Authorities in Australia, the United Kingdom and the United States this week levied financial sanctions against a Russian man accused of stealing data on nearly 10 million customers of the Australian health insurance giant Medibank. 33-year-old Aleksandr Ermakov allegedly stole and leaked the Medibank data while working with one of Russia’s most destructive ransomware groups, but little more is shared about the accused. Here’s a closer look at the activities of Mr. Ermakov’s alleged hacker handles.

Aleksandr Ermakov, 33, of Russia. Image: Australian Department of Foreign Affairs and Trade.

The allegations against Ermakov mark the first time Australia has sanctioned a cybercriminal. The documents released by the Australian government included multiple photos of Mr. Ermakov, and it was clear they wanted to send a message that this was personal.

It’s not hard to see why. The attackers who broke into Medibank in October 2022 stole 9.7 million records on current and former Medibank customers. When the company refused to pay a $10 million ransom demand, the hackers selectively leaked highly sensitive health records, including those tied to abortions, HIV and alcohol abuse.

The U.S. government says Ermakov and the other actors behind the Medibank hack are believed to be linked to the Russia-backed cybercrime gang REvil.

“REvil was among the most notorious cybercrime gangs in the world until July 2021 when they disappeared. REvil is a ransomware-as-a-service (RaaS) operation and generally motivated by financial gain,” a statement from the U.S. Department of the Treasury reads. “REvil ransomware has been deployed on approximately 175,000 computers worldwide, with at least $200 million paid in ransom.”

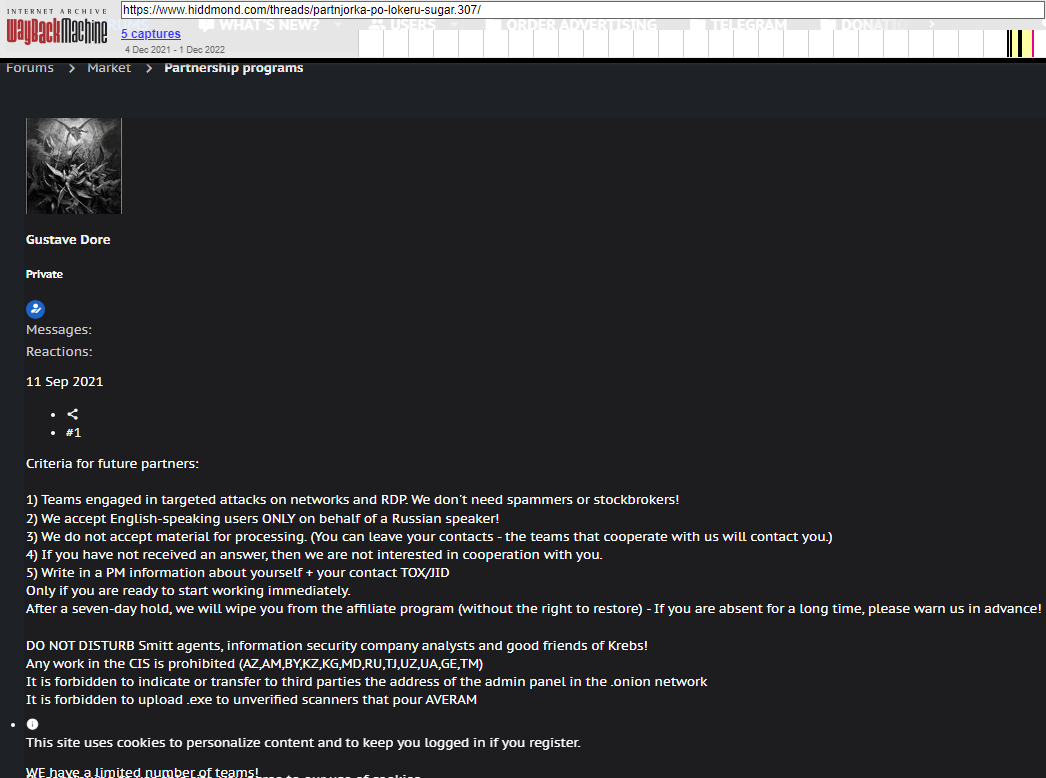

The sanctions say Ermakov went by multiple aliases on Russian cybercrime forums, including GustaveDore, JimJones, and Blade Runner. A search on the handle GustaveDore at the cyber intelligence platform Intel 471 shows this user created a ransomware affiliate program in November 2021 called Sugar (a.k.a. Encoded01), which focused on targeting single computers and end-users instead of corporations.

An ad for the ransomware-as-a-service program Sugar posted by GustaveDore warns readers against sharing information with security researchers, law enforcement, or “friends of Krebs.”

In November 2020, Intel 471 analysts concluded that GustaveDore’s alias JimJones “was using and operating several different ransomware strains, including a private undisclosed strain and one developed by the REvil gang.”

In 2020, GustaveDore advertised on several Russian discussion forums that he was part of a Russian technology firm called Shtazi, which could be hired for computer programming, web development, and “reputation management.” Shtazi’s website remains in operation today.

A Google-translated version of Shtazi dot ru. Image: Archive.org.

The third result when one searches for shtazi[.]ru in Google is an Instagram post from a user named Mikhail Borisovich Shefel, who promotes Shtazi’s services as if it were also his business. If this name sounds familiar, it’s because in December 2023 KrebsOnSecurity identified Mr. Shefel as “Rescator,” the cybercriminal identity tied to tens of millions of payment cards that were stolen in 2013 and 2014 from big box retailers Target and Home Depot, among others.

How close was the connection between GustaveDore and Mr. Shefel? The Treasury Department’s sanctions page says Ermakov used the email address ae.ermak@yandex.ru. A search for this email at DomainTools.com shows it was used to register just one domain name: millioner1[.]com. DomainTools further finds that a phone number tied to Mr. Shefel (79856696666) was used to register two domains: millioner[.]pw, and shtazi[.]net.

The December 2023 story here that outed Mr. Shefel as Rescator noted that Shefel recently changed his last name to “Lenin” and had launched a service called Lenin[.]biz that sells physical USSR-era Ruble notes bearing the image of Vladimir Lenin, the founding father of the Soviet Union. The Instagram account for Mr. Shefel includes images of stacked USSR-era Ruble notes, as well as multiple links to Shtazi.

The Instagram account of Mikhail Borisovich Shefel, aka MikeMike aka Rescator.

Intel 471’s research revealed Ermakov was affiliated in some way with REvil because the stolen Medibank data was published on a blog that had one time been controlled by REvil affiliates who carried out attacks and paid an affiliate fee to the gang.

But by the time of the Medibank hack, the REvil group had mostly scattered after a series of high-profile attacks led to the group being disrupted by law enforcement. In November 2021, Europol announced it arrested seven REvil affiliates who collectively made more than $230 million worth of ransom demands since 2019. At the same time, U.S. authorities unsealed two indictments against a pair of accused REvil cybercriminals.

“The posting of Medibank’s data on that blog, however, indicated a connection with that group, although the connection wasn’t clear at the time,” Intel 471 wrote. “This makes sense in retrospect, as Ermakov’s group had also been a REvil affiliate.”

It is easy to dismiss sanctions like these as ineffective, because as long as Mr. Ermakov remains in Russia he has little to fear of arrest. However, his alleged role as an apparent top member of REvil paints a target on him as someone who likely possesses large sums of cryptocurrency, said Patrick Gray, the Australian co-host and founder of the security news podcast Risky Business.

“I’ve seen a few people poo-poohing the sanctions…but the sanctions component is actually less important than the doxing component,” Gray said. “Because this guy’s life just got a lot more complicated. He’s probably going to have to pay some bribes to stay out of trouble. Every single criminal in Russia now knows he is a vulnerable 33 year old with an absolute ton of bitcoin. So this is not a happy time for him.”

Update, Feb. 21, 1:10 p.m. ET: The Russian security firm F.A.C.C.T reports that Ermakov has been arrested in Russia, and charged with violating domestic laws that prohibit the creation, use and distribution of malicious computer programs.

“During the investigation, several defendants were identified who were not only promoting their ransomware, but also developing custom-made malicious software, creating phishing sites for online stores, and driving user traffic to fraudulent schemes popular in Russia and the CIS,” F.A.C.C.T. wrote. “Among those detained was the owner of the nicknames blade_runner, GistaveDore, GustaveDore, JimJones.”

A shocking number of organizations — including banks and healthcare providers — are leaking private and sensitive information from their public Salesforce Community websites, KrebsOnSecurity has learned. The data exposures all stem from a misconfiguration in Salesforce Community that allows an unauthenticated user to access records that should only be available after logging in.

A researcher found DC Health had five Salesforce Community sites exposing data.

Salesforce Community is a widely-used cloud-based software product that makes it easy for organizations to quickly create websites. Customers can access a Salesforce Community website in two ways: Authenticated access (requiring login), and guest user access (no login required). The guest access feature allows unauthenticated users to view specific content and resources without needing to log in.

However, sometimes Salesforce administrators mistakenly grant guest users access to internal resources, which can cause unauthorized users to access an organization’s private information and lead to potential data leaks.

Until being contacted by this reporter on Monday, the state of Vermont had at least five separate Salesforce Community sites that allowed guest access to sensitive data, including a Pandemic Unemployment Assistance program that exposed the applicant’s full name, Social Security number, address, phone number, email, and bank account number.

This misconfigured Salesforce Community site from the state of Vermont was leaking pandemic assistance loan application data, including names, SSNs, email address and bank account information.

Vermont’s Chief Information Security Officer Scott Carbee said his security teams have been conducting a full review of their Salesforce Community sites, and already found one additional Salesforce site operated by the state that was also misconfigured to allow guest access to sensitive information.

“My team is frustrated by the permissive nature of the platform,” Carbee said.

Carbee said the vulnerable sites were all created rapidly in response to the Coronavirus pandemic, and were not subjected to their normal security review process.

“During the pandemic, we were largely standing up tons of applications, and let’s just say a lot of them didn’t have the full benefit of our dev/ops process,” Carbee said. “In our case, we didn’t have any native Salesforce developers when we had to suddenly stand up all these sites.”

Earlier this week, KrebsOnSecurity notified Columbus, Ohio-based Huntington Bank that its recently acquired TCF Bank had a Salesforce Community website that was leaking documents related to commercial loans. The data fields in those loan applications included name, address, full Social Security number, title, federal ID, IP address, average monthly payroll, and loan amount.

Huntington Bank has disabled the leaky TCF Bank Salesforce website. Matthew Jennings, deputy chief information security officer at Huntington, said the company was still investigating how the misconfiguration occurred, how long it lasted, and how many records may have been exposed.

KrebsOnSecurity learned of the leaks from security researcher Charan Akiri, who said he wrote a program that identified hundreds of other organizations running misconfigured Salesforce pages. But Akiri said he’s been wary of probing too far, and has had difficulty getting responses from most of the organizations he has notified to date.

“In January and February 2023, I contacted government organizations and several companies, but I did not receive any response from these organizations,” Akiri said. “To address the issue further, I reached out to several CISOs on LinkedIn and Twitter. As a result, five companies eventually fixed the problem. Unfortunately, I did not receive any responses from government organizations.”

The problem Akiri has been trying to raise awareness about came to the fore in August 2021, when security researcher Aaron Costello published a blog post explaining how misconfigurations in Salesforce Community sites could be exploited to reveal sensitive data (Costello subsequently published a follow-up post detailing how to lock down Salesforce Community sites).

On Monday, KrebsOnSecurity used Akiri’s findings to notify Washington D.C. city administrators that at least five different public DC Health websites were leaking sensitive information. One DC Health Salesforce Community website designed for health professionals seeking to renew licenses with the city leaked documents that included the applicant’s full name, address, Social Security number, date of birth, license number and expiration, and more.

Akiri said he notified the Washington D.C. government in February about his findings, but received no response. Reached by KrebsOnSecurity, interim Chief Information Security Officer Mike Rupert initially said the District had hired a third party to investigate, and that the third party confirmed the District’s IT systems were not vulnerable to data loss from the reported Salesforce configuration issue.

But after being presented with a document including the Social Security number of a health professional in D.C. that was downloaded in real-time from the DC Health public Salesforce website, Rupert acknowledged his team had overlooked some configuration settings.

Washington, D.C. health administrators are still smarting from a data breach earlier this year at the health insurance exchange DC Health Link, which exposed personal information for more than 56,000 users, including many members of Congress.

That data later wound up for sale on a top cybercrime forum. The Associated Press reports that the DC Health Link breach was likewise the result of human error, and said an investigation revealed the cause was a DC Health Link server that was “misconfigured to allow access to the reports on the server without proper authentication.”

Salesforce says the data exposures are not the result of a vulnerability inherent to the Salesforce platform, but they can occur when customers’ access control permissions are misconfigured.

“As previously communicated to all Experience Site and Sites customers, we recommend utilizing the Guest User Access Report Package to assist in reviewing access control permissions for unauthenticated users,” reads a Salesforce advisory from Sept. 2022. “Additionally, we suggest reviewing the following Help article, Best Practices and Considerations When Configuring the Guest User Profile.”

In a written statement, Salesforce said it is actively focused on data security for organizations with guest users, and that it continues to release “robust tools and guidance for our customers,” including:

Control Which Users Experience Cloud Site Users Can See

Best Practices and Considerations When Configuring the Guest User Profile

“We’ve also continued to update our Guest User security policies, beginning with our Spring ‘21 release with more to come in Summer ‘23,” the statement reads. “Lastly, we continue to proactively communicate with customers to help them understand the capabilities available to them, and how they can best secure their instance of Salesforce to meet their security, contractual, and regulatory obligations.”

![]()

When U.S. consumers have their online bank accounts hijacked and plundered by hackers, U.S. financial institutions are legally obligated to reverse any unauthorized transactions as long as the victim reports the fraud in a timely manner. But new data released this week suggests that for some of the nation’s largest banks, reimbursing account takeover victims has become more the exception than the rule.

The findings came in a report released by Sen. Elizabeth Warren (D-Mass.), who in April 2022 opened an investigation into fraud tied to Zelle, the “peer-to-peer” digital payment service used by many financial institutions that allows customers to quickly send cash to friends and family.

Zelle is run by Early Warning Services LLC (EWS), a private financial services company which is jointly owned by Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank, and Wells Fargo. Zelle is enabled by default for customers at over 1,000 different financial institutions, even if a great many customers still don’t know it’s there.

Sen. Warren said several of the EWS owner banks — including Capital One, JPMorgan and Wells Fargo — failed to provide all of the requested data. But Warren did get the requested information from PNC, Truist and U.S. Bank.

“Overall, the three banks that provided complete data sets reported 35,848 cases of scams, involving over $25.9 million of payments in 2021 and the first half of 2022,” the report summarized. “In the vast majority of these cases, the banks did not repay the customers that reported being scammed. Overall these three banks reported repaying customers in only 3,473 cases (representing nearly 10% of scam claims) and repaid only $2.9 million.”

Importantly, the report distinguishes between cases that involve straight up bank account takeovers and unauthorized transfers (fraud), and those losses that stem from “fraudulently induced payments,” where the victim is tricked into authorizing the transfer of funds to scammers (scams).

A common example of the latter is the Zelle Fraud Scam, which uses an ever-shifting set of come-ons to trick people into transferring money to fraudsters. The Zelle Fraud Scam often employs text messages and phone calls spoofed to look like they came from your bank, and the scam usually relates to fooling the customer into thinking they’re sending money to themselves when they’re really sending it to the crooks.

Here’s the rub: When a customer issues a payment order to their bank, the bank is obligated to honor that order so long as it passes a two-stage test. The first question asks, Did the request actually come from an authorized owner or signer on the account? In the case of Zelle scams, the answer is yes.

Trace Fooshee, a strategic advisor in the anti money laundering practice at Aite-Novarica, said the second stage requires banks to give the customer’s transfer order a kind of “sniff test” using “commercially reasonable” fraud controls that generally are not designed to detect patterns involving social engineering.

Fooshee said the legal phrase “commercially reasonable” is the primary reason why no bank has much — if anything — in the way of controlling for scam detection.

“In order for them to deploy something that would detect a good chunk of fraud on something so hard to detect they would generate egregiously high rates of false positives which would also make consumers (and, then, regulators) very unhappy,” Fooshee said. “This would tank the business case for the service as a whole rendering it something that the bank can claim to NOT be commercially reasonable.”

Sen. Warren’s report makes clear that banks generally do not pay consumers back if they are fraudulently induced into making Zelle payments.

“In simple terms, Zelle indicated that it would provide redress for users in cases of unauthorized transfers in which a user’s account is accessed by a bad actor and used to transfer a payment,” the report continued. “However, EWS’ response also indicated that neither Zelle nor its parent bank owners would reimburse users fraudulently induced by a bad actor into making a payment on the platform.”

Still, the data suggest banks did repay at least some of the funds stolen from scam victims about 10 percent of the time. Fooshee said he’s surprised that number is so high.

“That banks are paying victims of authorized payment fraud scams anything at all is noteworthy,” he said. “That’s money that they’re paying for out of pocket almost entirely for goodwill. You could argue that repaying all victims is a sound strategy especially in the climate we’re in but to say that it should be what all banks do remains an opinion until Congress changes the law.”

However, when it comes to reimbursing victims of fraud and account takeovers, the report suggests banks are stiffing their customers whenever they can get away with it. “Overall, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received,” the report notes.

How did the banks behave individually? From the report:

-In 2021 and the first six months of 2022, PNC Bank indicated that its customers reported 10,683 cases of unauthorized payments totaling over $10.6 million, of which only 1,495 cases totaling $1.46 were refunded to consumers. PNC Bank left 86% of its customers that reported cases of fraud without recourse for fraudulent activity that occurred on Zelle.

-Over this same time period, U.S. Bank customers reported a total of 28,642 cases of unauthorized transactions totaling over $16.2 million, while only refunding 8,242 cases totaling less than $4.7 million.

-In the period between January 2021 and September 2022, Bank of America customers reported 81,797 cases of unauthorized transactions, totaling $125 million. Bank of America refunded only $56.1 million in fraud claims – less than 45% of the overall dollar value of claims made in that time.

–Truist indicated that the bank had a much better record of reimbursing defrauded customers over this same time period. During 2021 and the first half of 2022, Truist customers filed 24,752 unauthorized transaction claims amounting to $24.4 million. Truist reimbursed 20,349 of those claims, totaling $20.8 million – 82% of Truist claims were reimbursed over this period. Overall, however, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received.

Fooshee said there has long been a great deal of inconsistency in how banks reimburse unauthorized fraud claims — even after the Consumer Financial Protection Bureau (CPFB) came out with guidance on what qualifies as an unauthorized fraud claim.

“Many banks reported that they were still not living up to those standards,” he said. “As a result, I imagine that the CFPB will come down hard on those with fines and we’ll see a correction.”

Fooshee said many banks have recently adjusted their reimbursement policies to bring them more into line with the CFPB’s guidance from last year.

“So this is heading in the right direction but not with sufficient vigor and speed to satisfy critics,” he said.

Seth Ruden is a payments fraud expert who serves as director of global advisory for digital identity company BioCatch. Ruden said Zelle has recently made “significant changes to its fraud program oversight because of consumer influence.”

“It is clear to me that despite sensational headlines, progress has been made to improve outcomes,” Ruden said. “Presently, losses in the network on a volume-adjusted basis are lower than those typical of credit cards.”

But he said any failure to reimburse victims of fraud and account takeovers only adds to pressure on Congress to do more to help victims of those scammed into authorizing Zelle payments.

“The bottom line is that regulations have not kept up with the speed of payment technology in the United States, and we’re not alone,” Ruden said. “For the first time in the UK, authorized payment scam losses have outpaced credit card losses and a regulatory response is now on the table. Banks have the choice right now to take action and increase controls or await regulators to impose a new regulatory environment.”

Sen. Warren’s report is available here (PDF).

![]()

There are, of course, some versions of the Zelle fraud scam that may be confusing financial institutions as to what constitutes “authorized” payment instructions. For example, the variant I wrote about earlier this year began with a text message that spoofed the target’s bank and warned of a pending suspicious transfer.

Those who responded at all received a call from a number spoofed to make it look like the victim’s bank calling, and were asked to validate their identities by reading back a one-time password sent via SMS. In reality, the thieves had simply asked the bank’s website to reset the victim’s password, and that one-time code sent via text by the bank’s site was the only thing the crooks needed to reset the target’s password and drain the account using Zelle.

None of the above discussion involves the risks affecting businesses that bank online. Businesses in the United States do not enjoy the same fraud liability protection afforded to consumers, and if a banking trojan or clever phishing site results in a business account getting drained, most banks will not reimburse that loss.

This is why I have always and will continue to urge small business owners to conduct their online banking affairs only from a dedicated, access restricted and security-hardened device — and preferably a non-Windows machine.

For consumers, the same old advice remains the best: Watch your bank statements like a hawk, and immediately report and contest any charges that appear fraudulent or unauthorized.