With passwords and MFA out of the way, let’s next look at connected apps or services that are tied to our priority accounts. When you log into other sites on the web through Facebook, Google, or another social account, as well as when you install social media apps or games, you are sharing information about those accounts with those services. This may be as limited as the email address and username on file, or may include much more information like your friends list, contacts, likes/subscriptions, or more.

A well-known example of this data-harvesting method is the Cambridge Analytica story, where installing a social media app opened up access to much more information than users realized. (Note: as mentioned in the linked article, Facebook added protective measures to limit the amount of data available to app developers, but connected accounts can still present a liability if misused.)

With this in mind, look under the Security or Privacy section of each of your account’s settings, and review where you have either used this account to log into a third-party website or allowed access when installing an app. Here are some handy links to some of the most common services to check:

If you aren’t going to use the app again or don’t want to share any details, remove them. Once you’ve checked your accounts, repeat this process with all the apps installed on your phone.

Just like connecting a social account to a third-party game can share information like your contact info and friend’s list, installing an app on your mobile device can share information including your contacts, camera roll and more. Fortunately, mobile OSes have gotten much better at notifying users before installation on what information is shared, so you should be able to see which apps might be nosier than you’re comfortable with.

Finally — and this is really for the nerds and techies out there — check if you have any API (short for “application programming interface”) keys or browser extensions connected to your accounts. API keys are commonly used to let different apps or services “talk” between one another. They let you use services like Zapier or IFTTT to do things like have your Spotify favorites automatically saved to a Google Sheet, or check Weather Underground to send a daily email with the forecast.

Browser extensions let you customize a web browser and integrate services, like quickly clicking to save an article for review on a “read it later” service like Instapaper. Even if you trust the developer when installing these apps, they may pose a risk later on if they are recovered or taken over by an attacker. These “zombie extensions” rely on a broad install base from a legitimate service which can later be misused to gather information or launch attacks by a malicious developer.

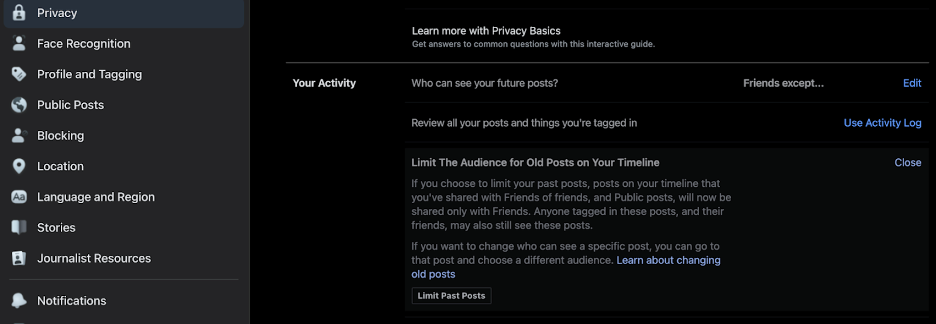

We’ve made great progress already, and taken steps to help defend your accounts from prying eyes going forward – now it’s time to lock down your previous activities on social media. Rather than enumerate every option on every service, I’ll highlight some common tools and privacy settings you’ll want to check:

Before moving on to email, I’ll add another plug for the NYT Social Media Security and Privacy Checklists if you, like me, would rather have a series of boxes to mark off while going through each step above.

Security experts know that you can’t erase the possibility of risk, and it can be counterproductive to build a plan to that expectation. What is realistic and achievable is identifying risk so you know what you’re up against, mitigating risk by following security best practices, and isolating risk where possible so that in the event of an incident, one failure doesn’t have a domino effect affecting other resources. If that seems a bit abstract, let’s take a look at a practical example.

Tech journalist Mat Honan was the unlucky victim of a targeted hack, which resulted in a near-complete lockout from his digital life requiring a Herculean effort to recover. Fortunately for us, Mat documented his experience in the Wired story, “How Apple and Amazon Security Flaws Led to My Epic Hacking,” which offers an excellent summary of exactly the type of domino effect I described. I encourage you to read the full article, but for a CliffsNotes version sufficient for our needs here:

Honan’s article goes into much more detail, including some of the changes made by the services exploited to prevent similar incidents in the future. The key takeaway is that having a couple of emails without strong authentication tied to all his most important accounts, including the recovery of these email accounts themselves, meant that the compromise of his Amazon account quickly snowballed into something much bigger.

We’re going to learn from that painful lesson, and do some segmentation on our email channels based on the priority and how public we want that account to be. (“Segmentation” is an industry term that can be mostly boiled down to “don’t put all your eggs in one basket”, and keep critical or vulnerable resources separate from each other.) I would suggest setting up a few different emails, listed here from least- to most-public:

For all of the above, of course, we’ll create strong passwords and set up 2FA. And speaking of 2FA, you can use the same split-channel approach we followed for email to set up a dedicated verification number (using a VOIP service or something like Google Voice) when sending a passcode by SMS is the only option supported. Keeping these recovery numbers separate from your main phone number reduces the risk of them being leaked, sold, or captured in an unrelated breach.

Good news: We’re almost done with doxxing ourselves! In the next section, we’ll sweep out those unused accounts to avoid leaving data-filled loose ends and take a look at how data brokers profit off of your personal information and what you can do to opt-out.

You’ve made it this far so maybe you’re passionate like we are about developing innovative ways to make security accessible. We’d love for you to join our mission.

We’d love to hear what you think. Ask a Question, Comment Below, and Stay Connected with Cisco Secure on social!

Cisco Secure Social Channels

card-fan-1200

pic-1200

The concept of zero trust is not a new one, and some may even argue that the term is overused. In reality, however, its criticality is growing with each passing day. Why? Because many of today’s attacks begin with the user. According to Verizon’s Data Breach Investigations Report, 82% of breaches involve the human element — whether it’s stolen credentials, phishing, misuse or error.

Additionally, today’s businesses are hyper-connected, meaning that — in addition to your employees — customers, partners and suppliers are all part of your ecosystem. Couple that with hybrid work, IoT, the move to the cloud, and more emboldened attackers, and organizational risk increases exponentially.

Adopting a zero trust model can dramatically reduce this risk by eliminating implicit trust. It has become so crucial, in fact, that several governments including the U.S., UK and Australia have released mandates and guidance for how organizations should deploy zero trust to improve national security.

However, because zero trust is more of a concept than a technology, and so many vendors use the term, organizations struggle with the best way to implement it. At Cisco, we believe you should take a holistic approach to zero trust, starting with what you have and adding on as you identify gaps in your defenses. And while layers of protection are necessary for powerful security, so is ease of use.

Zero trust plays a major role in building security resilience, or the ability to withstand unpredictable threats or changes and emerge stronger. Through zero trust, the identity and security posture of users, devices and applications are continuously checked and verified to prevent network intrusions — and to also limit impact if an unauthorized entity does gain access.

Organizations with high zero trust maturity are twice as likely to achieve business resilience.

– Cisco’s Guide to Zero Trust Maturity

Eliminating trust, however, doesn’t really conjure up images of user-friendly technology. No matter how necessary they are for the business, employees are unlikely to embrace security measures that make their jobs more cumbersome and time-consuming. Instead, they want fast, consistent access to any application no matter where they are or which device they are using.

That’s why Cisco is taking a different approach to zero trust — one that removes friction for the user. For example, with Cisco Secure Access by Duo, organizations can provide those connecting to their network with several quick, easy authentication options. This way, they can put in place multi-factor authentication (MFA) that frustrates attackers, not users.

Cisco Secure Access by Duo is a key pillar of zero trust security, providing industry-leading features for secure access, authentication and device monitoring. Duo is customizable, straightforward to use, and simple to set up. It enables the use of modern authentication methods including biometrics, passwordless and single sign-on (SSO) to help organizations advance zero trust without sacrificing user experience. Duo also provides the flexibility organizations need to enable secure remote access with or without a VPN connection.

During Cisco’s own roll-out of Duo to over 100,000 people, less than 1% of users contacted the help desk for assistance. On an annual basis, Duo is saving Cisco $3.4 million in employee productivity and $500,000 in IT help desk support costs. Furthermore, 86,000 potential compromises are averted by Duo each month.

La-Z-Boy, one of the world’s leading residential furniture producers, also wanted to defend its employees against cybersecurity breaches through MFA and zero trust. It needed a data security solution that worked agnostically, could grow with the company, and that was easy to roll out and implement.

“When COVID first hit and people were sent home to work remotely, we started seeing more hacking activity…” said Craig Vincent, director of IT infrastructure and operations at La-Z-Boy. “We were looking for opportunities to secure our environment with a second factor…. We knew that even post-pandemic we would need a hybrid solution.”

“It was very quick and easy to see where Duo fit into our environment quite well, and worked with any application or legacy app, while deploying quickly.” – Craig Vincent, Director of IT Infrastructure and Operations, La-Z-Boy

Today, Duo helps La-Z-Boy maintain a zero trust framework, stay compliant, and get clear visibility into what is connecting to its network and VPN. Zero trust helps La-Z-Boy secure its organization against threats such as phishing, stolen credentials and out-of-date devices that may be vulnerable to known exploits and malware.

As mentioned, zero trust is a framework, not a single product or technology. For zero trust to be truly effective, it must do four things:

Many technology companies may offer a single component of zero trust, or one aspect of protection, but Cisco’s robust networking and security expertise enables us to provide a holistic zero trust solution. Not only can we support all the steps above, but we can do so across your whole IT ecosystem.

Modern organizations are operating multi-environment ecosystems that include a mix of on-premises and cloud technologies from various vendors. Zero trust solutions should be able to protect across all this infrastructure, no matter which providers are in use. Protections should also extend from the network and cloud to users, devices, applications and data. With Cisco’s extensive security portfolio, operating on multiple clouds and platforms, zero trust controls can be embedded at every layer.

Depending on where you are in your security journey, embedding zero trust at every layer of your infrastructure may sound like a lofty endeavor. That’s why we meet customers where they are on their path to zero trust. Whether your first priority is to meet regulatory requirements, secure hybrid work, protect the cloud, or something else, we have the expertise to help you get started. We provide clear guidance and technologies for zero trust security mapped to established frameworks from organizations like CISA and NIST.

Much of our Cisco Secure portfolio can be used to build a successful zero trust framework, but some examples of what we offer include:

All of our technologies and services are backed by the unparalleled intelligence of Cisco Talos — so you always have up-to-date protection as you build your zero trust architecture. Additionally, our open, integrated security platform — Cisco SecureX — makes it simple to expand and scale your security controls, knowing they will work with your other technologies for more unified defenses.

As Italy’s leading insurance company, Sara Assicurazioni requires complete visibility into its extended network, including a multi-cloud architecture and hybrid workforce. The company has adopted a comprehensive zero trust strategy through Cisco Secure.

“Our decentralized users, endpoints, and cloud-based servers and workloads contribute to a large attack surface,” says Paolo Perrucci, director of information and communications technology architectures and operations at Sara Assicurazioni. “With Cisco, we have the right level of visibility on this surface.”

“The main reason we chose Cisco is that only Cisco can offer a global security solution rather than covering one specific point…. Thanks to Cisco Secure, I’m quite confident that our security posture is now many times better because we are leveraging more scalable, state-of-the-art security solutions.” – Luigi Vassallo, COO & CTO, Sara Assicurazioni

To learn more, explore our zero trust page and sign up for one of our free zero trust workshops.

Watch video: How Cisco implemented zero trust in just five months

We’d love to hear what you think. Ask a Question, Comment Below, and Stay Connected with Cisco Secure on social!

Cisco Secure Social Channels

In the first step of our doxxing research, we collected a list of our online footprint, digging out the most important accounts that you want to protect and obsolete or forgotten accounts you no longer use. Because the most recent and relevant data is likely to live in the accounts you use regularly, our next step will be to review the full scope of what’s visible from these accounts and to set more intentional boundaries on what is shared.

It’s important to note here that the goal isn’t to eliminate every trace of yourself from the internet and never go online again. That’s not realistic for the vast majority of people in our connected world (and I don’t know about you, but even if it was I wouldn’t want to!) And whether it’s planning for an individual or a giant organization, security built to an impossible standard is destined to fail. Instead, we are shifting you from default to intentional sharing, and improving visibility and control over what you do want to share.

Before making changes to the settings and permissions for each of these accounts, we’re going to make sure that access to the account itself is secure. You can start with your email accounts (especially any that you use as a recovery email for forgotten passwords, or use for financial, medical, or other sensitive communications). This shouldn’t take very long for each site, and involves a few straightforward steps:

The best way to prevent a breached password from exposing another account to attack is to use a unique password for for every website you visit. And while you may have heard previous advice on strong passwords (along the lines of “eight or more characters, with a mix of upper/lower case letters, numbers, and special characters”), more recent standards emphasize the importance of longer passwords. For a great explanation of why longer passwords work better than shorter, multi-character type passwords, check out this excellent XKCD strip:

A password manager will make this process much easier, as most have the ability to generate unique passwords and allow you to tailor their length and complexity. While we’re on the topic of what makes a good password, make sure that the password to access your password manager is both long and memorable.

You don’t want to save or auto-fill that password because it acts as the “keys to the kingdom” for everything else, so I recommend following a process like the one outlined in the comic above, or another mnemonic device, to help you remember that password. Once you’ve reset the password, check for a “log out of active devices” option to make sure the new password is used.

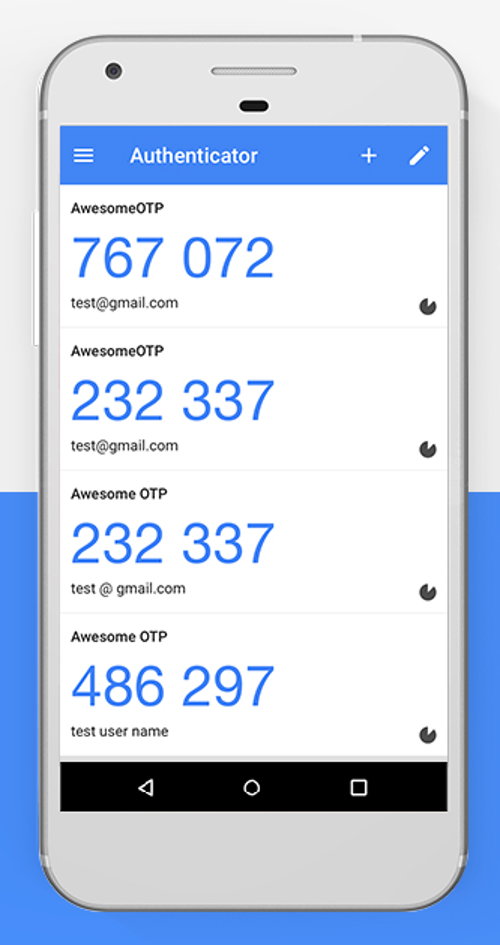

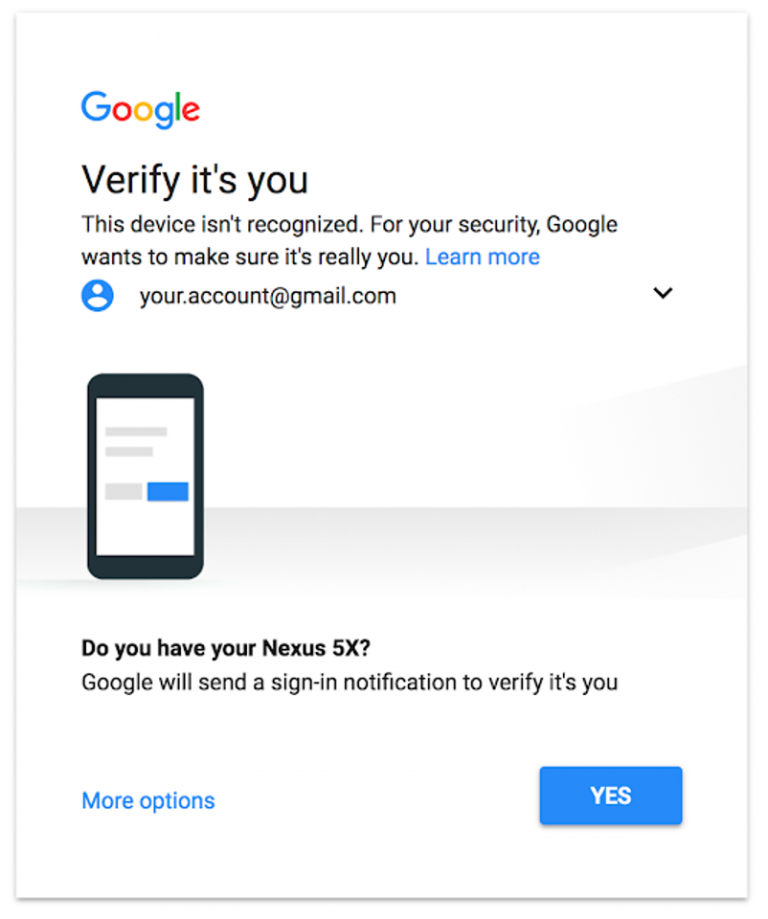

MFA uses two or more “factors” verifying something you know, something you have, or something you are. A password is an example of “something you know”, and here are a few of the most common methods used for an additional layer of security:

If you want to know more about the different ways you can log in with strong authentication and how they vary in effectiveness, check out the Google Security Team blog post “Understanding the Root Cause of Account Takeover.”

Before we move on from passwords and 2FA, I want to highlight a second step to log in that doesn’t meet the standard of strong authentication: password questions. These are usually either a secondary prompt after entering username and password, or used to verify your identity before sending a password reset link. The problem is that many of the most commonly-used questions rely on semi-public information and, like passcodes, are entered on the same device used to log in.

Another common practice is leveraging common social media quizzes/questionnaires that people post on their social media account. If you’ve seen your friends post their “stage name” by taking the name of their first pet and the street they grew up on, you may notice that’s a combination of two pretty common password questions! While not a very targeted or precise method of attack, the casual sharing of these surveys can have consequences beyond their momentary diversion.

One of the first widely-publicized doxxings happened when Paris Hilton’s contact list, notes, and photos were accessed by resetting her password using the password question, “what is your favorite pet’s name?”. Because Hilton had previously discussed her beloved chihuahua, Tinkerbell, the attacker was able to use this information to access the account.

Sometimes, though, you’ll be required to use these password questions, and in those cases I’ve got a simple rule to keep you safe: lie! That’s right, you won’t be punished if you fib when entering the answers to your password questions so that the answers can’t be researched, and most password managers also include a secure note field that will let you save your questions and answers in case you need to recall them later.

We’d love to hear what you think. Ask a Question, Comment Below, and Stay Connected with Cisco Secure on social!

Cisco Secure Social Channels

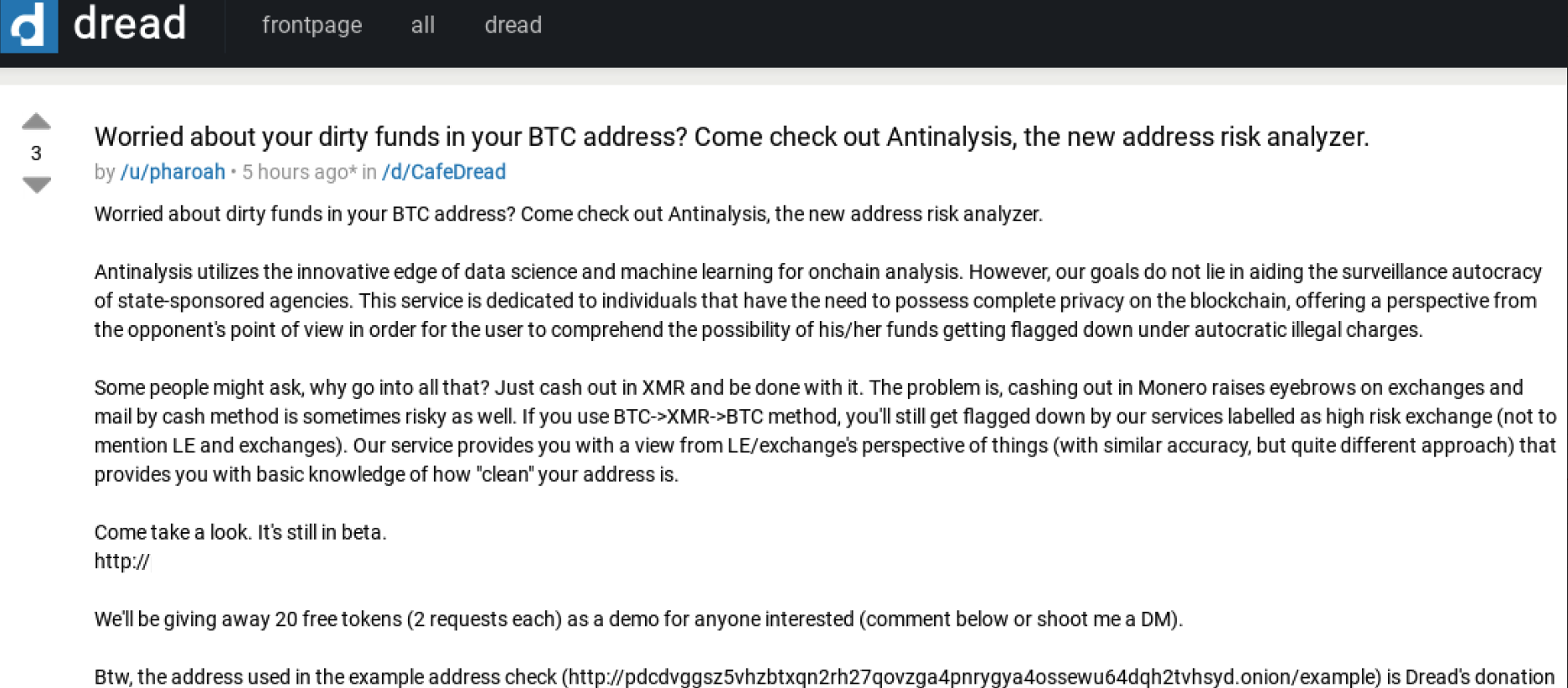

AMLBot, a service that helps businesses avoid transacting with cryptocurrency wallets that have been sanctioned for cybercrime activity, said an investigation published by KrebsOnSecurity last year helped it shut down three dark web services that secretly resold its technology to help cybercrooks avoid detection by anti-money laundering systems.

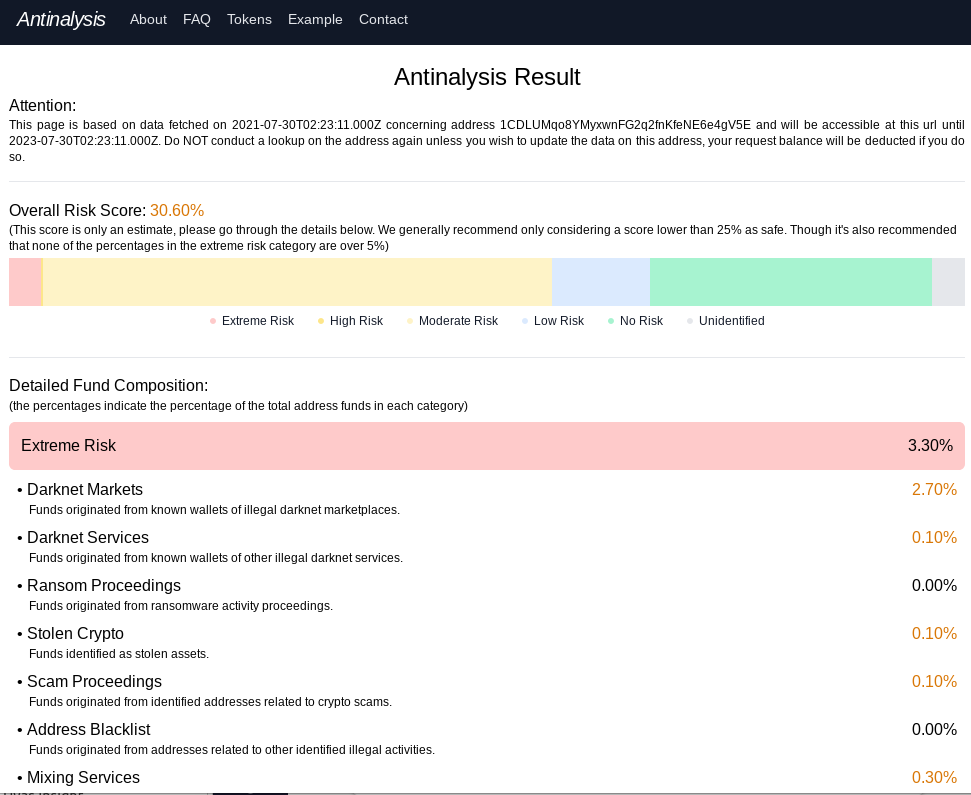

Antinalysis, as it existed in 2021.

In August 2021, KrebsOnSecurity published “New Anti Anti-Money Laundering Services for Crooks,” which examined Antinalysis, a service marketed on cybercrime forums that purported to offer a glimpse of how one’s payment activity might be flagged by law enforcement agencies and private companies that track and trace cryptocurrency transactions.

“Worried about dirty funds in your BTC address? Come check out Antinalysis, the new address risk analyzer,” read the service’s opening announcement. “This service is dedicated to individuals that have the need to possess complete privacy on the blockchain, offering a perspective from the opponent’s point of view in order for the user to comprehend the possibility of his/her funds getting flagged down under autocratic illegal charges.”

Antinalysis allows free lookups, but anyone wishing to conduct bulk look-ups has to pay at least USD $3, with a minimum $30 purchase. Other plans go for as high as $6,000 for 5,000 requests. Nick Bax, a security researcher who specializes in tracing cryptocurrency transactions, told KrebsOnSecurity at the time that Antinalysis was likely a clone of AMLBot because the two services generated near-identical results.

AMLBot shut down Antinalysis’s access just hours after last year’s story went live. However, Antinalysis[.]org remains online and accepting requests, as does the service’s Tor-based domain, and it is unclear how those services are sourcing their information.

AMLBot spokesperson Polina Smoliar said the company undertook a thorough review after that discovery, and in the process found two other services similar to Antinalysis that were reselling their application programming interface (API) access to cybercrooks.

Smoliar said that following the revelations about Antinalysis, AMLBot audited its entire client base, and implemented the ability to provide APIs only after a contract is signed and the client has been fully audited. AMLBot said it also instituted 24/7 monitoring of all client transactions.

“As a result of these actions, two more services with the name AML (the same as AMLBot has) were found to be involved in fraudulent schemes,” Smoliar said. “Information about the fraudsters was also sent to key market participants, and their transaction data was added to the tracking database to better combat money laundering.”

Experts say the founder of Antinalysis also runs a darknet market for narcotics.

The Antinalysis homepage and chatter on the cybercrime forums indicates the service was created by a group of coders known as the Incognito Team. Tom Robinson, co-founder of the blockchain intelligence firm Elliptic, said the creator of Antinalysis is also one of the developers of Incognito Market, a darknet marketplace specializing in the sale of narcotics.

“Incognito was launched in late 2020, and accepts payments in both Bitcoin and Monero, a cryptoasset offering heightened anonymity,” Robinson said. “The launch of Antinalysis likely reflects the difficulties faced by the market and its vendors in cashing out their Bitcoin proceeds.”

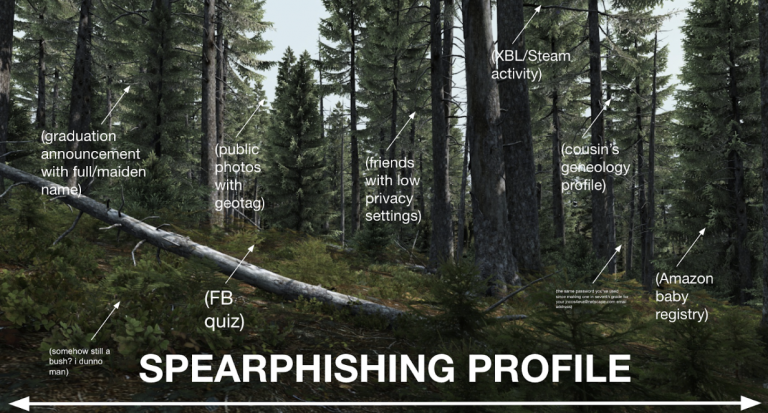

Sharing is caring… but on the internet, sharing can also be tricky! When we post something, we have to look at the forest and not just the trees. Doxxers usually start with one or two pieces of relatively innocent or public information, but by connecting the dots between those pieces they can build a frighteningly detailed picture of an individual.

Seemingly innocuous details can be pieced together into a much more personal profile when collected and leveraged to learn more. As one example, your wish list/wedding registry makes it easy for friends and family to get you gifts that you actually want, but could also be used to find out products/services you’re interested in as pretext (setting the scene) of a conversation or phishing email trying to gather more. You may have Google Alerts set up for your name (a great idea!), but this may not flag text in scanned documents such as school yearbooks, newspapers and other digitized paper records available online.

If the above sounds scary – don’t panic! Your first step in this auto-dox is going to be brainstorming as much personally identifying information (PII) shared online as possible. I suggest doing this either in a secure note or longhand. The goal is to write down all of the accounts/addresses/phone numbers that come to mind, as these are some of the top things that attackers will try to gather in their search. Start your list here:

Email addresses are an especially juicy target for someone trying to locate you, because most people only use one personal and maaaybe a second school or work email account. Those accounts are tied to all our other online identities and often double as our username for logging in.

When you finish this process, you will likely have dozens or even hundreds of “breadcrumbs” between your account list and search results. Read through your list again, and we’re going to sort it into three categories:

Great job! You’ve already got a much better idea of what people can learn about you than most folks ever do, and are well on your way to cleaning up your online footprint. In our next step, we’ll start locking down everything that you want to keep!

P.S. If you’re enjoying this process and value keeping people safe online, please check out our open roles at Cisco Secure.

We’d love to hear what you think. Ask a Question, Comment Below, and Stay Connected with Cisco Secure on social!

Cisco Secure Social Channels

Microsoft today released updates to fix at least 85 security holes in its Windows operating systems and related software, including a new zero-day vulnerability in all supported versions of Windows that is being actively exploited. However, noticeably absent from this month’s Patch Tuesday are any updates to address a pair of zero-day flaws being exploited this past month in Microsoft Exchange Server.

The new zero-day flaw– CVE-2022-41033 — is an “elevation of privilege” bug in the Windows COM+ event service, which provides system notifications when users logon or logoff. Microsoft says the flaw is being actively exploited, and that it was reported by an anonymous individual.

“Despite its relatively low score in comparison to other vulnerabilities patched today, this one should be at the top of everyone’s list to quickly patch,” said Kevin Breen, director of cyber threat research at Immersive Labs. “This specific vulnerability is a local privilege escalation, which means that an attacker would already need to have code execution on a host to use this exploit. Privilege escalation vulnerabilities are a common occurrence in almost every security compromise. Attackers will seek to gain SYSTEM or domain-level access in order to disable security tools, grab credentials with tools like Mimkatz and move laterally across the network.

Indeed, Satnam Narang, senior staff research engineer at Tenable, notes that almost half of the security flaws Microsoft patched this week are elevation of privilege bugs.

Some privilege escalation bugs can be particularly scary. One example is CVE-2022-37968, which affects organizations running Kubernetes clusters on Azure and earned a CVSS score of 10.0 — the most severe score possible.

Microsoft says that to exploit this vulnerability an attacker would need to know the randomly generated DNS endpoint for an Azure Arc-enabled Kubernetes cluster. But that may not be such a tall order, says Breen, who notes that a number of free and commercial DNS discovery services now make it easy to find this information on potential targets.

Late last month, Microsoft acknowledged that attackers were exploiting two previously unknown vulnerabilities in Exchange Server. Paired together, the two flaws are known as “ProxyNotShell” and they can be chained to allow remote code execution on Exchange Server systems.

Microsoft said it was expediting work on official patches for the Exchange bugs, and it urged affected customers to enable certain settings to mitigate the threat from the attacks. However, those mitigation steps were soon shown to be ineffective, and Microsoft has been adjusting them on a daily basis nearly each day since then.

The lack of Exchange patches leaves a lot of Microsoft customers exposed. Security firm Rapid7 said that as of early September 2022 the company observed more than 190,000 potentially vulnerable instances of Exchange Server exposed to the Internet.

“While Microsoft confirmed the zero-days and issued guidance faster than they have in the past, there are still no patches nearly two weeks out from initial disclosure,” said Caitlin Condon, senior manager of vulnerability research at Rapid7. “Despite high hopes that today’s Patch Tuesday release would contain fixes for the vulnerabilities, Exchange Server is conspicuously missing from the initial list of October 2022 security updates. Microsoft’s recommended rule for blocking known attack patterns has been bypassed multiple times, emphasizing the necessity of a true fix.”

Adobe also released security updates to fix 29 vulnerabilities across a variety of products, including Acrobat and Reader, ColdFusion, Commerce and Magento. Adobe said it is not aware of active attacks against any of these flaws.

For a closer look at the patches released by Microsoft today and indexed by severity and other metrics, check out the always-useful Patch Tuesday roundup from the SANS Internet Storm Center. And it’s not a bad idea to hold off updating for a few days until Microsoft works out any kinks in the updates: AskWoody.com usually has the lowdown on any patches that may be causing problems for Windows users.

As always, please consider backing up your system or at least your important documents and data before applying system updates. And if you run into any problems with these updates, please drop a note about it here in the comments.

What are the warning signs that someone has hijacked your Steam account? Here is what to look for and what you can do to get your account back.

The post Steam account hacked? Here’s how to get it back appeared first on WeLiveSecurity

When U.S. consumers have their online bank accounts hijacked and plundered by hackers, U.S. financial institutions are legally obligated to reverse any unauthorized transactions as long as the victim reports the fraud in a timely manner. But new data released this week suggests that for some of the nation’s largest banks, reimbursing account takeover victims has become more the exception than the rule.

The findings came in a report released by Sen. Elizabeth Warren (D-Mass.), who in April 2022 opened an investigation into fraud tied to Zelle, the “peer-to-peer” digital payment service used by many financial institutions that allows customers to quickly send cash to friends and family.

Zelle is run by Early Warning Services LLC (EWS), a private financial services company which is jointly owned by Bank of America, Capital One, JPMorgan Chase, PNC Bank, Truist, U.S. Bank, and Wells Fargo. Zelle is enabled by default for customers at over 1,000 different financial institutions, even if a great many customers still don’t know it’s there.

Sen. Warren said several of the EWS owner banks — including Capital One, JPMorgan and Wells Fargo — failed to provide all of the requested data. But Warren did get the requested information from PNC, Truist and U.S. Bank.

“Overall, the three banks that provided complete data sets reported 35,848 cases of scams, involving over $25.9 million of payments in 2021 and the first half of 2022,” the report summarized. “In the vast majority of these cases, the banks did not repay the customers that reported being scammed. Overall these three banks reported repaying customers in only 3,473 cases (representing nearly 10% of scam claims) and repaid only $2.9 million.”

Importantly, the report distinguishes between cases that involve straight up bank account takeovers and unauthorized transfers (fraud), and those losses that stem from “fraudulently induced payments,” where the victim is tricked into authorizing the transfer of funds to scammers (scams).

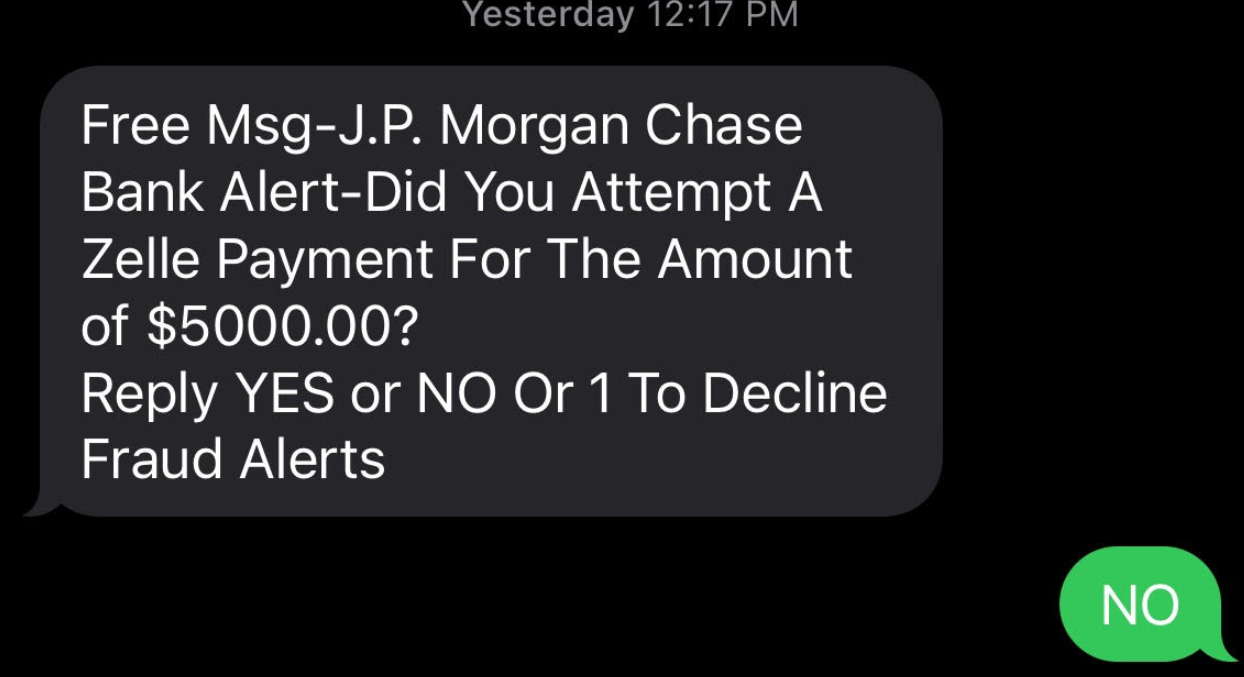

A common example of the latter is the Zelle Fraud Scam, which uses an ever-shifting set of come-ons to trick people into transferring money to fraudsters. The Zelle Fraud Scam often employs text messages and phone calls spoofed to look like they came from your bank, and the scam usually relates to fooling the customer into thinking they’re sending money to themselves when they’re really sending it to the crooks.

Here’s the rub: When a customer issues a payment order to their bank, the bank is obligated to honor that order so long as it passes a two-stage test. The first question asks, Did the request actually come from an authorized owner or signer on the account? In the case of Zelle scams, the answer is yes.

Trace Fooshee, a strategic advisor in the anti money laundering practice at Aite-Novarica, said the second stage requires banks to give the customer’s transfer order a kind of “sniff test” using “commercially reasonable” fraud controls that generally are not designed to detect patterns involving social engineering.

Fooshee said the legal phrase “commercially reasonable” is the primary reason why no bank has much — if anything — in the way of controlling for scam detection.

“In order for them to deploy something that would detect a good chunk of fraud on something so hard to detect they would generate egregiously high rates of false positives which would also make consumers (and, then, regulators) very unhappy,” Fooshee said. “This would tank the business case for the service as a whole rendering it something that the bank can claim to NOT be commercially reasonable.”

Sen. Warren’s report makes clear that banks generally do not pay consumers back if they are fraudulently induced into making Zelle payments.

“In simple terms, Zelle indicated that it would provide redress for users in cases of unauthorized transfers in which a user’s account is accessed by a bad actor and used to transfer a payment,” the report continued. “However, EWS’ response also indicated that neither Zelle nor its parent bank owners would reimburse users fraudulently induced by a bad actor into making a payment on the platform.”

Still, the data suggest banks did repay at least some of the funds stolen from scam victims about 10 percent of the time. Fooshee said he’s surprised that number is so high.

“That banks are paying victims of authorized payment fraud scams anything at all is noteworthy,” he said. “That’s money that they’re paying for out of pocket almost entirely for goodwill. You could argue that repaying all victims is a sound strategy especially in the climate we’re in but to say that it should be what all banks do remains an opinion until Congress changes the law.”

However, when it comes to reimbursing victims of fraud and account takeovers, the report suggests banks are stiffing their customers whenever they can get away with it. “Overall, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received,” the report notes.

How did the banks behave individually? From the report:

-In 2021 and the first six months of 2022, PNC Bank indicated that its customers reported 10,683 cases of unauthorized payments totaling over $10.6 million, of which only 1,495 cases totaling $1.46 were refunded to consumers. PNC Bank left 86% of its customers that reported cases of fraud without recourse for fraudulent activity that occurred on Zelle.

-Over this same time period, U.S. Bank customers reported a total of 28,642 cases of unauthorized transactions totaling over $16.2 million, while only refunding 8,242 cases totaling less than $4.7 million.

-In the period between January 2021 and September 2022, Bank of America customers reported 81,797 cases of unauthorized transactions, totaling $125 million. Bank of America refunded only $56.1 million in fraud claims – less than 45% of the overall dollar value of claims made in that time.

–Truist indicated that the bank had a much better record of reimbursing defrauded customers over this same time period. During 2021 and the first half of 2022, Truist customers filed 24,752 unauthorized transaction claims amounting to $24.4 million. Truist reimbursed 20,349 of those claims, totaling $20.8 million – 82% of Truist claims were reimbursed over this period. Overall, however, the four banks that provided complete data sets indicated that they reimbursed only 47% of the dollar amount of fraud claims they received.

Fooshee said there has long been a great deal of inconsistency in how banks reimburse unauthorized fraud claims — even after the Consumer Financial Protection Bureau (CPFB) came out with guidance on what qualifies as an unauthorized fraud claim.

“Many banks reported that they were still not living up to those standards,” he said. “As a result, I imagine that the CFPB will come down hard on those with fines and we’ll see a correction.”

Fooshee said many banks have recently adjusted their reimbursement policies to bring them more into line with the CFPB’s guidance from last year.

“So this is heading in the right direction but not with sufficient vigor and speed to satisfy critics,” he said.

Seth Ruden is a payments fraud expert who serves as director of global advisory for digital identity company BioCatch. Ruden said Zelle has recently made “significant changes to its fraud program oversight because of consumer influence.”

“It is clear to me that despite sensational headlines, progress has been made to improve outcomes,” Ruden said. “Presently, losses in the network on a volume-adjusted basis are lower than those typical of credit cards.”

But he said any failure to reimburse victims of fraud and account takeovers only adds to pressure on Congress to do more to help victims of those scammed into authorizing Zelle payments.

“The bottom line is that regulations have not kept up with the speed of payment technology in the United States, and we’re not alone,” Ruden said. “For the first time in the UK, authorized payment scam losses have outpaced credit card losses and a regulatory response is now on the table. Banks have the choice right now to take action and increase controls or await regulators to impose a new regulatory environment.”

Sen. Warren’s report is available here (PDF).

There are, of course, some versions of the Zelle fraud scam that may be confusing financial institutions as to what constitutes “authorized” payment instructions. For example, the variant I wrote about earlier this year began with a text message that spoofed the target’s bank and warned of a pending suspicious transfer.

Those who responded at all received a call from a number spoofed to make it look like the victim’s bank calling, and were asked to validate their identities by reading back a one-time password sent via SMS. In reality, the thieves had simply asked the bank’s website to reset the victim’s password, and that one-time code sent via text by the bank’s site was the only thing the crooks needed to reset the target’s password and drain the account using Zelle.

None of the above discussion involves the risks affecting businesses that bank online. Businesses in the United States do not enjoy the same fraud liability protection afforded to consumers, and if a banking trojan or clever phishing site results in a business account getting drained, most banks will not reimburse that loss.

This is why I have always and will continue to urge small business owners to conduct their online banking affairs only from a dedicated, access restricted and security-hardened device — and preferably a non-Windows machine.

For consumers, the same old advice remains the best: Watch your bank statements like a hawk, and immediately report and contest any charges that appear fraudulent or unauthorized.

Whether or not you’ve heard the term “doxxing” before, you’re probably familiar with the problem it names: collecting personal information about someone online to track down and reveal their real-life identity. The motivations for doxxing are many, and mostly malicious: for some doxxers, the goal in tracking someone is identity theft. For others, it’s part of a pattern of stalking or online harassment to intimidate, silence or punish their victim – and overwhelmingly, victims are youth and young adults, women, and LGBTQ+ people. The truth is, most of us have information online that we don’t realize can put us at risk, and that’s why I’ve written this series: to inform readers about how doxxing happens, and how you can protect yourself from this very real and growing problem by doxxing yourself.

In computer security, we talk about the idea of a “security mindset”: understanding how someone with bad intentions would cause harm, and being able to think like they would to find weak spots. In this series, you will learn by doing. By understanding the tools and methods used by those with ill intent, you’ll be better prepared to keep yourself safe and your information secure.

Your mission, should you choose to accept it, is to follow along and find out everything the internet knows about… you!

This series will provide simple steps for you to follow as you begin your investigation. Along the way, as you get familiar with the tools and tactics of internet sleuths, you’ll get a better idea of your current internet footprint as well as know what tracks you leave in the future. Our process will be split into three main sections:

Information is power. And in the case of doxxing, most people don’t realize how much of their power they’re giving up! My goal in this series is to demystify the methods used for doxxing, so in the spirit of “showing my work,” here are some of the best resources and collected checklists I referenced when planning these exercises, along with how to best use each:

If this looks like a whole lot of homework… don’t worry! We’ll cover most of the core tools and tips mentioned in these resources through the course of this series, and we’ll revisit these links at the end of the series when you’ve gotten more context on what they cover. In the next article, we’ll take on the review step of our process, getting a holistic inventory of what personal information is currently available online so you can prioritize the most important fixes. See you soon!

We’d love to hear what you think. Ask a Question, Comment Below, and Stay Connected with Cisco Secure on social!

Cisco Secure Social Channels

A recent proliferation of phony executive profiles on LinkedIn is creating something of an identity crisis for the business networking site, and for companies that rely on it to hire and screen prospective employees. The fabricated LinkedIn identities — which pair AI-generated profile photos with text lifted from legitimate accounts — are creating major headaches for corporate HR departments and for those managing invite-only LinkedIn groups.

Some of the fake profiles flagged by the co-administrator of a popular sustainability group on LinkedIn.

Last week, KrebsOnSecurity examined a flood of inauthentic LinkedIn profiles all claiming Chief Information Security Officer (CISO) roles at various Fortune 500 companies, including Biogen, Chevron, ExxonMobil, and Hewlett Packard.

Since then, the response from LinkedIn users and readers has made clear that these phony profiles are showing up en masse for virtually all executive roles — but particularly for jobs and industries that are adjacent to recent global events and news trends.

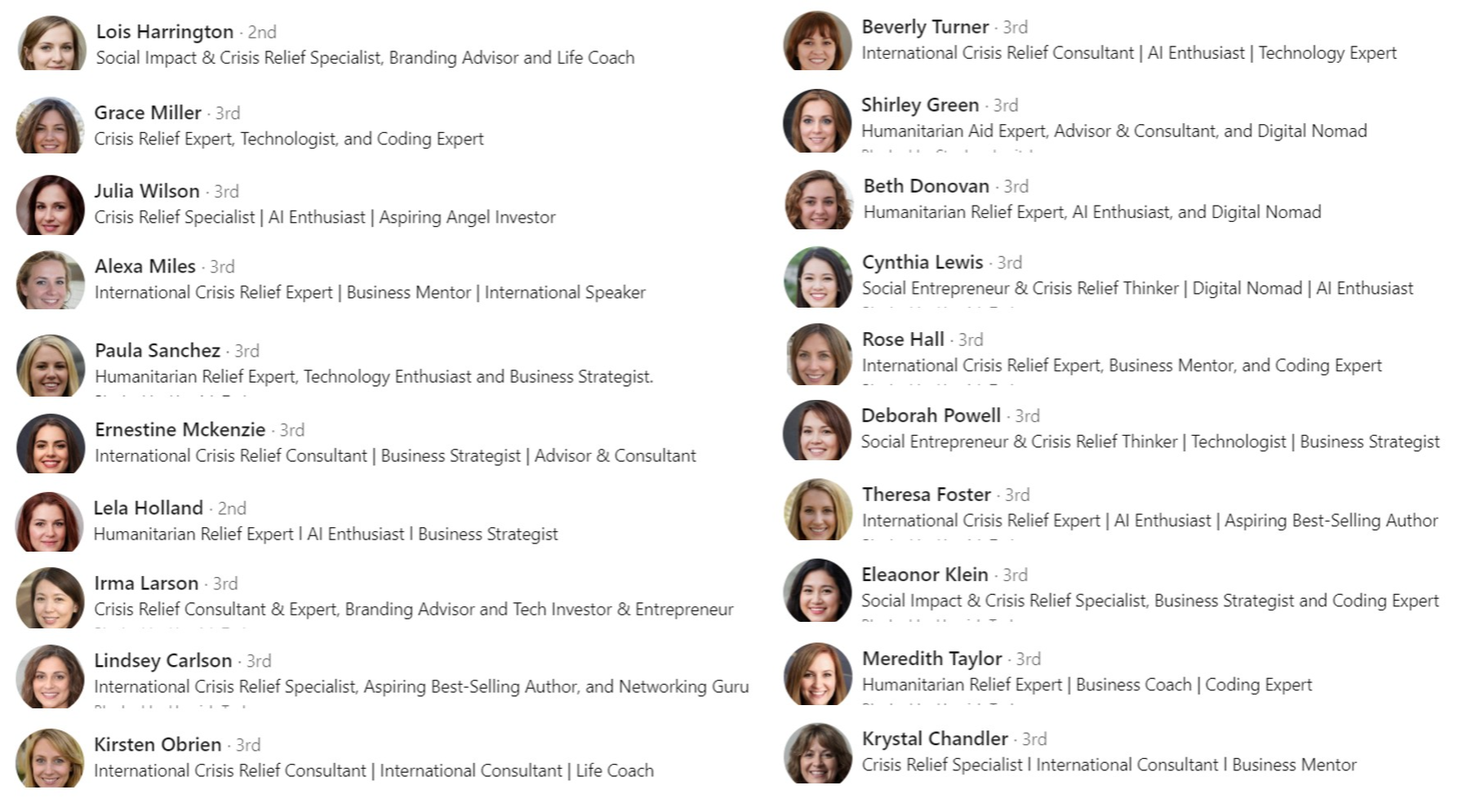

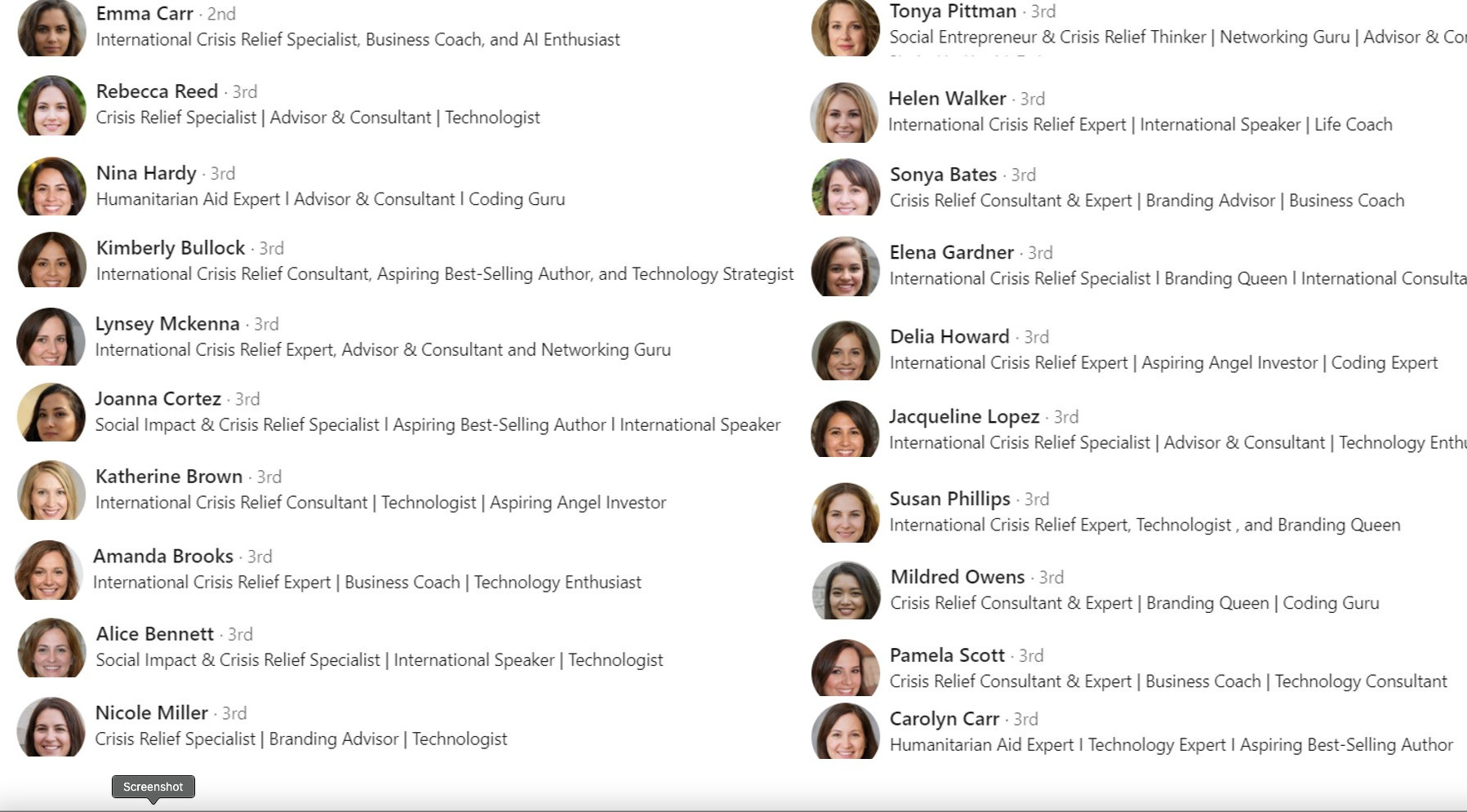

Hamish Taylor runs the Sustainability Professionals group on LinkedIn, which has more than 300,000 members. Together with the group’s co-owner, Taylor said they’ve blocked more than 12,700 suspected fake profiles so far this year, including dozens of recent accounts that Taylor describes as “cynical attempts to exploit Humanitarian Relief and Crisis Relief experts.”

“We receive over 500 fake profile requests to join on a weekly basis,” Taylor said. “It’s hit like hell since about January of this year. Prior to that we did not get the swarms of fakes that we now experience.”

The opening slide for a plea by Taylor’s group to LinkedIn.

Taylor recently posted an entry on LinkedIn titled, “The Fake ID Crisis on LinkedIn,” which lampooned the “60 Least Wanted ‘Crisis Relief Experts’ — fake profiles that claimed to be experts in disaster recovery efforts in the wake of recent hurricanes. The images above and below show just one such swarm of profiles the group flagged as inauthentic. Virtually all of these profiles were removed from LinkedIn after KrebsOnSecurity tweeted about them last week.

Another “swarm” of LinkedIn bot accounts flagged by Taylor’s group.

Mark Miller is the owner of the DevOps group on LinkedIn, and says he deals with fake profiles on a daily basis — often hundreds per day. What Taylor called “swarms” of fake accounts Miller described instead as “waves” of incoming requests from phony accounts.

“When a bot tries to infiltrate the group, it does so in waves,” Miller said. “We’ll see 20-30 requests come in with the same type of information in the profiles.”

After screenshotting the waves of suspected fake profile requests, Miller started sending the images to LinkedIn’s abuse teams, which told him they would review his request but that he may never be notified of any action taken.

Some of the bot profiles identified by Mark Miller that were seeking access to his DevOps LinkedIn group. Miller said these profiles are all listed in the order they appeared.

Miller said that after months of complaining and sharing fake profile information with LinkedIn, the social media network appeared to do something which caused the volume of group membership requests from phony accounts to drop precipitously.

“I wrote our LinkedIn rep and said we were considering closing the group down the bots were so bad,” Miller said. “I said, ‘You guys should be doing something on the backend to block this.”

Jason Lathrop is vice president of technology and operations at ISOutsource, a Seattle-based consulting firm with roughly 100 employees. Like Miller, Lathrop’s experience in fighting bot profiles on LinkedIn suggests the social networking giant will eventually respond to complaints about inauthentic accounts. That is, if affected users complain loudly enough (posting about it publicly on LinkedIn seems to help).

Lathrop said that about two months ago his employer noticed waves of new followers, and identified more than 3,000 followers that all shared various elements, such as profile photos or text descriptions.

“Then I noticed that they all claim to work for us at some random title within the organization,” Lathrop said in an interview with KrebsOnSecurity. “When we complained to LinkedIn, they’d tell us these profiles didn’t violate their community guidelines. But like heck they don’t! These people don’t exist, and they’re claiming they work for us!”

Lathrop said that after his company’s third complaint, a LinkedIn representative responded by asking ISOutsource to send a spreadsheet listing every legitimate employee in the company, and their corresponding profile links.

Not long after that, the phony profiles that were not on the company’s list were deleted from LinkedIn. Lathrop said he’s still not sure how they’re going to handle getting new employees allowed into their company on LinkedIn going forward.

It remains unclear why LinkedIn has been flooded with so many fake profiles lately, or how the phony profile photos are sourced. Random testing of the profile photos shows they resemble but do not match other photos posted online. Several readers pointed out one likely source — the website thispersondoesnotexist.com, which makes using artificial intelligence to create unique headshots a point-and-click exercise.

Cybersecurity firm Mandiant (recently acquired by Google) told Bloomberg that hackers working for the North Korean government have been copying resumes and profiles from leading job listing platforms LinkedIn and Indeed, as part of an elaborate scheme to land jobs at cryptocurrency firms.

Fake profiles also may be tied to so-called “pig butchering” scams, wherein people are lured by flirtatious strangers online into investing in cryptocurrency trading platforms that eventually seize any funds when victims try to cash out.

In addition, identity thieves have been known to masquerade on LinkedIn as job recruiters, collecting personal and financial information from people who fall for employment scams.

But the Sustainability Group administrator Taylor said the bots he’s tracked strangely don’t respond to messages, nor do they appear to try to post content.

“Clearly they are not monitored,” Taylor assessed. “Or they’re just created and then left to fester.”

This experience was shared by the DevOp group admin Miller, who said he’s also tried baiting the phony profiles with messages referencing their fakeness. Miller says he’s worried someone is creating a massive social network of bots for some future attack in which the automated accounts may be used to amplify false information online, or at least muddle the truth.

“It’s almost like someone is setting up a huge bot network so that when there’s a big message that needs to go out they can just mass post with all these fake profiles,” Miller said.

In last week’s story on this topic, I suggested LinkedIn could take one simple step that would make it far easier for people to make informed decisions about whether to trust a given profile: Add a “created on” date for every profile. Twitter does this, and it’s enormously helpful for filtering out a great deal of noise and unwanted communications.

Many of our readers on Twitter said LinkedIn needs to give employers more tools — perhaps some kind of application programming interface (API) — that would allow them to quickly remove profiles that falsely claim to be employed at their organizations.

Another reader suggested LinkedIn also could experiment with offering something akin to Twitter’s verified mark to users who chose to validate that they can respond to email at the domain associated with their stated current employer.

In response to questions from KrebsOnSecurity, LinkedIn said it was considering the domain verification idea.

“This is an ongoing challenge and we’re constantly improving our systems to stop fakes before they come online,” LinkedIn said in a written statement. “We do stop the vast majority of fraudulent activity we detect in our community – around 96% of fake accounts and around 99.1% of spam and scams. We’re also exploring new ways to protect our members such as expanding email domain verification. Our community is all about authentic people having meaningful conversations and to always increase the legitimacy and quality of our community.”

In a story published Wednesday, Bloomberg noted that LinkedIn has largely so far avoided the scandals about bots that have plagued networks like Facebook and Twitter. But that shine is starting to come off, as more users are forced to waste more of their time fighting off inauthentic accounts.

“What’s clear is that LinkedIn’s cachet as being the social network for serious professionals makes it the perfect platform for lulling members into a false sense of security,” Bloomberg’s Tim Cuplan wrote. “Exacerbating the security risk is the vast amount of data that LinkedIn collates and publishes, and which underpins its whole business model but which lacks any robust verification mechanisms.”

Malicious software, or “malware,” refers to any program designed to infect and disrupt computer systems and networks. The risks associated with a malware infection can range from poor device performance to stolen data.

However, thanks to their closed ecosystem, built-in security features, and strict policies on third-party apps, Apple devices tend to be less prone to malware infections compared to their Android counterparts. But it’s important to note that they’re not completely without vulnerabilities.

Several iPhone viruses could infect your smartphone and affect its functionality, especially if you jailbreak your iPhone (that is, opening your iOS to wider features, apps, and themes).

This article covers how you can detect malware infections and how to remove viruses from your device so you can get back to enjoying the digital world.

Malware can affect your iPhone in a variety of ways. Here are a few telltale signs that your iPhone might have an unwelcome visitor.

If you notice any of the signs above, it’s a good idea to check for malware. Here are some steps you can take.

If you’ve confirmed malware on your iPhone, don’t worry. There’s still time to protect yourself and your data. Below is an action plan you can follow to remove malware from your device.

In many cases, hackers exploit outdated versions of iOS to launch malware attacks. If you don’t have the latest version of your operating system, it’s a good idea to update iOS to close this potential vulnerability. Just follow these steps:

It might sound simple, but restarting your device can fix certain issues. The system will restart on its own when updating the iOS. If you already have the latest version, restart your iPhone now.

If updating the iOS and restarting your device didn’t fix the issue, try clearing your phone’s browsing history and data. If you’re using Safari, follow these steps:

Keep in mind that the process is similar for Google Chrome and most other popular web browsers.

Malicious software, such as spyware and ransomware, often end up on phones by masquerading as legitimate apps. To err on the side of caution, delete any apps that you don’t remember downloading or installing.

The option to restore to a previous backup is one of the most valuable features found on the iPhone and iPad. Essentially, this allows you to restore your device to an iCloud backup made before the malware infection.

Here’s how:

If none of the steps above solves the problem, a factory reset might be the next order of business. Restoring your phone to factory settings will reset it to its out-of-factory configuration, deleting all of your apps, content, and settings in the process and replacing them with original software only.

To factory reset your iPhone, follow these steps:

The best way to protect your iOS device is to avoid malware in the first place. Follow these security measures to safeguard your device:

If you have an iPhone and are like most other people, you probably use your device for almost everything you do online. And while it’s amazing to have the internet in the palm of your hands, it’s also important to be aware of online threats like malware, which can put your digital life at risk.

The good news is that McAfee has your back with our award-winning and full-scale mobile security app. McAfee Mobile Security provides full protection against various types of malware targeting the Apple ecosystem. With safe browsing features, a secure VPN, and antivirus software, McAfee Security for iOS delivers protection against emerging threats, so you can continue to use your iPhone with peace of mind.

Download the McAfee Security app today and get all-in-one protection.

The post A Guide to Remove Malware From Your iPhone appeared first on McAfee Blog.