victim is tricked into authorizing the transfer of funds to scammers (scams).

A common example of the latter is the Zelle Fraud Scam, which uses an ever-shifting set of come-ons to trick people into transferring money to fraudsters. The Zelle Fraud Scam often employs text messages and phone calls spoofed to look like they came from your bank, and the scam usually relates to fooling the customer into thinking they’re sending money to themselves when they’re really sending it to the crooks.

Here’s the rub: When a customer issues a payment order to their bank, the bank is obligated to honor that order so long as it passes a two-stage test. The first question asks, Did the request actually come from an authorized owner or signer on the account? In the case of Zelle scams, the answer is yes.

Trace Fooshee, a strategic advisor in the anti money laundering practice at Aite-Novarica, said the second stage requires banks to give the customer’s transfer order a kind of “sniff test” using “commercially reasonable” fraud controls that generally are not designed to detect patterns involving social engineering.

Fooshee said the legal phrase “commercially reasonable” is the primary reason why no bank has much — if anything — in the way of controlling for scam detection.

“In order for them to deploy something that would detect a good chunk of fraud on something so hard to detect they would generate egregiously high rates of false positives which would also make consumers (and, then, regulators) very unhappy,” Fooshee said. “This would tank the business case for the service as a whole rendering it something that the bank can claim to NOT be commercially reasonable.”

Sen. Warren’s report makes clear that banks generally do not pay consumers back if they are fraudulently induced into making Zelle payments.

“In simple terms, Zelle indicated that it would provide redress for users in cases of unauthorized transfers in which a user’s account is accessed by a bad actor and used to transfer a payment,” the report continued. “However, EWS’ response also indicated that neither Zelle nor its parent bank owners would reimburse users fraudulently induced by a bad actor into making a payment on the platform.”

Still, the data suggest banks did repay at least some of the funds stolen from scam victims about 10 percent of the time. Fooshee said he’s surprised that number is so high.

“That banks are paying victims of authorized payment fraud scams anything at all is noteworthy,” he said. “That’s money that they’re paying for out of pocket almost entirely for goodwill. You could argue that repaying all victims is a sound strategy especially in the climate we’re in but to say that it should be what all banks do remains an opinion until Congress changes the law.”

However, when it comes to reimbursing victims of fraud and account takeovers, the report suggests banks are stiffing their customers whenever they can get away with it. “Overall, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received,” the report notes.

How did the banks behave individually? From the report:

-In 2021 and the first six months of 2022, PNC Bank indicated that its customers reported 10,683 cases of unauthorized payments totaling over $10.6 million, of which only 1,495 cases totaling $1.46 were refunded to consumers. PNC Bank left 86% of its customers that reported cases of fraud without recourse for fraudulent activity that occurred on Zelle.

-Over this same time period, U.S. Bank customers reported a total of 28,642 cases of unauthorized transactions totaling over $16.2 million, while only refunding 8,242 cases totaling less than $4.7 million.

-In the period between January 2021 and September 2022, Bank of America customers reported 81,797 cases of unauthorized transactions, totaling $125 million. Bank of America refunded only $56.1 million in fraud claims – less than 45% of the overall dollar value of claims made in that time.

–Truist indicated that the bank had a much better record of reimbursing defrauded customers over this same time period. During 2021 and the first half of 2022, Truist customers filed 24,752 unauthorized transaction claims amounting to $24.4 million. Truist reimbursed 20,349 of those claims, totaling $20.8 million – 82% of Truist claims were reimbursed over this period. Overall, however, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received.

Fooshee said there has long been a great deal of inconsistency in how banks reimburse unauthorized fraud claims — even after the Consumer Financial Protection Bureau (CPFB) came out with guidance on what qualifies as an unauthorized fraud claim.

“Many banks reported that they were still not living up to those standards,” he said. “As a result, I imagine that the CFPB will come down hard on those with fines and we’ll see a correction.”

Fooshee said many banks have recently adjusted their reimbursement policies to bring them more into line with the CFPB’s guidance from last year.

“So this is heading in the right direction but not with sufficient vigor and speed to satisfy critics,” he said.

Seth Ruden is a payments fraud expert who serves as director of global advisory for digital identity company BioCatch. Ruden said Zelle has recently made “significant changes to its fraud program oversight because of consumer influence.”

“It is clear to me that despite sensational headlines, progress has been made to improve outcomes,” Ruden said. “Presently, losses in the network on a volume-adjusted basis are lower than those typical of credit cards.”

But he said any failure to reimburse victims of fraud and account takeovers only adds to pressure on Congress to do more to help victims of those scammed into authorizing Zelle payments.

“The bottom line is that regulations have not kept up with the speed of payment technology in the United States, and we’re not alone,” Ruden said. “For the first time in the UK, authorized payment scam losses have outpaced credit card losses and a regulatory response is now on the table. Banks have the choice right now to take action and increase controls or await regulators to impose a new regulatory environment.”

Sen. Warren’s report is available here (PDF).

![]()

There are, of course, some versions of the Zelle fraud scam that may be confusing financial institutions as to what constitutes “authorized” payment instructions. For example, the variant I wrote about earlier this year began with a text message that spoofed the target’s bank and warned of a pending suspicious transfer.

Those who responded at all received a call from a number spoofed to make it look like the victim’s bank calling, and were asked to validate their identities by reading back a one-time password sent via SMS. In reality, the thieves had simply asked the bank’s website to reset the victim’s password, and that one-time code sent via text by the bank’s site was the only thing the crooks needed to reset the target’s password and drain the account using Zelle.

None of the above discussion involves the risks affecting businesses that bank online. Businesses in the United States do not enjoy the same fraud liability protection afforded to consumers, and if a banking trojan or clever phishing site results in a business account getting drained, most banks will not reimburse that loss.

This is why I have always and will continue to urge small business owners to conduct their online banking affairs only from a dedicated, access restricted and security-hardened device — and preferably a non-Windows machine.

For consumers, the same old advice remains the best: Watch your bank statements like a hawk, and immediately report and contest any charges that appear fraudulent or unauthorized.